Key Takeaways for Johnson & Johnson Stock

- Johnson & Johnson reported Q1 2026 worldwide revenue of $24.1 billion, a 10% year-over-year increase that beat consensus and prompted a guidance raise to a $100.2 billion full-year midpoint.

- Operating income reached $6.60 billion in Q1, supported by an operating margin of 27% against a gross margin of 66%.

- The company raised its adjusted diluted EPS guidance to a midpoint of $11.40, representing roughly 6% growth at the midpoint.

The launch data inside JNJ stock’s Q1 results is moving faster than Wall Street’s models reflect. Explore JNJ’s financials and new product ramp on TIKR for free →

Johnson & Johnson Stock Posts 10% Revenue Growth as New Launches Fill the STELARA Gap in Q1 2026

Johnson & Johnson (JNJ) reported Q1 2026 worldwide revenue of $24.1 billion following its April 14 earnings call, beating consensus while absorbing a 920-basis-point biosimilar headwind from STELARA, the company’s former immunology blockbuster now facing generic competition.

The company is a diversified healthcare giant operating across two segments: Innovative Medicine (pharmaceuticals) and MedTech (medical devices and surgical systems).

Excluding STELARA, Innovative Medicine grew at a double-digit rate in the quarter, underscoring how quickly new launches are absorbing the lost revenue.

CEO Joaquin Duato framed the result directly on Q1 earnings call: “We said 2026 would be a year of accelerated growth and impact for Johnson & Johnson, and with our strong Q1 performance, including our beat on consensus and raise guidance, you can see we are delivering on that promise.”

DARZALEX, the company’s multiple myeloma backbone therapy, generated $4 billion in sales with 18% operational growth.

TREMFYA, the company’s IL-23 immunology biologic, delivered 64% growth in the quarter, driven by continued share gains across psoriatic disease and an accelerating inflammatory bowel disease launch.

The highest-profile new product is ICOTYDE, an oral IL-23 peptide approved in March 2026 for plaque psoriasis that management described as potentially one of the company’s largest products ever, with early prescriber counts already above 1,500 in the first weeks post-launch.

INLEXZO, an intravesical drug-releasing device for high-risk non-muscle invasive bladder cancer, received its permanent reimbursement code in April, triggering a 90% surge in new patient insertions in the following weeks per management commentary on the call.

The company raised full-year 2026 operational sales guidance to a midpoint of $100.2 billion, aiming to cross the $100 billion annual revenue threshold for the first time.

ICOTYDE’s early uptake signals and TREMFYA’s 64% growth are the catalysts Wall Street is still sizing up. Pull JNJ’s complete product-level data and analyst estimates on TIKR for free →

JNJ’s Revenue Growth Is Accelerating, but Launch Investment Is Compressing Near-Term Margins

Johnson & Johnson’s revenue grew to $24.1 billion in Q1 2026, the fastest quarterly rate visible across the eight-quarter income statement.

Gross margin came in at 66%, matching the trough from a year earlier when the STELARA biosimilar headwind first hit revenue mix.

The Innovative Medicine segment carries structurally higher margins than MedTech, so the ongoing mix shift toward lower-margin revenues is a mechanical gross margin drag the income statement reflects directly.

Operating income reached $6.60 billion in the quarter, with an operating margin of 27%.

The gap between the 66% gross margin and the 27% operating margin reflects the cost of a multi-product launch cycle, with SG&A at $5.85 billion driven by heavy early-year investment behind ICOTYDE, INLEXZO, and CAPLYTA.

The trajectory to watch is whether TREMFYA and ICOTYDE revenue begins expanding gross margin back toward the 69% to 70% levels seen in higher-mix quarters as launch investment moderates.

JNJ Trades at a Gross Margin Discount to MRK and LLY While Pfizer’s Recovery Closes the Gap

Johnson & Johnson’s gross margin of 68% in the most recent annual period sits below both Merck (MRK) at 77% and Eli Lilly (LLY) at 83%, while Pfizer (PFE) at 76% has recovered sharply from a COVID-era trough to surpass JNJ by 8 points.

Pfizer’s trajectory is the most striking shift in the peer set, with PFE gross margin collapsing from 80% to 60% between 2021 and 2023 before recovering to 76%, a reversal driven by the wind-down of COVID product revenues and a return to the company’s legacy pharmaceutical mix.

Lilly’s 83% gross margin reflects the premium pricing of Mounjaro and Zepbound, high-margin GLP-1 assets with no direct analogue in JNJ’s portfolio, making LLY the aspirational ceiling rather than the relevant comparable.

