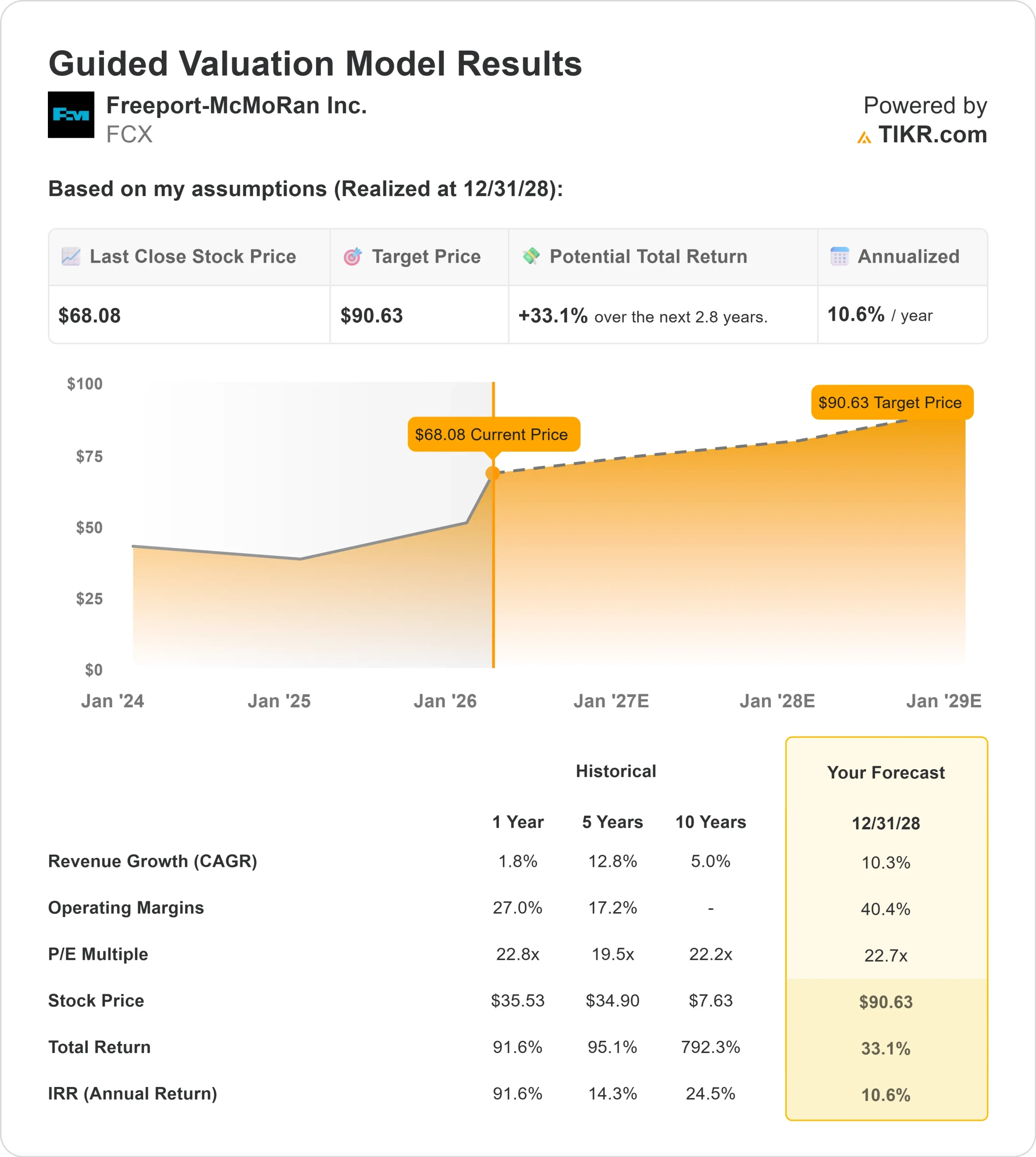

Key Stats for FCX Stock

- This-Week Performance: 6%

- 52-Week Range: $28 to $70

- Valuation Model Target Price: $91

- Implied Upside: 33%

Value your favorite stocks like Freeport-McMoRan with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Freeport McMoRan stock rose about 6% this week, finishing near $68 per share as investors reacted to stronger copper prices, expanded Indonesian mining rights, and renewed institutional positioning. Shares closed near their 52 week high of $70, signaling sustained buying interest rather than a short-term bounce.

The stock moved higher primarily because copper prices strengthened, which directly increases Freeport’s earnings power.

With much of its cost structure fixed, higher realized copper prices expand margins and free cash flow disproportionately, improving near-term profit expectations.

That improvement in commodity fundamentals coincided with management outlining plans to restore 85% of Grasberg production by the second half of 2026 and ramp Production Blocks 2 and 3 in the second quarter, reinforcing confidence in volume recovery this year.

This week, CEO Kathleen Quirk emphasized the newly signed MOU with the Indonesian government to extend Grasberg’s mining rights for the life of the resource, calling it a “very, very exciting milestone” that enables long-term production planning beyond 2041.

Management reiterated that U.S. leach production is expected to rise to about 300 million pounds this year from roughly 240 million pounds last year, part of a plan to increase U.S. output by 60% by 2030 while targeting cost reductions from about $3 per pound toward $2.50.

Institutional activity added further context. Fiera Capital boosted its stake by 99.6% to 295,209 shares worth about $11.58 million, Barings LLC acquired 120,080 shares valued at roughly $4.71 million, Lansforsakringar increased its position by 9.9% to 481,235 shares, NEOS Investment Management raised its stake by 45.7% to 198,510 shares, and Hodges Capital grew its holdings by 8.9% to 499,667 shares, bringing institutional ownership to 80.77%.

At the same time, CAO Stephen Higgins sold 29,654 shares at $63 for about $1.87 million and CAO Ellie Mikes sold 11,000 shares at $62.03 for $682,330, reflecting selective insider selling amid broader institutional accumulation.

See analysts’ growth forecasts and price targets for Freeport-McMoRan (It’s free) >>>

Is FCX Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 10.3%

- Operating Margins: 40.4%

- Exit P/E Multiple: 22.7x

Revenue growth reflects stronger realized copper prices, incremental underground expansion at Grasberg, and steady output from U.S. operations rather than aggressive volume expansion.

The margin outlook assumes copper remains structurally supported by electrification demand, limited new global supply, and disciplined capital spending, which can drive strong incremental free cash flow when prices rise even modestly.

The most meaningful driver in 2026 remains copper pricing relative to Freeport’s cost structure. Because costs are largely fixed, sustained strength in copper can materially expand operating cash flow, strengthen the balance sheet, and enhance capital return flexibility through dividends and buybacks.

Operational execution at Grasberg and continued scaling of U.S. leach production are also central. Delivering on the 300 million pound U.S. leach target this year while progressing toward the longer-term 800 million pound objective by 2030 would meaningfully expand high-margin output at low incremental cost.

Combined with targeted cost reductions toward $2.50 per pound in the U.S., this creates operating leverage even without aggressive volume growth.

Based on these inputs, the model estimates a target price of $91, implying 33% total upside from current levels.

At current prices near $68, Freeport appears undervalued if copper fundamentals remain constructive, with 2026 performance tied primarily to commodity strength, disciplined execution, and cash flow expansion rather than speculative growth assumptions.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does FCX Stock Have From Here?

Investors can estimate Freeport-McMoRan potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See Freeport-McMoRan true value, or any stock’s, in under 60 seconds (Free with TIKR) >>>