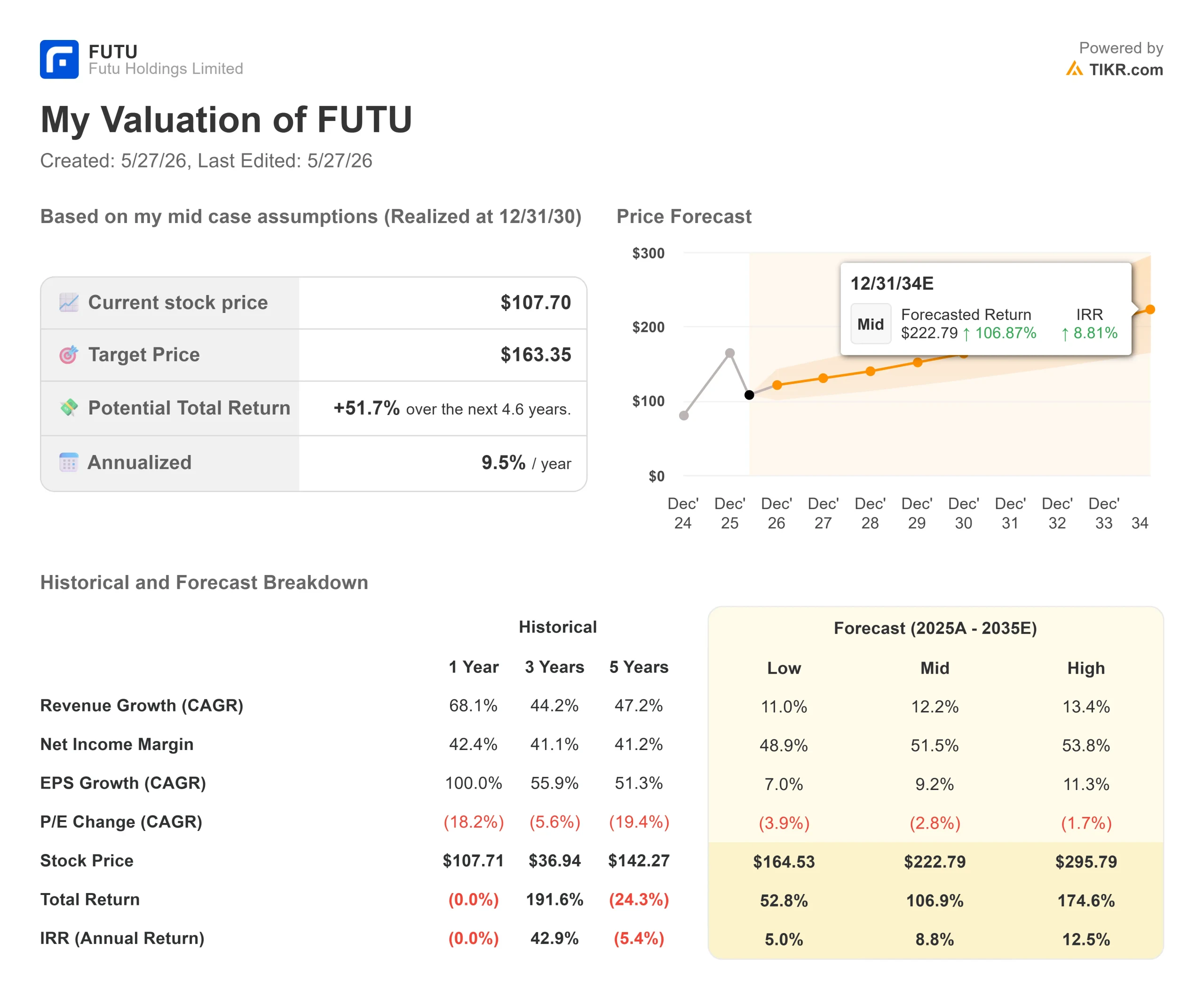

Key Stats for Futu Holdings Stock

- Current Price: $107.70

- Target Price (Mid): ~$163

- Street Target: $198.42

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

- Earnings Reaction (Q4 2025, reported 3/12/26): -1.31%

- Max Drawdown: -54.90% on 5/22/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

