Key Stats for Home Depot Stock

- Past-Week Performance: -6%

- 52-Week Range: $ 326.3to $426.8

- Current Price: $357.9

What Happened?

Home Depot (HD), the world’s largest home improvement retailer, just beat Q4 adjusted EPS expectations by $0.18 and delivering $2.72 against a $2.54 estimate while a frozen U.S. housing market has kept the stock 16% below its 52-week high of $426.75.

On February 24, Q4 earnings showed comparable sales rising 0.4%, topping the flat consensus, as Pro customers — contractors and builders who drive large, recurring job-site orders — posted positive comps and outperformed the DIY segment.

Pro customers drove the quarter even as the roofing industry hit its worst quarterly volume since 2019, with SRS, Home Depot’s specialty building materials subsidiary, still gaining market share through the slump.

CFO Richard McPhail stated on the Q4 2025 earnings call that “we have not yet seen a catalyst for an inflection in housing activity,” even as the company affirmed fiscal 2026 guidance calling for total sales growth of 2.5% to 4.5%.

Home Depot’s investment in its Pro ecosystem, including an AI-powered project planning tool generating tens of thousands of weekly sessions and real-time big and bulky delivery tracking launching by end of Q1, positions the company to capture a $200 billion white space in professional contractor spending before housing turnover recovers.

Wall Street’s Take on HD Stock

Home Depot’s Q4 beat of $2.72 adjusted EPS against a $2.54 estimate confirms the Pro-driven model is holding ground even as the U.S. housing market sits near 30-to-40-year turnover lows.

Management guided fiscal 2026 EPS growth of flat to 4%, but TIKR’s consensus estimate prices in a 1.5% EPS decline for the year, meaning the Street is not yet convinced housing pressure eases fast enough to validate that target.

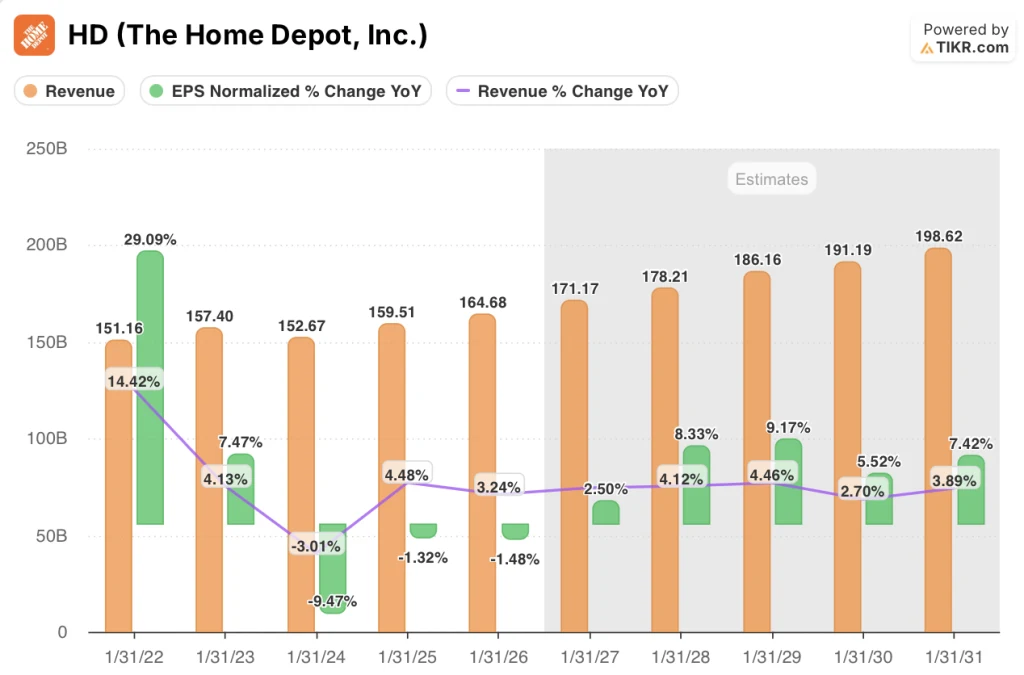

Revenue tells a steadier story: TIKR projects $171.2 billion in fiscal 2027 and $178.2 billion in fiscal 2028, reflecting 3.9% and 4.1% growth respectively, as SRS organic sales and roughly 15 new store openings layer incremental volume onto the base.

