Key Stats for HubSpot Stock

- This Week Performance: 15%

- 52-Week Range: $207.2 to $732

- Current Price: $268.5

What Happened?

HubSpot stock‘s 9.3% single-session surge to $268.5 yesteday signals that the market is finally pricing in what the numbers have been saying for quarters: this is no longer a CRM company but an AI-native growth platform with genuine enterprise momentum.

The immediate trigger was a 13-firm analyst repricing on February 12, where even the most aggressive cuts, including RBC slashing its target from $800 to $400 and Needham from $700 to $300, still implied significant upside against a stock trading near multi-year lows.

Beneath the target resets, the mechanical story is Q4 revenue growing 20% to $846.8 million, beating the $830.5 million consensus, while adjusted EBIT of $191 million cleared estimates by $7.2 million and operating margin expanded 4 points year-over-year to 22.6%.

However, the market’s mental model of HubSpot is shifting from a seat-based SaaS company toward a consumption-driven AI platform, supported by over 10,000 Prospecting Agent activations, 8,000 Customer Agent deployments, and a credit monetization layer that management expects to outpace revenue growth through fiscal 2026.

CEO Yamini Rangan stated on the Q4 earnings call that “one of the leaders in vibe coding is using you intelligence the power of that,” contextualizing how AI-native companies like Lovable are choosing HubSpot as their go-to-market platform, directly rebutting disruption fears circulating across the software sector.

Reinforcing institutional conviction, JP Morgan maintained a buy-equivalent stance with a $530 target while Morgan Stanley held at $405, both absorbing significant cuts yet still pricing in 97% and 50% upside respectively from the February 10 close of $231.95.

Looking out 3 to 5 years, HubSpot’s position as the most visible CRM in LLM-generated answers, combined with net new ARR growing 24% and outpacing revenue growth for six consecutive quarters, signals a durable compounding engine that increasingly resembles the early trajectory of today’s large-cap SaaS incumbents.

Wall Street’s Take on HUBS Stock

HubSpot’s Q4 revenue beat and $1B share buyback authorization confirm that the company’s AI-native platform transition is accelerating forward estimates, with FY2026 revenue guidance of $3.7B implying continued 18% growth despite broad software sector pressure.

The fundamental case strengthens further as forward estimates show FY2026 EBITDA expanding 21.8% to $870M at a 23.7% margin, while normalized EPS grows 28.4% to $12.5, marking a clear acceleration from FY2025’s 19.5% EPS growth.

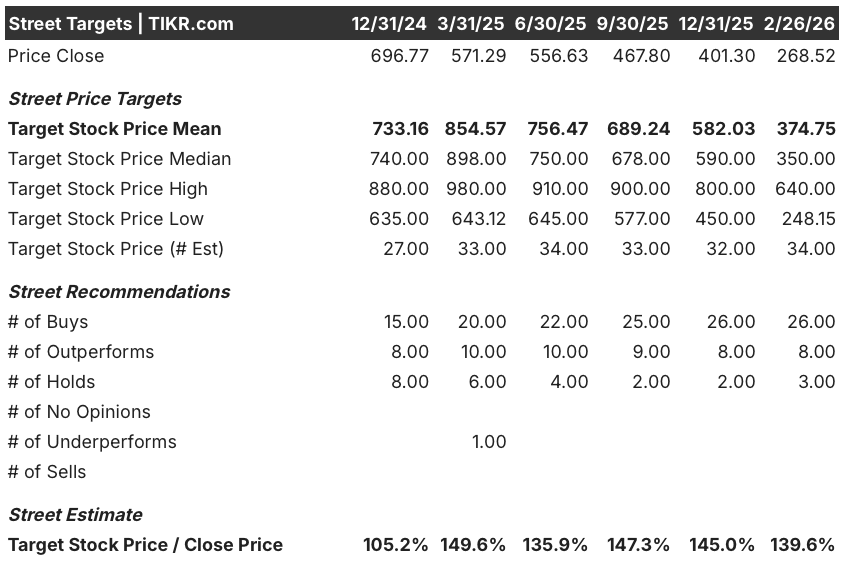

Wall Street stands firmly bullish with 26 buys, 8 outperforms, and just 3 holds against a mean price target of $374.8, implying 39.6% upside from the current $268.5, with analysts holding conviction despite a stock trading 63.3% below its 52-week high.