Merck’s 77% gross margin is the most structurally relevant benchmark, as MRK operates a diversified pharmaceutical portfolio with a similar absence of a device segment pulling the blended rate lower.

JNJ’s MedTech business is the persistent structural drag that separates it from every pure-play pharmaceutical peer in this chart, and the STELARA biosimilar exit removed one of the highest-margin products from the Innovative Medicine mix at the same time.

The thesis rests on whether ICOTYDE and TREMFYA, both high-margin immunology assets, can shift the consolidated gross margin back toward the 70% range JNJ briefly reached in 2022, narrowing the Merck gap without the MedTech segment permanently capping the recovery.

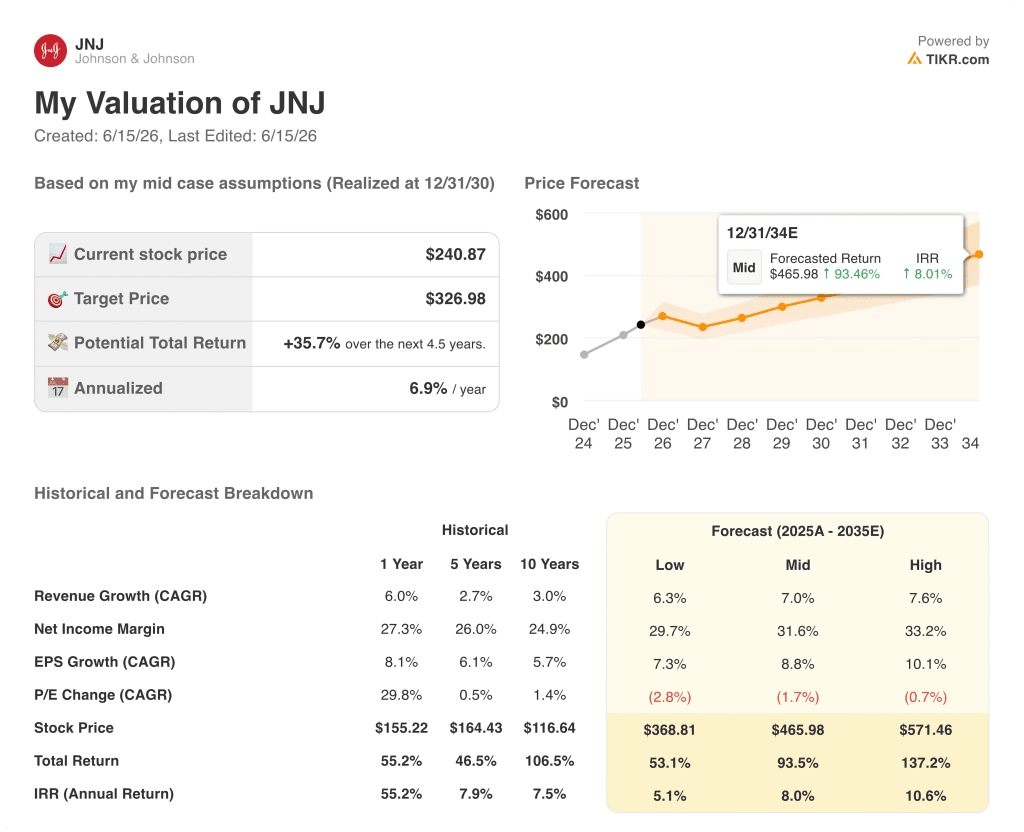

Is Johnson & Johnson Stock Undervalued in 2026? TIKR’s $327 Model Says the Pipeline Has to Hold

TIKR’s model values Johnson & Johnson at approximately $327 by December 2030, implying around 36% total return from the current price of $241, or roughly 7% per year.

That target is credible only if gross margin begins recovering as ICOTYDE and TREMFYA revenue scale and early-year launch investment moderates, the exact mechanism the income statement is currently suppressing.

If front-loaded SG&A converts to durable top-line growth without a permanent step-up in operating expenses, the 27% operating margin visible today is likely the floor, not the ceiling.

The TIKR model is built on assumptions you can interrogate yourself. Run your own valuation on JNJ stock on TIKR for free →

Should You Invest in Johnson & Johnson?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Johnson & Johnson stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Johnson & Johnson alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze JNJ stock on TIKR for Free →

Does Johnson & Johnson pay a dividend?

Johnson & Johnson raised its quarterly dividend 3% to $1.34 per share in April 2026, marking the 64th consecutive year of dividend growth, at an annualized rate of $5.36 per share.