Key Stats for FICO Stock

- Current Price: $1,270.83

- Target Price (Mid): ~$2,440

- Street Target: ~$1,530

- Potential Total Return: ~92%

- Annualized IRR: ~17% / year

- Earnings Reaction: +3.27% (April 28, 2026)

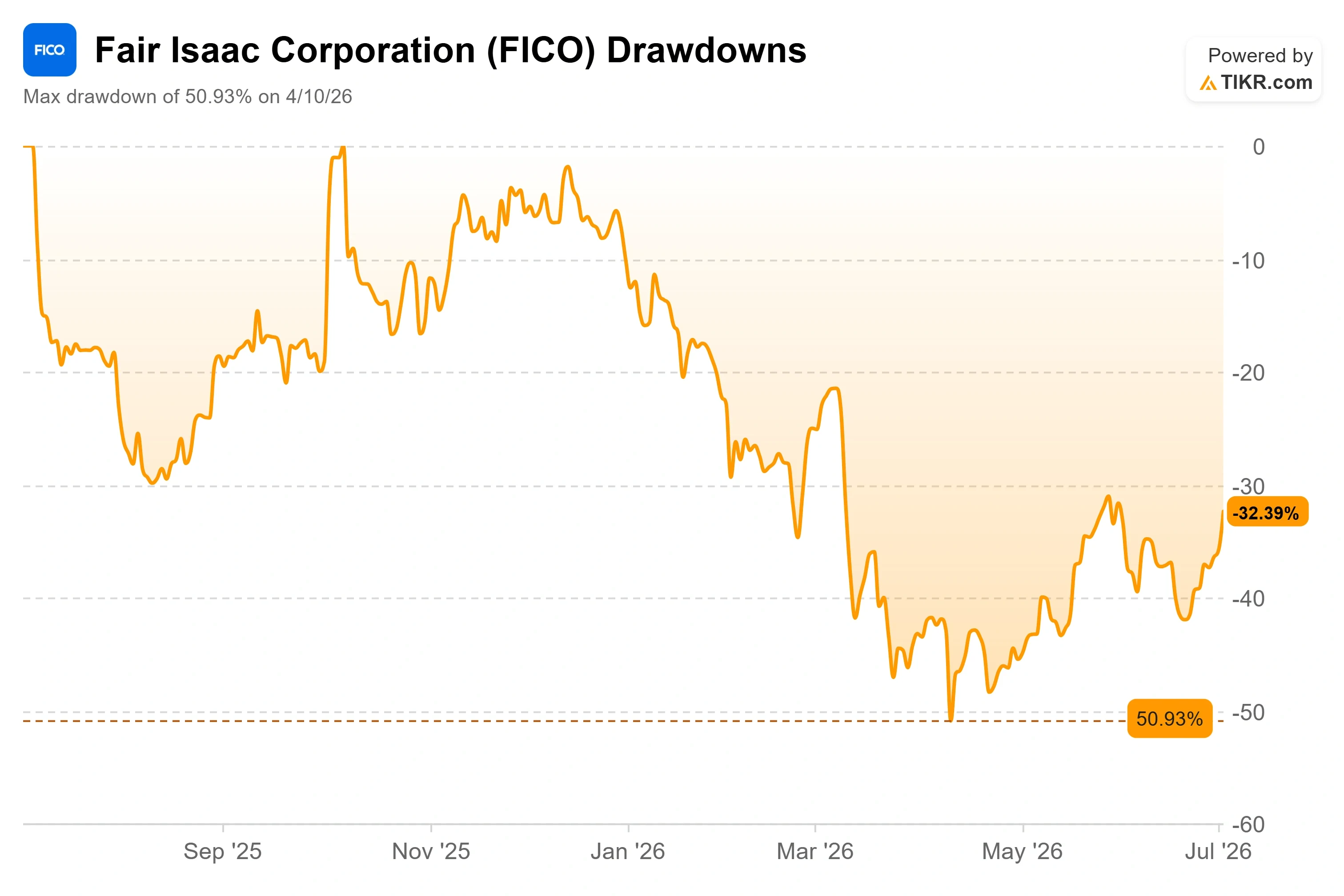

- Max Drawdown: 50.93% (April 10, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Fair Isaac Corporation (FICO) spent most of 2026 as a punching bag, so a 5% pop needs explaining. On July 2, the stock closed up 5.32% at $1,270.83, and the reason was not an earnings beat or an analyst upgrade. It coincided with a quiet data drop the day before.

