Key Stats for Illumina Stock

- Past-Week Performance: 2%

- 52-Week Range: $69 to $156

- Current Price: $118

What Happened to Illumina Stock?

Illumina (ILMN) shares closed at $117.67 yesterday, though the stock had surged as high as $151 in mid-January when the company simultaneously previewed a Q4 revenue beat, announced the Billion Cell Atlas with AstraZeneca, Merck, and Eli Lilly, and completed the $350 million SomaLogic acquisition within the same three-week window.

On February 5, Illumina reported Q4 adjusted EPS of $1.35, clearing the $1.23 consensus estimate by nearly 10%, while Q4 revenue of $1.16 billion topped expectations of $1.10 billion and clinical consumables grew 20% ex-China, marking the second highest NovaSeq X placement quarter since the platform’s 2023 launch.

The outperformance was anchored by accelerating clinical adoption of sequencing-based diagnostics, particularly the shift from whole exome to whole genome sequencing in oncology and rare disease, which drove sequencing consumables revenue to $755 million and pushed total sequencing gigabase output on connected instruments more than 30% higher year-over-year.

Taken together, the earnings beat, the SomaLogic close, the CMS reimbursement of TruSight Oncology Comprehensive at $2,989.55 per test on January 20, and the Billion Cell Atlas pharma partnerships repositioned Illumina from a company managing a difficult high-throughput platform transition to one actively expanding into proteomics, spatial transcriptomics, and AI-driven drug discovery.

CEO Jacob Thaysen stated on the Q4 2025 earnings call that “the momentum we have built going into 2026 gives me high confidence that the strategy we put in place in 2024 to return to long-term growth is working,” citing 20% clinical consumables growth ex-China and full-year non-GAAP EPS of $4.84 beating original guidance.

Wall Street’s median 12-month price target sits at $131.00, roughly 11% above the February 20 close of $117.67, with the current analyst breakdown at 8 buys, 9 holds, and 3 sells against a peer group average recommendation of buy.

Beyond 2026 guidance of $4.5 billion to $4.6 billion in revenue and $5.05 to $5.20 in EPS, Illumina’s convergence of core sequencing, multiomics via SomaLogic, and BioInsight’s pharma data subscriptions points toward the company’s 2027 targets of high single-digit growth and approximately 26% operating margins as increasingly within reach.

Wall Street’s Take on Illumina Stock

Illumina’s Q4 beat, the SomaLogic close, the CMS reimbursement win for TruSight Oncology Comprehensive, and the Billion Cell Atlas pharma alliances collectively signal that the company’s three-pillar strategy is producing revenue-level results, not just pipeline promises.

The fundamental case rests on a clear earnings recovery trajectory, with normalized EPS climbing from $0.86 in 2023 to $4.84 in 2025 and consensus estimates projecting $5.13 for 2026, representing nearly a 6% year-over-year gain as clinical consumables sustain double-digit to mid-teens growth.

Wall Street’s mean price target currently stands at $135.84 across 19 analysts, sitting roughly 15% above the February 20 close of $117.67, with 8 buys, 8 holds, and 3 underperforms or sells reflecting a cautiously improving but still divided consensus.

The analyst target range spans from a low of $80.00 to a high of $170.00, a $90 spread that captures genuine disagreement over how quickly China normalizes, whether research funding recovers, and how fast SomaLogic becomes accretive.

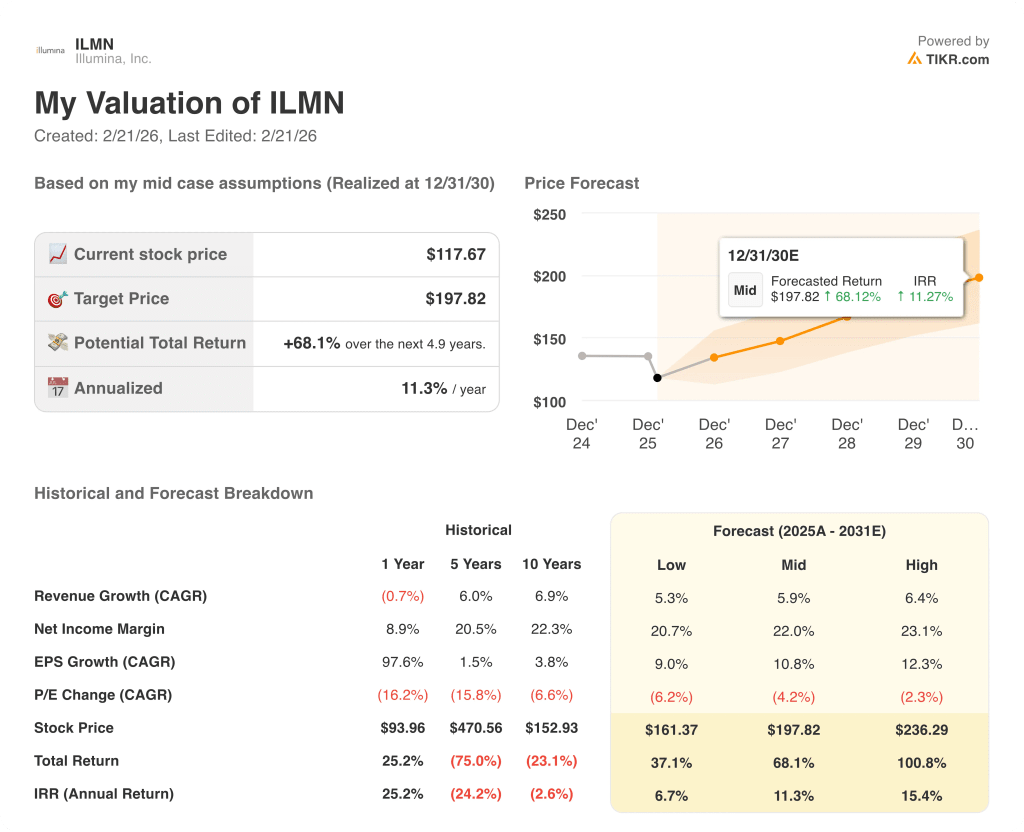

What Does the Valuation Model Say?

Building on the SomaLogic integration and BioInsight’s early pharma traction, a mid-case TIKR valuation model prices ILMN at $198 by December 2030, implying a 68.1% total return and an annualized IRR of 11.3% from the current price of $117.67.

The primary risk is multiple compression, as ILMN already trades at 26x forward earnings while research end-markets remain pressured by NIH funding uncertainty and China contributes only $210 million to $220 million in 2026 revenue with instrument sales constrained by the Unreliable Entities List designation.

At $117.67, Illumina looks undervalued relative to both its $135.84 mean analyst target and its $197.82 model fair value, but the discount is justified until SomaLogic dilution fades, research spending stabilizes, and BioInsight converts pharma interest into recurring subscription revenue.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.