The analyst target spread between $248.2 on the low end and $640.0 on the high end reflects a binary setup where credit monetization scaling and upmarket acceleration drive the bull case, while multiple compression and AI disruption fears anchor the bear scenario.

What Does the Valuation Model Say?

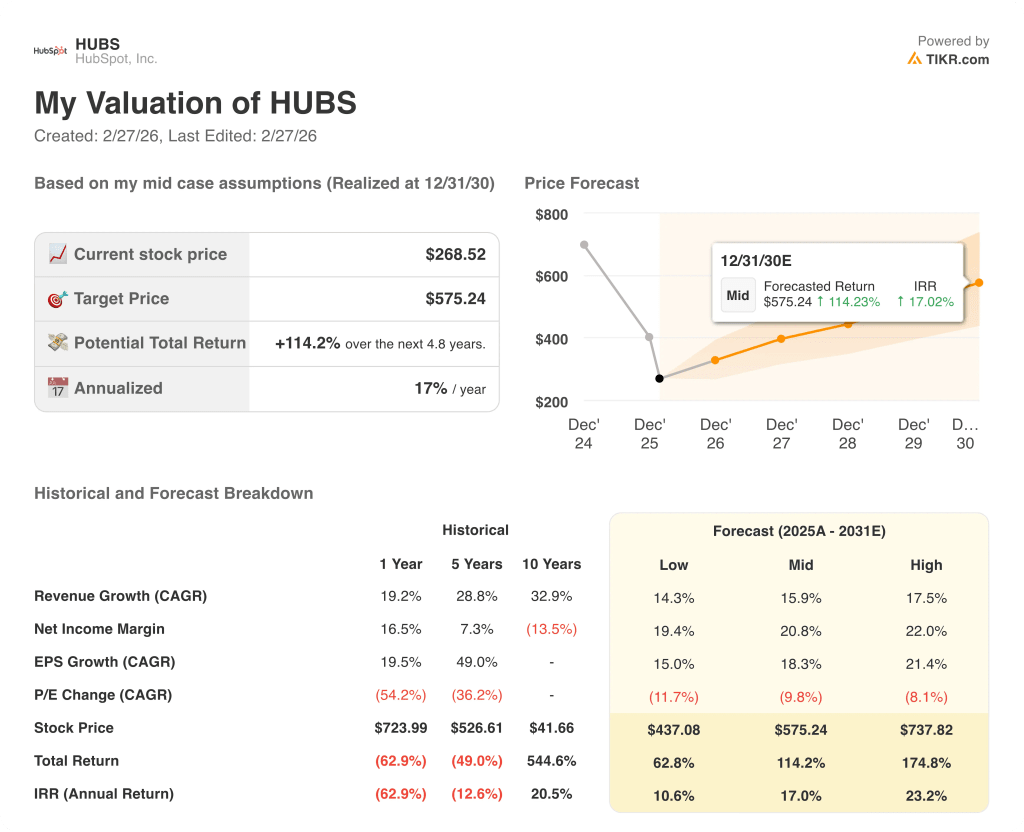

Given HubSpot’s six consecutive quarters of net new ARR outpacing revenue growth and its emerging credit consumption layer, the mid-case valuation model prices HUBS at $575.2, implying a 114.2% total return and a 17.0% annualized IRR through December 2030.

The most consequential risk remains P/E multiple compression, already contracting from 44x three months ago to 20x today, a trend that could continue pressuring the stock even as underlying fundamentals accelerate toward the model’s projected $12.5 EPS for FY2026.

HUBS looks undervalued at $268.5 given its 39.6% analyst upside, accelerating EPS trajectory, and a mid-case model projecting 17.0% annualized returns, with credit monetization scaling and FY2026 margin expansion serving as the key inflection points to watch.

Should You Invest in HubSpot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HUBS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HubSpot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HUBS stock on TIKR for Free →