Key Stats for Disney Stock

- Past-Week Performance: -4%

- 52-Week Range: $ to $

- Current Price: $

What Happened?

Disney (DIS), the global entertainment and theme park conglomerate, turned its streaming business from a $4 billion annual loss three years ago into a 10% margin target for FY2026, while its Experiences segment crossed $10 billion in quarterly revenue for the first time.

On February 2, Disney reported Q1 FY2026 results showing streaming revenue growth of 12% and earnings growth of approximately 50%, with CFO Hugh Johnston reiterating double-digit EPS growth guidance for both FY2026 and FY2027 at the March 2 Morgan Stanley conference.

Disney’s film studio generated more than $6.5 billion at the global box office in calendar 2025, its third biggest year ever, with Zootopia 2 becoming Hollywood’s highest-grossing animated film of all time at $1.7 billion, and four major theatrical releases still ahead in FY2026.

Hugh Johnston, CFO, stated at the Morgan Stanley Technology, Media and Telecom Conference on March 2 that “if you think about it, buy some Disney stock, too. It’s not a bad idea and a pretty good buy these days,” tying the remark directly to the company’s $7 billion share buyback program and double-digit EPS growth trajectory.

With Josh D’Amaro taking over as CEO and Dana Walden as President and Chief Creative Officer around March 18, the Mandalorian, Toy Story 5, Devil Wears Prada 2, and Moana releasing in FY2026, and a $60 billion Experiences expansion underway, Disney’s three-segment flywheel enters fresh leadership with momentum across every business line.

Wall Street’s Take on DIS Stock

The streaming inflection that drove normalized EPS from $3.53 in FY2022 to $5.93 in FY2025 is now compounding into the Experiences and film businesses simultaneously, creating a multi-segment earnings acceleration the stock has not yet priced in.

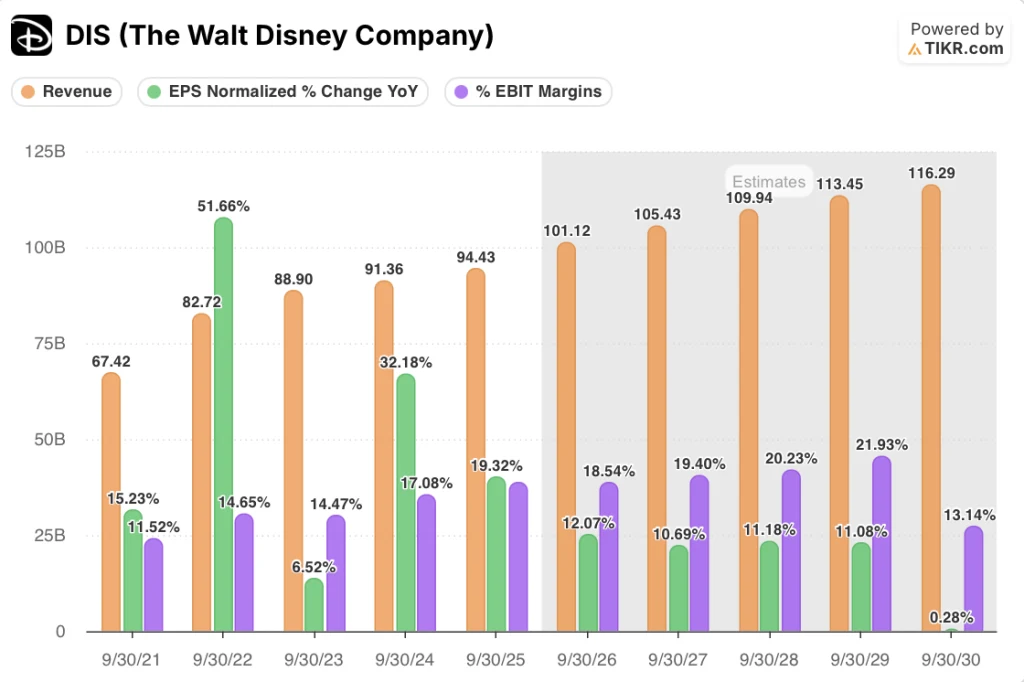

TIKR estimates put FY2026 revenue at $101.1 billion, up 7.1% year-over-year, with EBIT margins expanding to 18.5% from 18.6% in FY2025, while normalized EPS grows another 12.1% to $6.65 as the double-digit EPS guidance plays out.

Of 31 analysts covering Disney as of March 6, 20 rate it a Buy, 6 an Outperform, 4 a Hold, and 1 a Sell, with a mean price target of $130.30, implying 28.3% upside from the current price of $101.54.

The spread between the low analyst target of $77.00 and the high of $160.00 reflects diverging views on CEO transition risk and the streaming growth runway, with the bull case anchored to the FY2026 film slate and the $60 billion Experiences expansion.

What Does the Valuation Model Say?

TIKR’s mid-case target of $137.72 implies 35.6% total return over approximately 4.6 years, pricing in a 4.3% revenue CAGR and net income margin expansion to 12.4%, well below Disney’s 10-year historical peak of 16.8%.

The market is pricing Disney as a mature media company, but normalized EPS grew 19.3% in FY2025 alone, a growth rate inconsistent with the stock trading 19% below its 52-week high of $124.69.

The Experiences segment crossing $10 billion in quarterly revenue for the first time, combined with full-year bookings up 5%, directly justifies the TIKR model’s assumption of sustained mid-single-digit revenue growth through FY2030.

CFO Hugh Johnston’s unsolicited buy recommendation at the March 2 Morgan Stanley conference, backed by a $7 billion share repurchase program, signals that management views $101.54 as a material discount to intrinsic value.

The CEO transition to Josh D’Amaro around March 18 is the single execution risk that breaks the model if strategic continuity fractures, because the double-digit EPS guidance for FY2027 depends on the film slate and Experiences expansion proceeding without disruption.

Disney’s Q2 FY2026 earnings report is the next confirmation point: $500 million in SVOD operating income and approximately 5% Experiences revenue growth would validate the TIKR model’s margin expansion trajectory and the double-digit EPS target for the full year.

Should You Invest in The Walt Disney Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DIS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Walt Disney Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DIS stock on TIKR for Free →