Emerson Electric Co. (NYSE: EMR) has been on a strong run this year. Shares are up about 23% as industrial spending rebounds and demand for electrification, automation, and energy management accelerates. The company has been shifting toward higher-margin software and control systems, giving it a stronger growth profile than many traditional industrial peers.

Recently, Emerson completed a multi-year modernization project with Salt River Project, revamping excitation systems at four hydroelectric dams to improve operational efficiency and grid reliability. The company is also advancing its Sustainable Grid Solutions platform, delivering software and analytics for smarter renewable and distributed energy integration. These moves reflect how Emerson is evolving toward higher-value automation and grid software, reinforcing its exposure to long-term electrification and infrastructure trends.

This article explores where Wall Street analysts think Emerson could trade by 2027. We have combined consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Unlock our Free Report: 5 AI compounders that analysts believe are undervalued and could deliver years of outperformance with accelerating AI adoption (Sign up for TIKR, it’s free) >>>

Analyst Price Targets Suggest Modest Upside

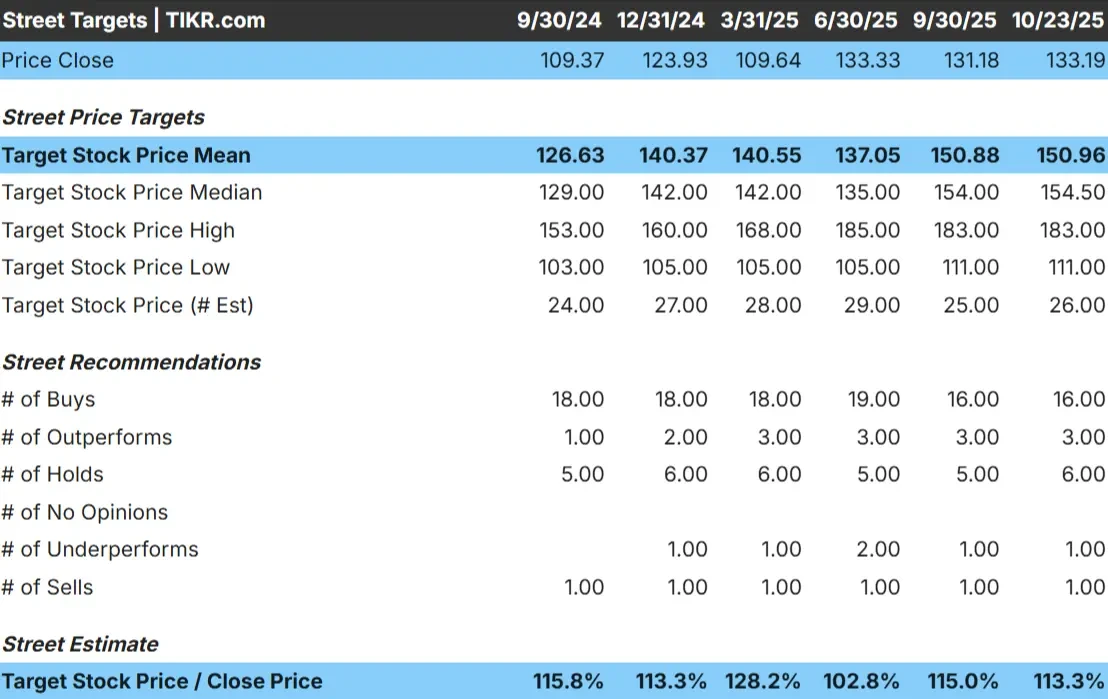

Emerson trades around $133/share today. The average analyst price target is $151/share, which points to about 13% upside over the next year. Forecasts remain relatively tight, showing moderate confidence in the company’s steady performance:

- High estimate: ~$183/share

- Low estimate: ~$111/share

- Median target: ~$155/share

- Ratings: 16 Buys, 3 Outperforms, 6 Holds, 1 Underperform, 1 Sell

With roughly 13% upside, analysts view Emerson as a solid but fairly valued compounder. For investors, the setup looks balanced. The stock could outperform if industrial demand holds up or if its automation and software portfolio drives stronger margin expansion than expected.

See analysts’ growth forecasts and price targets for Emerson Electric (It’s free!) >>>

Emerson: Growth Outlook and Valuation

The company’s fundamentals appear steady and well-supported by long-term trends in electrification and automation:

