Eaton Corporation plc (NYSE: ETN) has been one of the strongest industrial performers in recent years. The stock trades around $372/share, near record highs, supported by growing demand for electrification, grid modernization, and aerospace systems.

Recently, Eaton secured new work supporting U.S. grid modernization efforts and expanded its electrical segment to meet rising demand for power management and EV components. The company also strengthened its position in high-voltage systems through a strategic acquisition, reinforcing its leadership in the global energy transition and ability to benefit from long-term infrastructure investment.

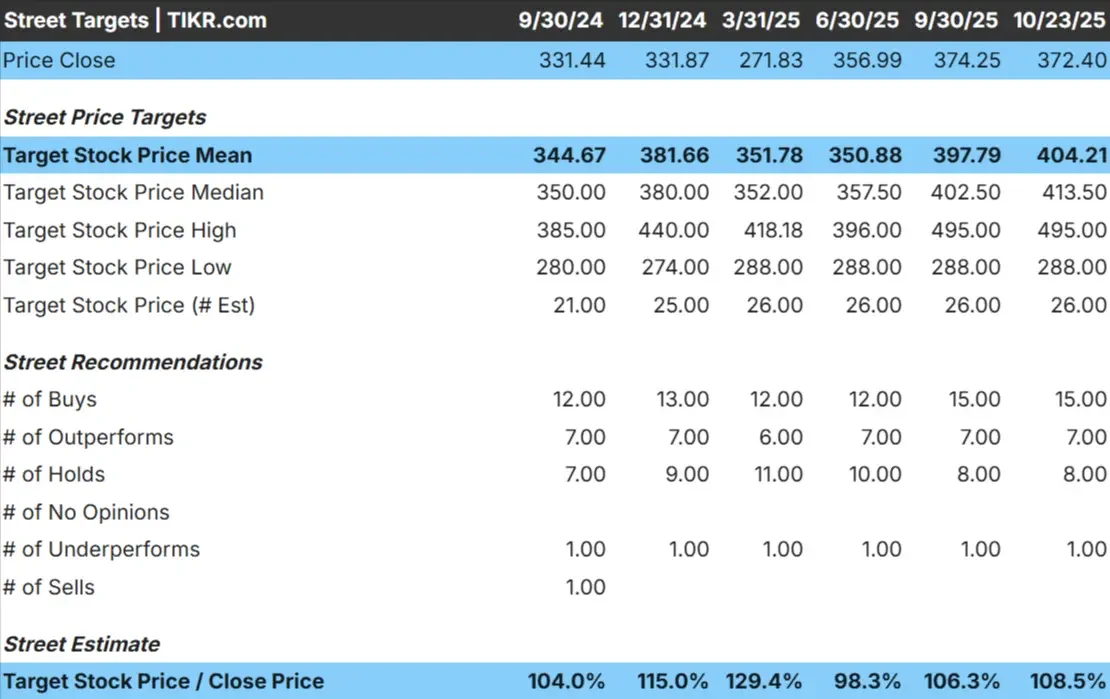

This article explores where Wall Street analysts think Eaton could trade by 2027. We have reviewed consensus targets and valuation models to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

Eaton trades near $372/share today. The average analyst price target is $404/share, pointing to around 9% upside over the next year. Forecasts remain relatively consistent across analysts, showing steady confidence in Eaton’s fundamentals:

- High estimate: ~$495/share

- Low estimate: ~$288/share

- Median target: ~$414/share

- Ratings: 15 Buys, 7 Outperforms, 8 Holds, 1 Underperform

It looks like analysts see modest upside potential, reflecting expectations for stable growth rather than a big breakout. For investors, Eaton continues to be viewed as a reliable compounder with strong exposure to long-term themes like electrification and aerospace, but most of the good news may already be priced in.

See analysts’ growth forecasts and price targets for Eaton Corporation (It’s free!) >>>

Eaton: Growth Outlook and Valuation

Eaton’s fundamentals remain solid and well-balanced:

- Revenue is expected to grow around 9% annually through 2027

- Operating margins are projected to reach roughly 22%

- Shares trade near 25x forward earnings, a premium to peers

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 25x forward P/E suggests the stock could reach about $446/share by 2027. That implies roughly 20% total upside, or around 8.5% annualized returns.

These projections show Eaton as a steady, high-quality compounder rather than a fast grower. Its pricing power, operational discipline, and balance sheet strength make it a dependable pick in the industrial space.

For investors, the takeaway is that Eaton offers consistent returns backed by real business momentum, though future gains may come more from earnings growth than multiple expansion.

Value stocks like Eaton Corporation in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Eaton continues to benefit from strong tailwinds in electrification, aerospace, and power management. Its electrical segment remains the main growth engine, driven by grid modernization, EV infrastructure, and renewable energy projects. Meanwhile, its aerospace business has seen solid momentum as commercial and defense activity rebounds.

Management’s focus on operational efficiency and high-return capital investments also strengthens Eaton’s long-term profile. Free cash flow remains healthy, allowing consistent reinvestment and shareholder returns.

For investors, these strengths suggest Eaton is well-positioned to ride major structural trends in global energy systems while maintaining reliable earnings growth and margin stability.

Bear Case: Valuation and Growth Ceiling

Even with these positives, Eaton’s valuation already reflects a lot of its success. The stock trades at a premium compared to peers, suggesting investors are paying up for its quality and consistency. If industrial activity cools or demand growth slows, that premium could make it harder for the stock to deliver strong returns.

Eaton is also tied to economic cycles in areas like construction and manufacturing, which can fluctuate with broader market conditions.

For investors, the main risk is that the stock’s strong fundamentals are already well recognized. Eaton is a world-class business, but its high expectations mean future gains could be limited if growth levels off.

Outlook for 2027: What Could Eaton Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 25x forward P/E suggests Eaton could trade near $446/share by 2027. That would represent about a 20% total return, or roughly 8.5% annualized gains from current levels.

While that marks a solid return profile, it already assumes steady execution and sustained demand in electrification and aerospace. To deliver stronger gains, Eaton would need to outperform expectations on earnings growth or margin expansion.

For investors, Eaton looks like a durable long-term compounder, offering steady performance built on real competitive advantages in energy and infrastructure.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.