One Session Changed Everything

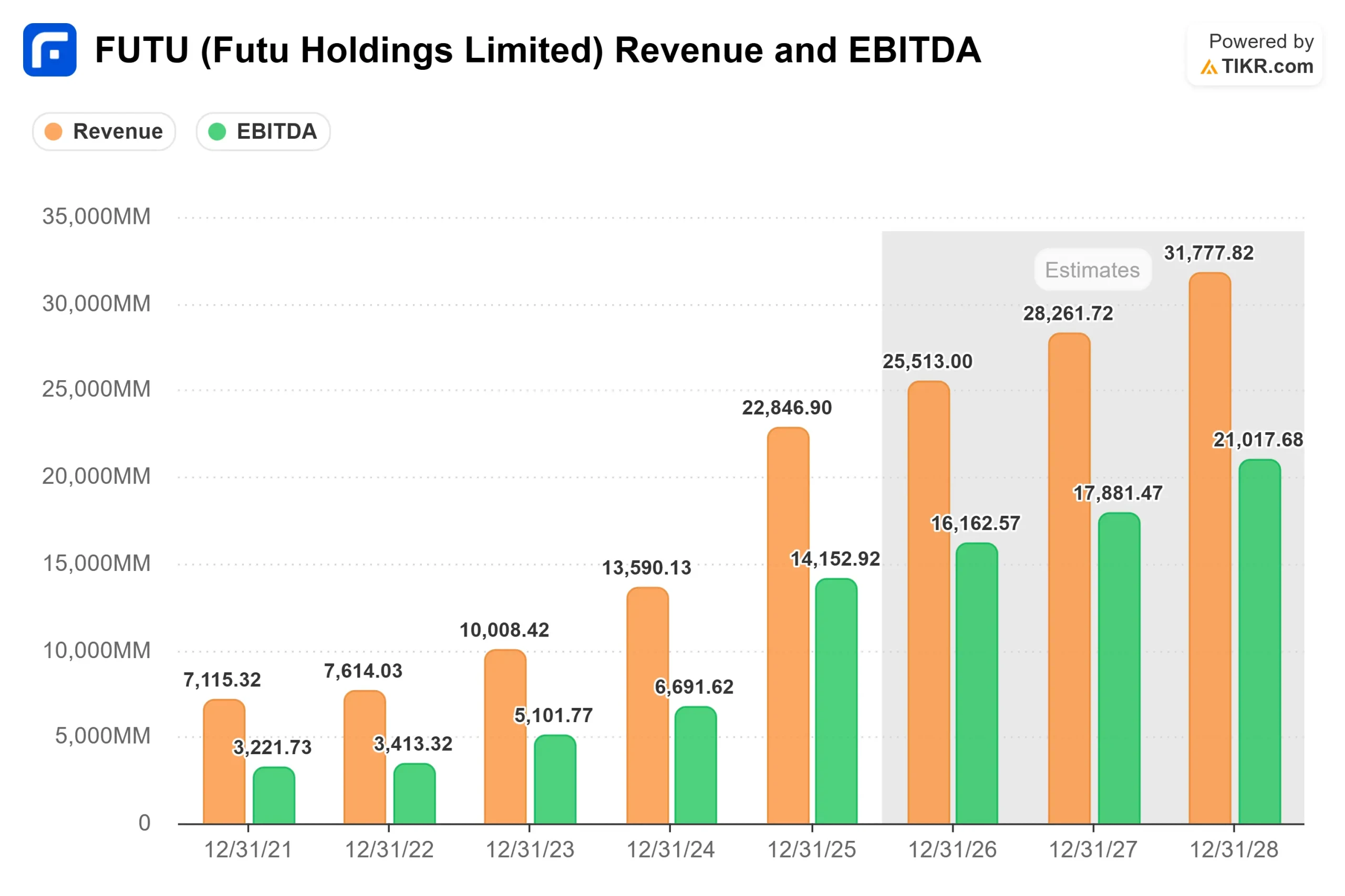

Futu Holdings (FUTU) spent 2025 delivering one of the strongest growth records in Asian fintech. Revenue grew 68% to HKD 22.8 billion. Full-year net income more than doubled. The company added over 950,000 net new funded accounts. Then came May 22, 2026.

That day, China’s securities regulator, the China Securities Regulatory Commission (CSRC), along with seven other government agencies, announced formal penalty proceedings against Futu and two rival offshore brokerages. The CSRC alleged that certain Futu entities conducted securities, fund sales, and futures business in mainland China without the required licenses, proposing penalties totaling approximately RMB 1.85 billion (around $271 million) and ordering the related companies to rectify or cease such activities. A mandatory two-year wind-down restricts existing mainland users to selling and withdrawing only, with a full shutdown of mainland-facing apps to follow. A proposed personal fine for CEO Li Hua was also included. These remain proposals, not final determinations.

The sell-off that followed was one of the steepest single-session drops in FUTU’s history, with shares plunging roughly 31%. JPMorgan cut to Neutral and slashed its target from $300 to $87. Goldman Sachs also cut to Neutral, lowering its target from $210.47 to $102.13 and trimming revenue forecasts for 2026, 2027, and 2028 by 16%, 14%, and 14%, respectively.

By May 26, FUTU had bounced back to $107.70 after Futu announced it had deployed $160 million in share repurchases under its existing $800 million buyback program. Even so, FUTU sits 46.8% below its 52-week high of $202.53, with Q1 2026 earnings due tomorrow morning.

