Johnson & Johnson (NYSE: JNJ) continues to deliver steady results even as its growth pace slows. With strong margins, a fortress balance sheet, and a reliable dividend, J&J remains a core defensive play in healthcare.

Recently, J&J reported third-quarter results that beat expectations, supported by strong MedTech sales and continued recovery in its Innovative Medicine segment. The company also gained FDA approval for its new lung cancer treatment Rybrevant combination therapy and announced plans to expand its robotic surgery platform, Ottava, into clinical trials in 2026. These developments highlight J&J’s focus on innovation and its steady pivot toward higher-growth healthcare technologies.

This article explores where Wall Street analysts think Johnson & Johnson could trade by 2027. We’ve pulled together consensus price targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Very Limited Upside

JNJ trades around $190/share today. The average analyst price target sits near $198/share, suggesting roughly 3% upside over the next year. Forecasts show a wide range:

- High estimate: ~$225/share

- Low estimate: ~$155/share

- Median target: ~$204/share

- Ratings: 9 Buys, 3 Outperforms, 11 Holds, 1 Underperform

With only a few points of potential upside, analysts see J&J as largely priced in. For investors, that means the stock is viewed more as a dependable income play than a high-growth opportunity. The reward here is stability and consistent dividends, not explosive returns.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Johnson & Johnson: Growth Outlook and Valuation

The company’s fundamentals remain stable and predictable:

- Revenue is projected to grow about 5% annually through 2027

- Operating margins are expected to hold near 33%

- Shares trade around 15x forward earnings, close to their long-term average

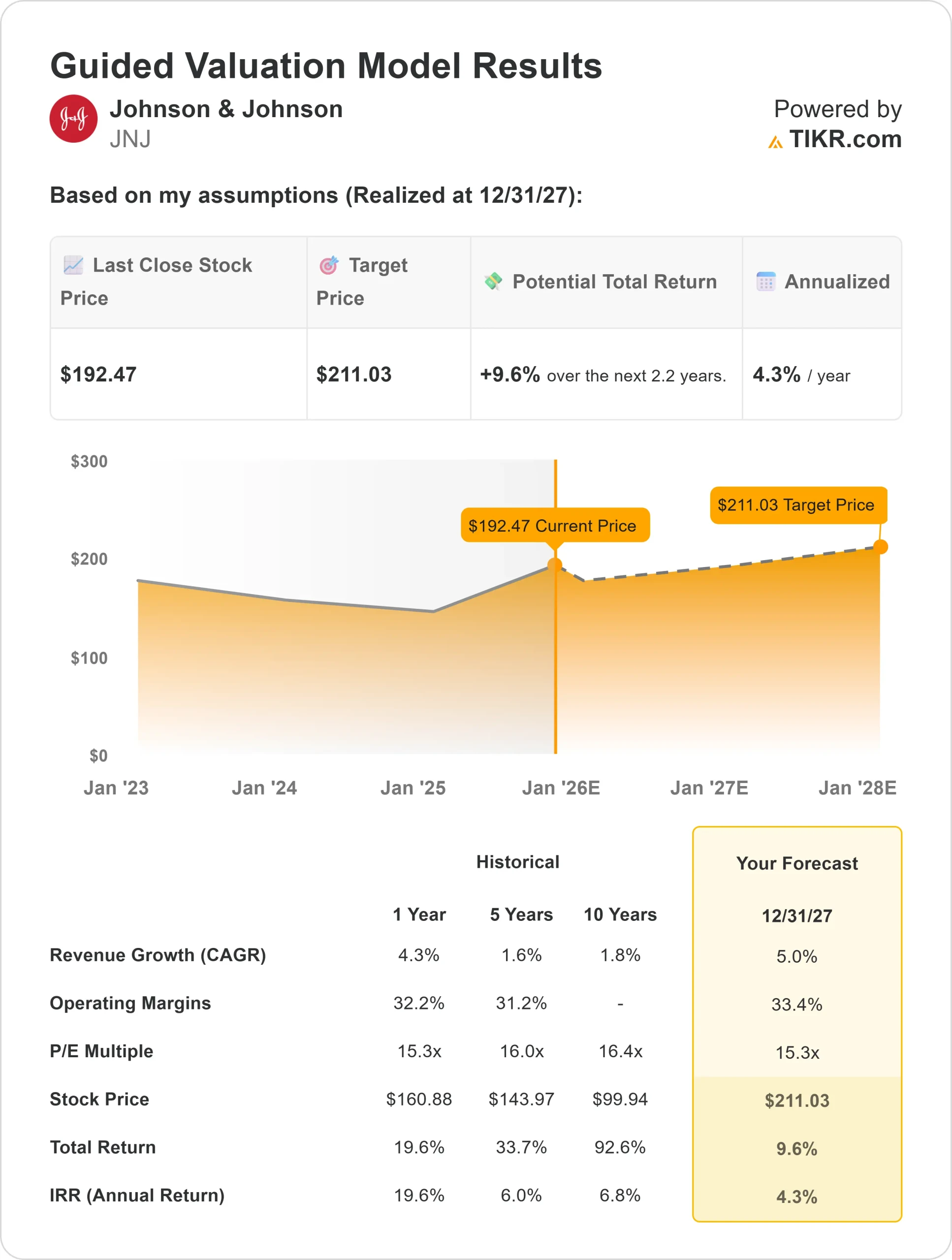

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 15x forward P/E suggests around $211/share by 2027

- That implies about 9.6% total upside, or roughly 4% annualized returns

For investors, this points to slow but steady compounding. J&J fits best for those prioritizing safety and reliability. It is unlikely to lead in growth, but it continues to reward long-term holders with consistent cash flow and dividend growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

J&J’s diversified portfolio remains a major advantage. The MedTech segment continues to grow through new products in surgical robotics and cardiovascular care, while the Innovative Medicine division benefits from strong oncology and immunology pipelines. These areas help offset slower growth in older pharmaceutical products.

The company’s strong balance sheet and dependable free cash flow also give it flexibility to invest in R&D, strategic acquisitions, and dividend hikes. For investors, these strengths show J&J’s ability to keep delivering stable earnings and long-term resilience even during uncertain markets.

Bear Case: Slower Growth and Legal Overhangs

Despite its durability, J&J’s growth story is far from perfect. Its pharmaceutical arm faces patent expirations, while litigation related to product liabilities remains a lingering concern. Both could limit valuation expansion or weigh on future earnings momentum.

For investors, the key risk is stagnation. J&J could continue generating solid profits but struggle to deliver market-beating returns without new catalysts. Until it accelerates growth in its MedTech pipeline or sees a breakthrough in drug development, upside may stay limited.

Outlook for 2027: What Could J&J Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 15x forward P/E suggests J&J could trade around $211/share by 2027. That represents about a 9.6% total return or roughly 4% annualized gains from current levels.

For investors, this suggests J&J is fairly valued with modest upside tied to execution rather than multiple expansion. The company’s mix of consistent earnings, strong cash flow, and a dependable dividend makes it one of the most stable compounders in the healthcare space.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.