Align Technology, Inc. (NASDAQ: ALGN) has faced a challenging stretch in 2025. Demand for clear aligners has softened amid weaker consumer spending and a slower dental market recovery. Shares trade near $132/share, down sharply from last year’s highs, as investors turn cautious on discretionary health products.

Recently, Align reported steady third-quarter results that showed sequential improvement in margins and solid growth in its iTero scanner business. The company also introduced new AI-driven treatment planning tools aimed at improving accuracy and patient outcomes, signaling its ongoing commitment to digital orthodontic innovation. These updates show that Align continues to invest in technology and expand its leadership position despite short-term demand pressure.

This article explores where Wall Street analysts believe Align Technology could trade by 2027. We’ve compiled consensus price targets and valuation model results to outline the stock’s potential path ahead. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

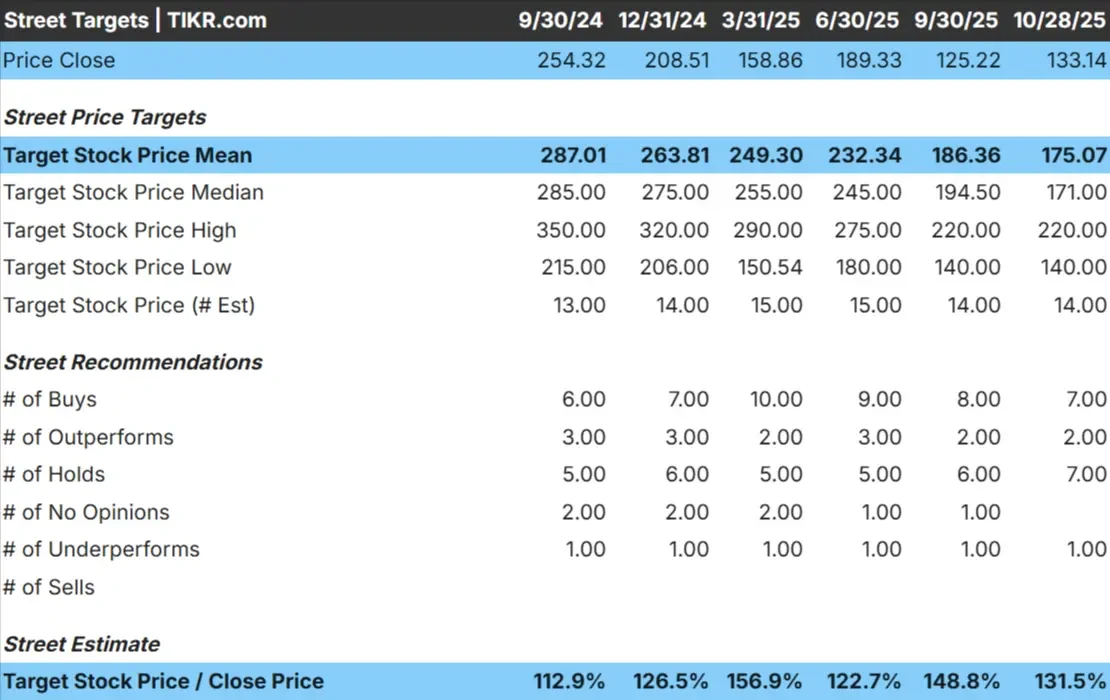

Align Technology trades near $132/share today. The average analyst price target is around $175/share, which points to about 31% upside. Forecasts vary widely and reflect mixed sentiment among Wall Street analysts:

- High estimate: ~$220/share

- Low estimate: ~$140/share

- Median target: ~$171/share

- Ratings: 7 Buys, 2 Outperforms, 7 Holds, 1 Underperform

It looks like analysts see meaningful upside ahead, but conviction remains divided. For investors, this suggests the market expects gradual stabilization rather than a sharp rebound in earnings momentum.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Align Technology: Growth Outlook and Valuation

The company’s fundamentals appear steady but not especially strong:

