Key Stats for Domino’s Stock

- Past-Week Performance: +1.5%

- 52-Week Range: $370.7 to $449.1

- Current Price: $408.4

What Happened?

Berkshire Hathaway raised its Domino’s (DPZ) stake 12.3% to 3.4 million shares in Q4 2025, validating a pizza chain that just posted its 32nd consecutive year of international same-store sales growth while trading at $408.41.

On February 23, Domino’s reported Q4 revenue of $1.54 billion, beating the $1.52 billion consensus, as its “Best Deal Ever” value promotion and Parmesan Stuffed Crust drove U.S. same-store sales 3.7% higher against an analyst estimate of 3.5%.

Free cash flow surged 31.2% to $671.5 million for full-year 2025, fueled by 3% U.S. same-store sales growth and 172 net new U.S. stores, outpacing every public QSR brand with over 3,000 units in net store growth since 2019.

On February 24, JP Morgan upgraded DPZ to “Overweight,” citing a franchise network so resilient that only 23 of 7,186 U.S. stores closed over the past three years, while a struggling unnamed national competitor announced up to 250 closures in H1 2026.

CEO Russell Weiner stated on the Q4 2025 earnings call that “our growth prospects have never been greater because our brand has never been stronger,” then relaunched Best Deal Ever the same day and guided for 3% U.S. same-store sales growth in 2026.

With Domino’s Rewards loyalty membership up nearly 20% to 37.3 million active users since its 2023 relaunch, DoorDash still below fair-share penetration, a new e-commerce platform live, and $459.7 million remaining in buyback authorization, the company’s self-described path to doubling U.S. retail sales from roughly $10 billion is backed by compounding operational infrastructure, not projection alone.

Wall Street’s Take on DPZ Stock

Berkshire’s 12.3% stake increase to 3.4 million shares in Q4 2025 lands against a stock trading 17.2% below the analyst mean price target of $478.58, suggesting institutional money sees a disconnect the market has not yet closed.

Revenue grew 5% to $4.94 billion in FY2025 and consensus estimates project a 7.0% acceleration to $5.28 billion in FY2026, reflecting confidence that the Best Deal Ever relaunch and DoorDash expansion compound the base rather than replace it.

Domino’s EBITDA also grew from $970 million in FY2024 to $1.04 billion in FY2025, and in a franchise model where royalty income scales directly with system sales volume, expanding EBITDA margins from 20.5% to 21.1% on flat pricing confirms Domino’s stock is growing more profitable per dollar of revenue, not just growing bigger.

Free cash flow surging 31.2% to $671.5 million while pricing stayed flat proves Domino’s stock is extracting margin through volume and procurement leverage, not price increases, a durability signal that most QSR peers cannot currently replicate.

Eighteen analysts rate DPZ a buy or outperform, 13 hold, and just 2 assign underperform or sell ratings, with a mean price target of $478.58 implying 17.2% upside from the March 6 close of $408.41, a consensus that has held firm even as the stock drifted 15.6% lower over the past year.

The spread between the $340 low target and the $601 high target reflects a genuine fork: bears anchor on DPE’s international drag and insurance cost pressure, while bulls price in the Best Deal Ever relaunch, DoorDash fair-share gap, and 175-plus net new U.S. stores in FY2026.