- Revenue growth expected around 4–5% annually through 2027

- Operating margin projected near 20%

- Shares trade at roughly 20x forward earnings, a slight premium to peers

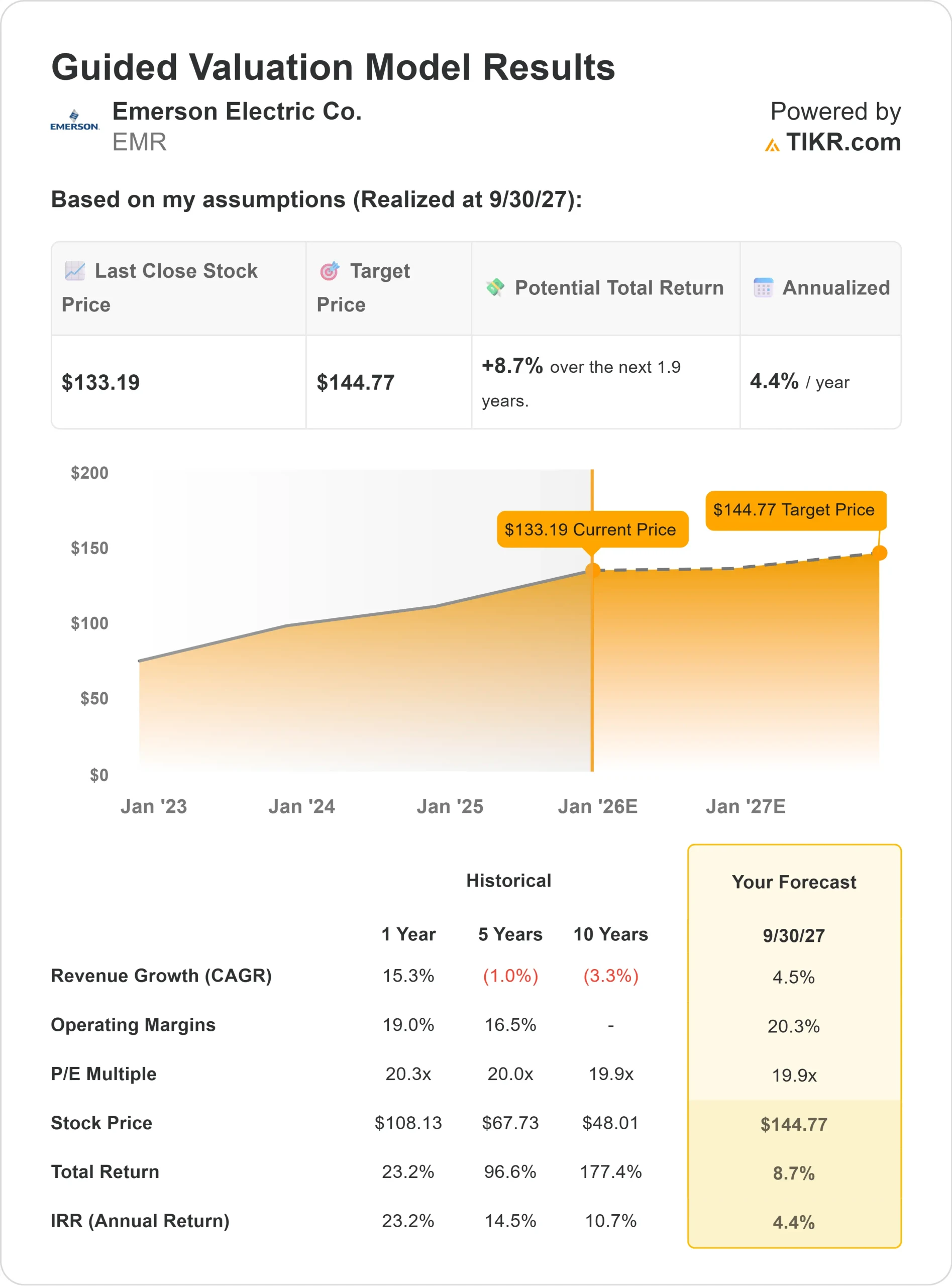

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19.9x forward P/E suggests about $145/share by 2027, implying roughly 9% total upside or around 4% annualized returns.

These figures show Emerson’s current strength is largely reflected in its valuation. For investors, it remains a dependable, cash-generating business, but future returns will likely track earnings growth rather than multiple expansion. Owning Emerson is about stability and compounding rather than chasing fast gains.

Value stocks like Emerson Electric in as little as 60 seconds with TIKR (It’s free) >>>

What’s Driving the Optimism?

Emerson’s shift toward higher-margin automation, software, and electrification continues to strengthen its long-term outlook. Its exposure to energy transition projects and grid modernization provides recurring demand that is less dependent on short-term industrial cycles.

The company’s disciplined cost management and operational efficiency are also translating into steady margin expansion. With a strong balance sheet and consistent free cash flow, Emerson is well-positioned to keep funding acquisitions and dividend growth.

For investors, these factors point to a high-quality business built for stability and gradual compounding. Emerson may not deliver explosive growth, but it has the foundation to keep performing through economic cycles.

Bear Case: Valuation and Growth Ceiling

Despite its strong execution, Emerson’s valuation already reflects much of its growth potential. The stock trades near 20x forward earnings, slightly above peers that offer similar fundamentals. If industrial demand softens or capital spending slows, earnings momentum could stall.

Another risk is that backlogs and government-driven energy projects may normalize sooner than expected, limiting revenue growth.

For investors, the concern is paying a premium for safety. Emerson remains a high-quality operator, but at current levels, upside appears limited unless growth meaningfully accelerates.

Outlook for 2027: What Could Emerson Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 19.9x forward P/E suggests Emerson could trade near $145/share by 2027. That represents roughly 9% total upside, or around 4% annualized returns.

While that implies modest gains, it already assumes solid execution and stable end-market demand. For Emerson to outperform, margins would need to expand faster or its software-driven portfolio would need to show stronger organic growth.

For investors, Emerson looks like a reliable long-term compounder. It is best suited for those prioritizing steady income, balance sheet strength, and consistent performance over high-growth potential.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Click here to sign up for TIKR and get your free copy of TIKR’s 5 AI Compounders report today.