- Revenue is expected to grow about 2–3% annually through 2027

- Operating margins are projected to hold near 23%

- Shares trade around 13x forward earnings, below long-term averages

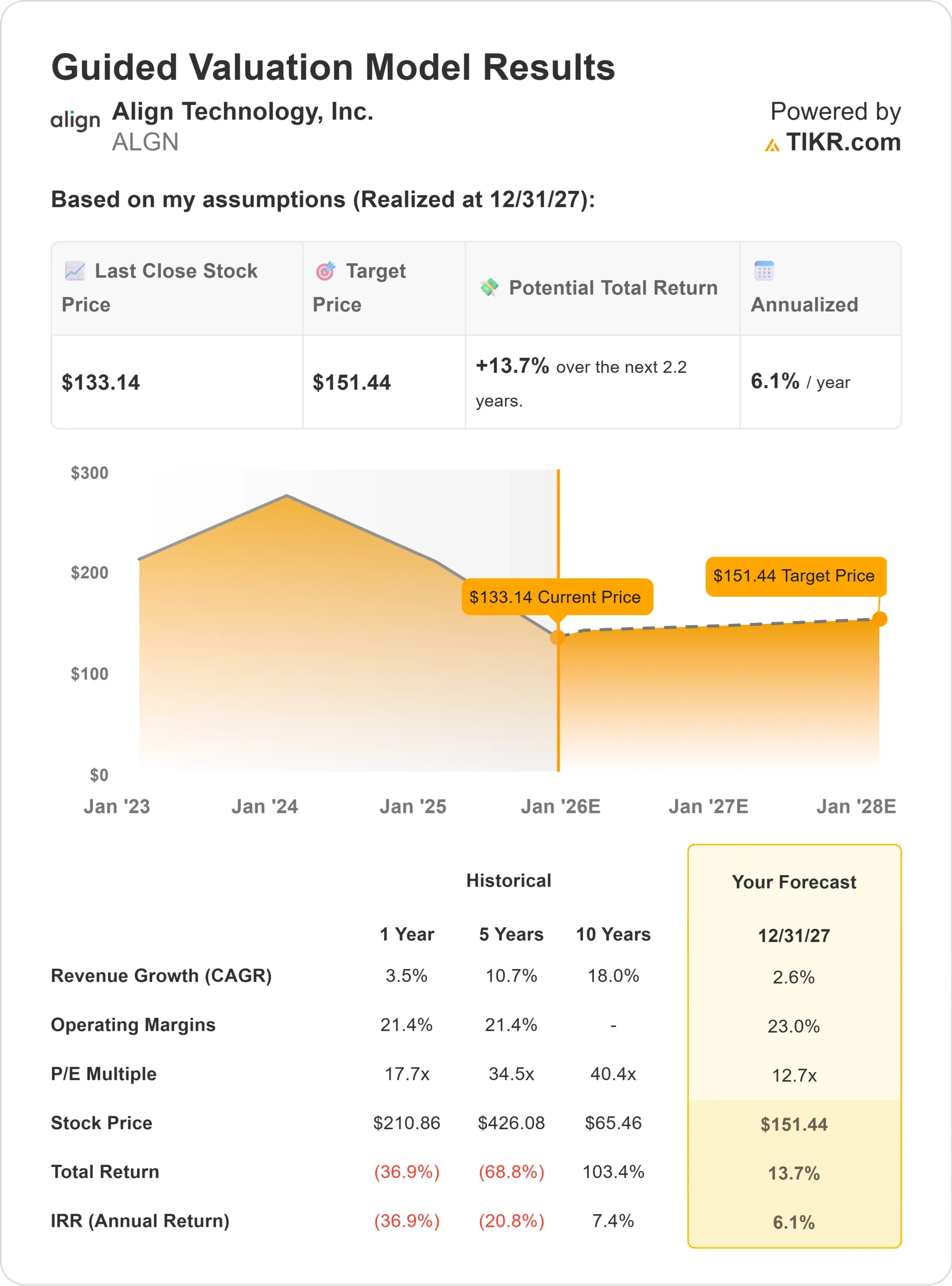

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a forward P/E of roughly 13x suggests ~$151/share by 2027.

- That implies about 14% total upside, or around 6% annualized returns.

These assumptions suggest Align can deliver steady compounding, though likely at a slower pace than in prior years. The stock looks fairly priced for its fundamentals, and meaningful upside would depend on stronger margin recovery or renewed demand in global aligner markets.

For investors, Align offers a balanced setup with reasonable valuation, dependable margins, and moderate upside potential. It is more of a quality compounder than a rapid growth play.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Align remains the clear leader in digital orthodontics. Its brand strength, global reach, and innovation pipeline continue to support its position in a growing but competitive industry. The company’s focus on AI-driven treatment planning and expanding its iTero scanner ecosystem reinforces its technological moat and customer loyalty.

International markets also present an opportunity for long-term growth as awareness of clear aligners increases. Align’s consistent product innovation and practitioner education efforts could help it capture this demand once macro conditions improve.

For investors, These strengths suggest Align has the foundation to gradually rebuild earnings momentum and sustain its leadership position over time.

Bear Case: Slow Recovery and Competition

Despite its strengths, Align’s recovery may take time. The business is sensitive to consumer confidence and dental office activity, which remain uneven across markets. A slower rebound in elective healthcare spending could limit near-term growth.

Competition is also intensifying as low-cost regional brands and traditional orthodontic solutions put pressure on pricing.

For investors, The main risk is that Align’s strong brand and innovation leadership may not be enough to offset pricing and volume headwinds if demand remains soft.

Outlook for 2027: What Could Align Be Worth

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a forward P/E of around 13x suggests Align could trade near $151/share by 2027. That represents about a 14% total upside, or roughly 6% annualized returns from today’s price near $133/share.

While this would mark a modest recovery, it already assumes stable margins and slow but steady growth. For stronger returns, Align would need to accelerate aligner volume growth, maintain pricing power, and deepen penetration in international markets.

For investors, Align looks like a steady long-term compounder with measured upside potential. The company’s consistent innovation, balance sheet strength, and leading market position make it a credible hold for patient investors focused on quality over quick gains.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>