See historical and forward estimates for Futu Holdings stock (It’s free!) >>>

The 13% Figure Is the Whole Argument

Futu disclosed that as of Q1 2026, funded accounts from mainland China represented approximately 13% of its total, and that operations across all regions outside mainland China remain normal, with overseas accounts continuing to grow.

This did not happen by accident. On the Q4 2025 earnings call, CFO Arthur Chen confirmed that Malaysia and Hong Kong together contributed more than 50% of new client additions in Q4, with Japan, Singapore, and the U.S. each contributing between 10% and 20%. The Moomoo platform was the most downloaded trading app in Australia in 2025 and reached 2 million cumulative downloads in Japan.

TIKR segment data shows international revenues (countries other than Hong Kong) grew from HKD 1,323.25 million in 2024 to HKD 2,746.81 million in 2025, roughly 108% year-over-year, outpacing even Hong Kong’s already strong growth. The regulatory action removes a meaningful but not a majority slice of the business.

The harder question is whether those 13% of mainland accounts represent a larger share of revenue than their headcount implies, particularly through margin trading and high-frequency activity. That is what tomorrow’s Q1 report will begin to answer.

What the Q4 Call Reveals

CFO Chen confirmed on the Q4 call that Chinese ADRs (American Depositary Receipts of mainland-based companies listed in the U.S.) made up less than 10% of U.S. stock trading volumes in Q4, down from around 10% in Q3. The concern that FUTU is a proxy trade on Chinese equities has been quietly dismantled by its own data. As Daniel Yuan, Chief Staff to CEO, noted on the call, clients were diversifying “beyond large technology names into a broader range of sectors and across the AI value chain,” with U.S. stock trading turnover reaching HKD 3 trillion in Q4, up 17% sequentially.

Management guided, before any regulatory action landed, that Q1 2026 net asset inflows would post a “double-digit sequential increase” and set a new company record. That implies the underlying business was healthy heading into the quarter.

Wealth management is the other undercovered story. Client assets in that segment reached HKD 179.6 billion in Q4, up 62% year-on-year. CFO Chen said the long-term revenue mix would skew toward fee income from wealth management, a less volatile and more recurring revenue stream than brokerage commissions.

Valuation: Distress or Opportunity?

Before the crash, FUTU traded at an NTM (next twelve months) P/E of around 11.3x. At $107.70, that multiple has compressed to 8.76x. This is a business with an LTM (last twelve months) gross margin of 94.4% and an LTM return on equity of 33.1%. It has beaten consensus revenue estimates in each of the last four quarters, including Q4 2025 actual revenue of HKD 6,438.47 million against a consensus estimate of HKD 6,302.01 million, a beat of 2.17%.

The proposed $271 million fine, while significant, is measured against the 2025 cash from operations of HKD 40,788 million. The larger risk is not the fine itself but the revenue that disappears with the mandatory mainland wind-down and any reputational spillover into adjacent markets.

On peers, UP Fintech (TIGR), also named in the CSRC action, trades at an NTM P/E of 4.79x versus FUTU’s 9.06x. Futu’s premium reflects its scale advantage: 3.4 million funded accounts, a deeper wealth management platform, and a more diversified geographic footprint. Whether that premium is fully justified post-crackdown is a legitimate question, but the gap is not irrational.

The 19 street analysts tracked by TIKR show a mean target of HKD 1,554.88, with 14 Buys, 3 Outperforms, and 2 Holds. BofA Securities maintained its Buy rating after the regulatory shock, lowering its price target to $223.50 from $235.00.

See how Futu Holdings performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $107.70

- Target Price (Mid): ~$163

- Potential Total Return: ~52%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Futu Holdings stock (It’s free!) >>>

The TIKR mid-case assumes a revenue CAGR of around 12% and a net income margin of around 52%. The two primary revenue drivers are funded account growth across non-mainland markets and rising wealth management fee income. The margin driver is operating leverage as client acquisition costs continue to fall on a per-account basis.

The primary risk is that the CSRC action is not contained. If regulators in other jurisdictions apply similar scrutiny, or if mainland trading activity proves more important to revenue than the 13% account share suggests, the mid-case assumptions break. The free cash flow trajectory in the downside scenario still supports a viable business, but at a lower valuation multiple. The scenario analysis for FUTU is unusually wide, and tomorrow’s earnings report will start narrowing it.

Conclusion

Tomorrow’s Q1 2026 report is the most important data event FUTU has faced in years. The number to watch is not EPS. It is how much of the record Q4 trading volume and net asset inflows were driven by mainland accounts versus the international business. If non-mainland markets held up through Q1, the path from $107.70 toward the mid-case target of around $163 is credible. If mainland exposure proves larger than the 13% account figure implies, the bear case gains ground. The report drops before market open. There will not be much ambiguity left after that.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Futu Holdings?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Futu Holdings, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Futu Holdings alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Futu Holdings on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!