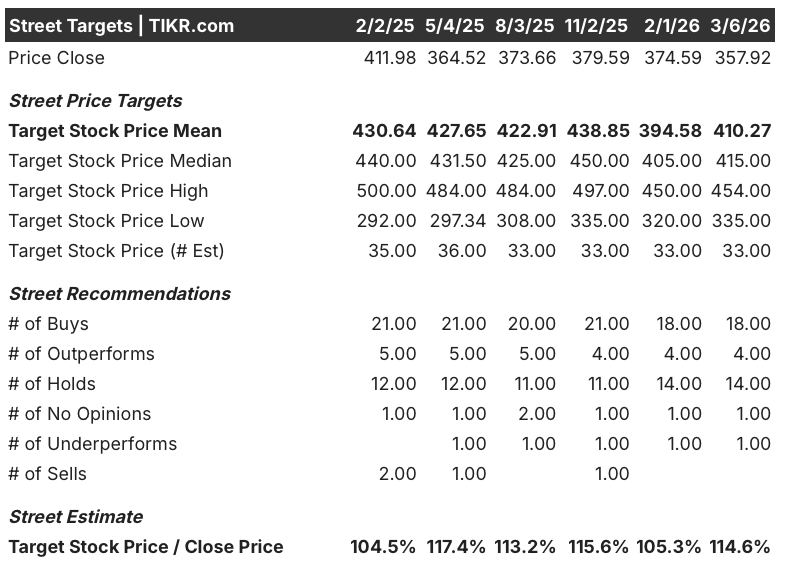

Despite the EPS skepticism, 22 of 33 analysts with active price targets rate HD a buy or outperform, with a mean target of $410.27 implying 14.6% upside from $357.92, suggesting the Street sees execution quality even without a housing recovery priced in.

The spread between the $454 bull target from Jefferies and the $335 bear floor maps directly to one variable: whether housing turnover, currently at multi-decade lows, inflects before the end of fiscal 2026 or stays frozen through it.

What Does the Valuation Model Say?

TIKR’s mid-case model prices HD at $548.70 by January 2031, implying a 53.3% total return and a 9.1% annualized IRR. That target assumes a 3.8% revenue CAGR and net income margins recovering from 8.9% today to 9.5% by fiscal 2031.

The margin recovery assumption is the tension point: TIKR’s model requires net income margins to expand even as management guided gross margin down to 33.1% in fiscal 2026 from 33.3% in fiscal 2025, pressured by the full-year annualization of GMS.

The market is pricing HD as a pure housing proxy, but the Pro ecosystem, contractors and builders driving large recurring job-site orders, delivered positive comps in Q4 while the broader DIY segment remained under pressure.

The AI-powered project planning tool generating tens of thousands of weekly sessions and Two Sigma delivery reliability achieved in fiscal 2025 give HD measurable operational proof that Pro stickiness is compounding before any housing recovery begins.

CFO McPhail confirmed share repurchases are expected to resume in the first half of 2027, a capital return signal the current price of $357.92 does not reflect and one that directly supports EPS re-acceleration in the model’s outer years.

The risk is that consumer uncertainty deepens: management explicitly cited job concerns, elevated financing costs, and economic anxiety as the reason big-ticket discretionary projects remain under pressure, which would push EPS contraction beyond fiscal 2026 and break the model’s margin recovery assumption.

The Q1 2026 earnings call in May is the first real test: management guided mid-single-digit percentage negative EPS growth for Q1, so watch whether U.S. comps hold positive and whether Pro order volumes show the trough is passing.

Should You Invest in The Home Depot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HD stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Home Depot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HD stock on TIKR for Free →