Key Stats for Ford Motor Company

- 52-Week Range: $10.68 to $17.78

- Current Price: $13.61

- Street Target Price: $14.95

- TIKR Model Target (Mid Case): ~$21

- Market Cap: ~$54B

- Q1 2026 Revenue: $43.3B (up 6% YoY)

- Q1 2026 Adjusted EBIT: $3.5B (margin of 8.1%)

- Dividend Yield: 4.4%

- Full-Year Adjusted EBIT Guidance: $8.5B to $10.5B

Analyze your favorite stocks like Ford Motor Company with TIKR (It’s free) >>>

Ford Has Been Grinding Sideways All Year. Here’s Why

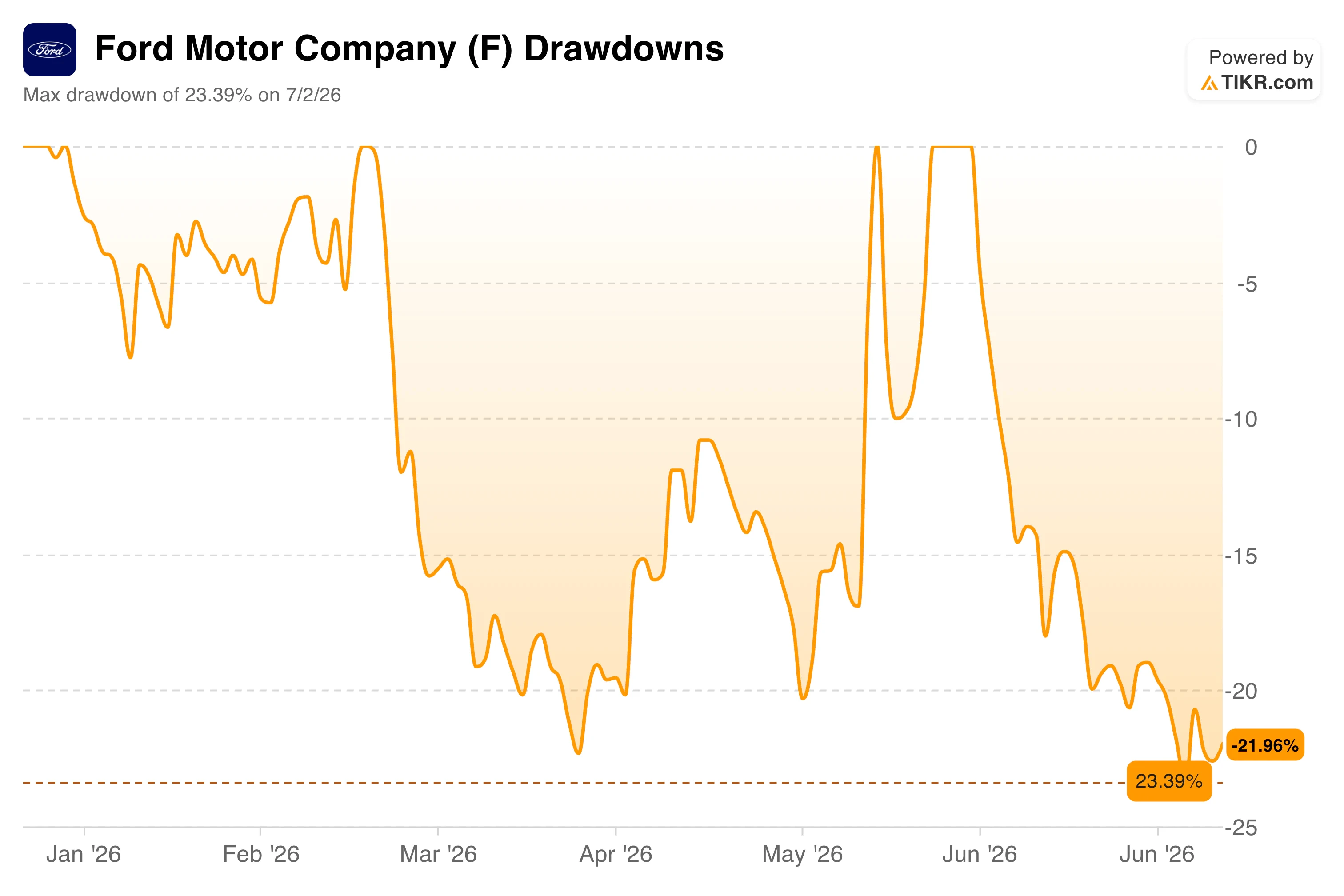

Ford Motor Company (F) has spent 2026 as a stock that keeps almost breaking out and then doesn’t. It started the year near its highs, sold off through March, recovered twice to near-zero drawdown, then sold off again in late June after Q2 sales came in down 10% and a wave of recall headlines hit the tape.

The drawdowns chart captures the frustration precisely. Ford hit a maximum drawdown of 23.39% on July 2, its worst level of the year, then bounced slightly to sit at -21.96% as of early July. The pattern across the full year is telling: the stock recovers, then gives it back, recovering to near flat twice without ever finding the sustained buying interest that would turn it into a trend.

The Q2 sales drop of 10% looked alarming at the headline level, but Ford attributed most of it to planned model phase-outs and a 69% collapse in daily rental fleet sales, a category the company has been intentionally shrinking to protect pricing.

Underlying retail sales were essentially flat. The recall count, now at 51 so far this year, covering hundreds of thousands of vehicles, is the louder overhang.

Ford CEO Jim Farley has publicly acknowledged the quality problem and tied the J.D. Power award to real progress in reducing warranty costs, but the market is waiting to see that show up consistently in the margin line.

See analysts’ growth forecasts and price targets for Ford Motor stock (It’s free) >>>

