Ford Motor Company (NYSE: F) has bounced back this year, trading near $13/share after a strong rally. The stock remains a steady value name, supported by its dominant truck lineup and disciplined cost control, though growth expectations stay muted as the EV transition continues to pressure results.

Recently, Ford announced plans to expand production of its hybrid F-150 and launch a new lineup of affordable EVs aimed at boosting competitiveness in North America. The company also reported stronger-than-expected quarterly profits, driven by cost cuts and higher demand for its commercial vehicle division. These updates show Ford’s strategy is focused on profitability and efficiency rather than chasing volume growth at all costs.

This article explores where Wall Street analysts believe Ford could trade by 2027. We’ve gathered consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Limited Downside

Ford trades near $13/share today. The average analyst price target is $12/share, slightly below the current price, suggesting limited downside over the next year. Forecasts show a wide range and reflect mixed sentiment among analysts:

- High estimate: ~$16/share

- Low estimate: ~$10/share

- Median target: ~$12/share

- Ratings: 2 Buys, 2 Outperforms, 16 Holds, 2 Sells

This range highlights the market’s uncertainty about Ford’s next phase of growth. While analysts acknowledge the company’s progress in cost control and cash generation, most believe these strengths are already reflected in the share price. For investors, this means Ford’s upside potential appears capped unless management delivers a clear turnaround in its EV strategy or stronger-than-expected earnings growth.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Ford: Growth Outlook and Valuation

Ford’s fundamentals remain stable but lack major catalysts.

- Revenue growth: ~0.5% CAGR through 2027

- Operating margins: ~5%

- Forward P/E: ~9x

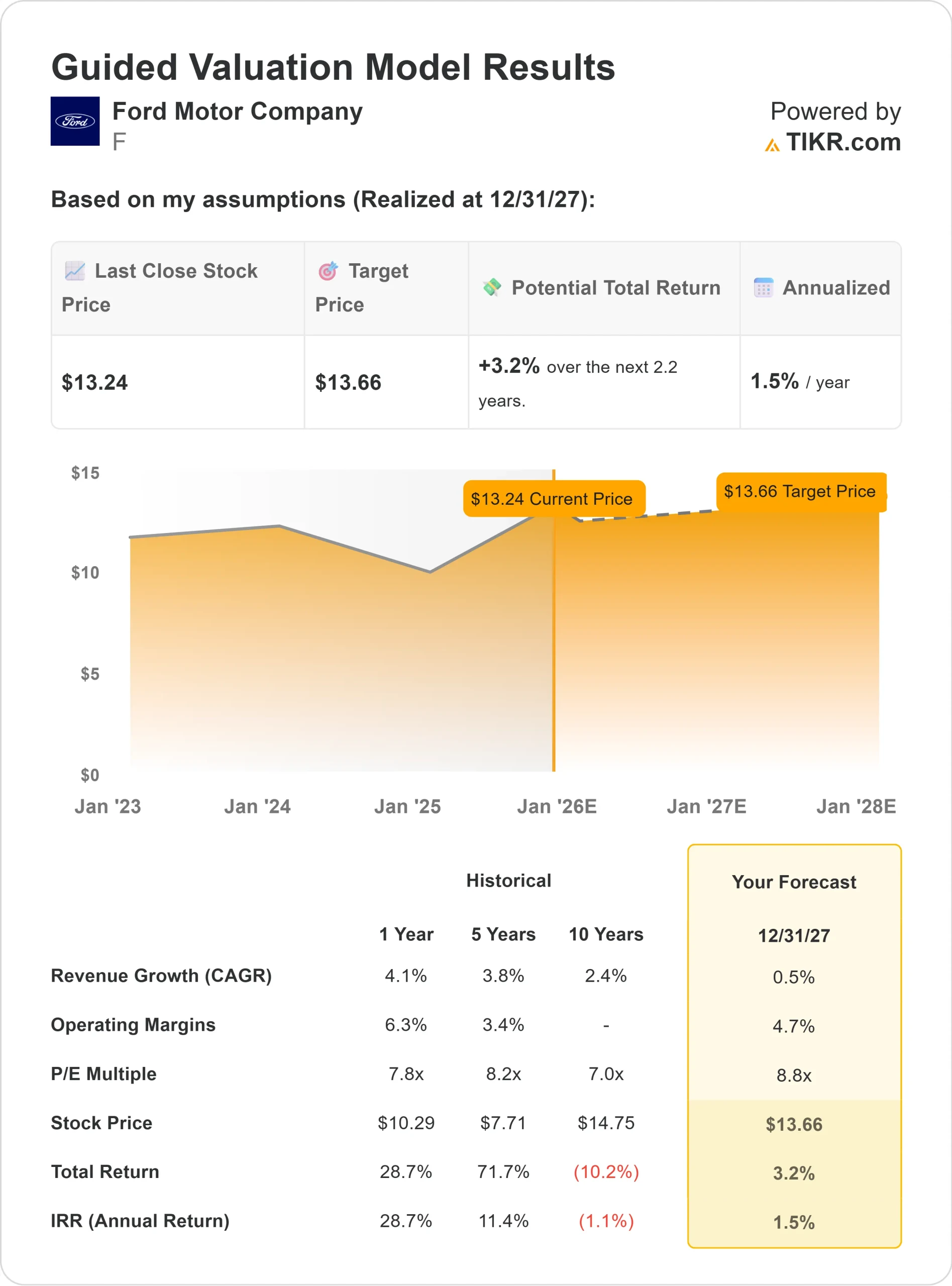

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 9x forward P/E suggests ~$14/share by 2027,

- That implies about 3% total upside, or roughly 1.5% annualized returns.

These projections point to a company that can deliver steady performance but not explosive growth. Ford’s 4.6% dividend yield provides most of its expected return, supported by reliable cash flow from its truck and commercial vehicle franchises. For investors, Ford looks more like a stable value and income play than a growth opportunity. It may appeal to those prioritizing consistency over capital appreciation.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Ford continues to strengthen its most profitable businesses. The company’s truck and commercial vehicle segments remain industry leaders, generating reliable cash flow even in a slower economy. Its hybrid strategy is gaining traction, with strong demand for hybrid F-150 models helping offset weaker electric vehicle sales.

Management has also emphasized capital discipline and cost efficiency, which are beginning to show results. Operating margins are improving gradually, and the company is prioritizing profitability over volume growth. For investors, these actions suggest Ford has the tools to sustain earnings stability and protect shareholder value through market cycles.

Bear Case: Growth and EV Uncertainty

Even with these positives, Ford faces ongoing challenges. The global auto market is slowing, and the company’s full EV rollout has been more difficult than expected. Delays, pricing pressure, and rising competition from Tesla and Chinese automakers could limit margin expansion in the near term.

Ford also carries significant leverage, leaving it vulnerable if demand softens or production costs rise. For investors, the concern is that Ford’s solid truck franchise may not be enough to offset these headwinds. Without faster growth or a more competitive EV lineup, the stock could remain stuck near current levels.

Outlook for 2027: What Could Ford Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 9x forward P/E suggests Ford could trade near $14/share by 2027. That would represent about 3% total upside, or roughly 1.5% annualized returns from today’s price near $13/share.

While the model points to limited capital appreciation, Ford’s 4.6% dividend yield provides a solid income cushion. For investors, the outlook reflects a steady but unspectacular return profile. The stock looks well-suited for those seeking consistency and cash flow, but less appealing for those targeting high growth.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>