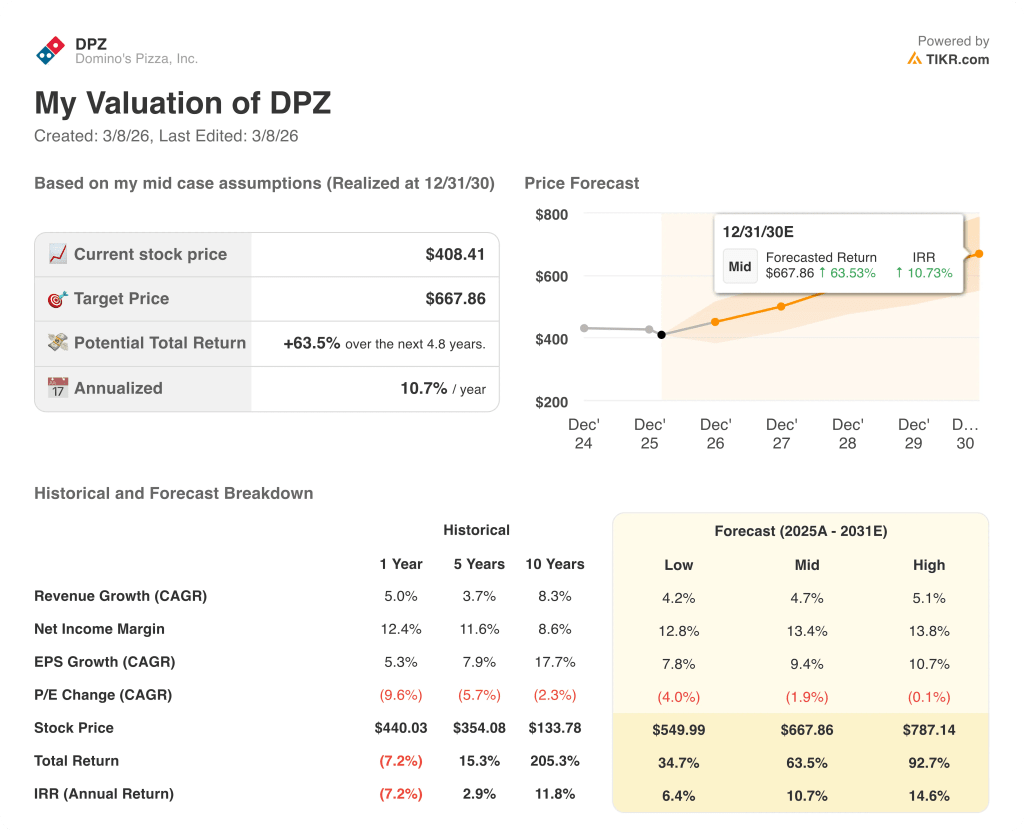

What Does the Valuation Model Say?

The TIKR mid-case model prices DPZ at $667.86 by December 31, 2030, implying a 63.5% total return and a 10.7% annualized IRR, driven by a 4.7% revenue CAGR and net income margins expanding from 12.4% to 13.4% as supply chain procurement productivity offsets food basket inflation.

The model’s margin expansion assumption is directly supported by management’s FY2026 guidance for operating income growth of approximately 8% alongside only low single-digit food basket increases, meaning the profitability lever is procurement efficiency, not pricing.

The market is pricing DPZ at 20x forward earnings, down from 21x three months prior, despite EPS accelerating from $17.57 in FY2025 to a consensus estimate of $19.83 in FY2026, a 12.9% growth rate the current multiple does not reflect.

The 37.3 million active Domino’s Rewards loyalty members, up nearly 20% since the 2023 relaunch, provide the recurring order volume base that justifies the TIKR model’s assumption of sustained, compounding same-store sales growth through 2030.

CEO Russell Weiner’s same-day relaunch of Best Deal Ever on February 23 signals management’s confidence that the value promotion, which drove positive order counts across all income cohorts in FY2025, remains the primary volume engine heading into a pressured 2026 macro environment.

The key risk is DPE, the Domino’s Pizza Enterprises franchise covering Australia and key Asian markets, where continued underperformance has already dragged international SSS below the 3% long-term algorithm and could pressure the TIKR model’s 4.7% revenue CAGR if a turnaround under new CEO Andrew Gregory stalls.

Q1 2026 same-store sales results will be the first read on whether Best Deal Ever’s relaunch and DoorDash expansion can offset January weather disruptions and sustain the 3% U.S. comp guidance, the single input that anchors the entire TIKR forward model.

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DPZ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Domino’s Pizza, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DPZ stock on TIKR for Free →