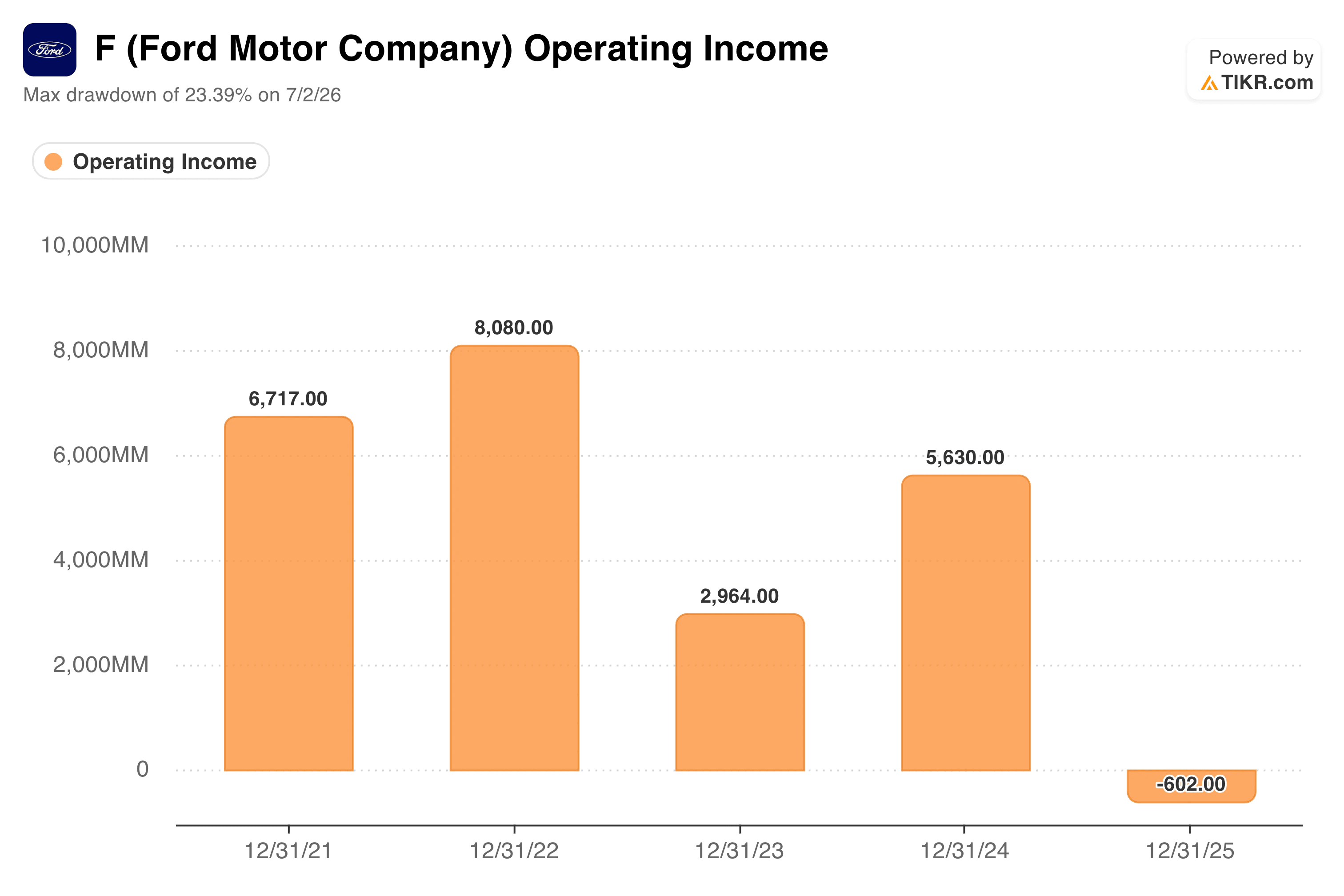

The Operating Income Chart Shows What the Market Is Worried About

Ford’s operating income chart is the source of much of the market’s skepticism, and it warrants a closer look before making any case for the stock.

Operating income peaked at $8.1B in 2022, fell to $3.0B in 2023 as warranty charges and early EV losses mounted, recovered to $5.6B in 2024, then fell to -$602M in 2025. That negative bar is what investors are staring at.

The explanation matters: 2025 included roughly $1.7B in Novelis-related charges connected to a supplier disruption, and Ford Model e, the company’s EV division, lost around $5B for the full year. The core Blue and Pro segments were still profitable, but the losses on the operating line overwhelmed them. Q1 2026 showed the underlying businesses improving in real ways.

Ford Pro generated $1.7B in EBIT on $14.7B in revenue at an 11.4% margin, and software subscriptions from commercial fleet customers grew 30% year over year to 879,000. Ford Blue delivered $1.9B in EBIT on the strength of F-Series, Bronco, and Explorer.

CFO Sherry House said the path to higher margins is clear, and the first quarter showed those building blocks in action. The full-year guidance rose to $8.5B to $10.5B in adjusted EBIT, reflecting genuine confidence in the second half, including a recovery in Novelis’s profit and continued cost reductions.

The complication is that Q1 EBIT included $1.3B in one-time tariff refunds, making the underlying improvement harder to read cleanly until Q2 results arrive on July 28.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What the TIKR Model Says About the Long-Term Setup

The valuation model here is not a high-conviction growth story. It’s a patient value setup built on modest assumptions that reflect what Ford can actually deliver.

The mid-case assumes around 3.5% annual revenue growth and net income margins around 4%, both conservative numbers for a company with $43B quarterly revenue and an improving cost structure.

On those inputs, the model targets around $21 per share, implying a total return of around 54% over four and a half years at roughly 10% annualized.

The low case lands near $22 at about 6% annually; the high case reaches around $32 at around 10%. While waiting on that path, investors collect a 4.4% dividend yield, which is real cash returned while the thesis plays out.

The Street target of around $15 is much more conservative, reflecting analyst caution about EV losses and macro risk. The gap between $15 and $21 is essentially the argument over whether Ford can get Model e losses under control while sustaining the Ford Pro margin improvement.

Should You Invest in Ford Motor Company?

Ford is a genuine value setup at current prices, but patience is a requirement. The EV segment continues to lose around $800M per quarter, commodity costs are rising, and the recall overhang is real.

What makes the stock interesting is that the market is pricing Ford as if the Blue and Pro segments can’t carry the weight, even though they demonstrably already do.

At a 4.4% yield, a single-digit forward P/E, and a mid-case model target of around $21, the stock doesn’t need a dramatic turnaround to work. It needs Ford to keep executing the way it did in Q1, with or without tariff tailwinds.

See analysts’ growth forecasts and price targets for Ford Motor stock (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!