On July 1, Fannie Mae and Freddie Mac released more than a decade of loan-level performance data for FICO Score 10T, the company’s newest and most predictive credit score, covering mortgages from April 2013 through September 2025. The same release also published additional data for VantageScore 4.0, the rival model FICO competes against. So the milestone advanced both scores at once. For a stock priced as though its mortgage franchise is quietly dying, even a partial validation of 10T matters.

Here is the tension. FICO is still down around 30% year to date and sits 50.93% below its 52-week high, a drawdown that bottomed on April 10, 2026. Bulls argue the business has never been stronger and the selloff is a fear-driven repricing. Bears argue the market is correctly discounting a mortgage moat that regulators are actively prying open. The question neither side can fully answer yet: does releasing the data to validate 10T help FICO more than it helps the rival model sitting right beside it?

Why a Data Release Moved the Stock

To understand the move, you have to understand what has been weighing on FICO. In 2025, the Federal Housing Finance Agency, which oversees Fannie Mae and Freddie Mac, opened the conforming mortgage market to VantageScore 4.0, a rival credit model owned by the three credit bureaus. That ended FICO’s exclusivity on government-backed loans and triggered the worst selloff in the company’s history.

The July 1 release is a step in that same modernization process. The GSEs published historical scores for 10T, the trended-data version of the FICO Score that the company says is meaningfully more predictive than both Classic FICO and VantageScore 4.0. Because the same release also updated VantageScore data, it is a milestone for the broader transition, not a FICO-only win. What helps FICO specifically is that lenders can now test the predictiveness claim against real GSE loan data. FICO Score 10T is currently available at no cost alongside Classic FICO through the FICO Score 10T Free Access Program, and nearly 70 lenders have already signed up.

Julie May, vice president and general manager of B2B Scores at FICO, framed the release as a validation opportunity. She said FICO Score 10T is the most predictive credit score model available and that the company is eager for market participants to dig into the data to independently validate the model’s strength. That matters because FICO’s mortgage argument rests on predictiveness, not price. If independent analysis confirms 10T outperforms, the case for switching to a cheaper model weakens.

See historical and forward estimates for FICO stock (It’s free!) >>>

The Gaming Argument the Market Keeps Missing

At the Barclays Americas Select Conference on May 5, 2026, CEO William Lansing laid out why he thinks VantageScore’s entry is far less threatening than the stock price implies. His argument is the crux of the bull case, and it does not show up cleanly in headlines.

Lansing’s point is that FICO and VantageScore have competed head-to-head for over 20 years in auto and card lending, and VantageScore has won no meaningful paid share. In his telling, the only reason to switch a mortgage is to “game” the government-sponsored enterprises: because a two-score system always leaves one score looking better than the other, lenders could shop for the more favorable score to Fannie and Freddie. He put a ceiling on how much of the market it even affects.

“If you work through all the math on it… it takes you to about a 9% addressable market.” – William Lansing, CEO, Fair Isaac Corporation

Why this matters: Even in Lansing’s own scenario, the exposure is capped at under 10% of the market, and because gaming requires pulling both scores, FICO says it would see no volume loss. That reframes VantageScore from an existential threat into a marginal one, at least by management’s math. FICO also matched VantageScore’s $0.99 upfront price, removing cost as a reason to switch and leaving predictiveness as the deciding factor.

What the Business Is Actually Doing

The disconnect between narrative and numbers is stark. In the second quarter of fiscal 2026, reported on April 28, FICO grew revenue 39% year over year, driven by a 127% surge in mortgage origination revenue and a Scores segment that expanded 60%. The stock’s reaction to that report was a modest +3.27% on the day, a sign the market was more focused on regulatory risk than results. Management raised full-year fiscal 2026 guidance to around $2.45 billion in revenue.

The software side is compounding quietly underneath the mortgage drama. The FICO Platform, the company’s AI-native decisioning product that lets banks and retailers act on customer data in real time, grew 54% year over year last quarter. Lansing described the stickiness of that business directly.

“Our dollar-based net retention revenue on the platform is 136%.” – William Lansing, CEO, Fair Isaac Corporation

Why this matters: a 136% net retention rate, meaning existing customers spend 36% more year over year, even before new logos, is the signature of a land-and-expand software business the market is not paying for. Lansing said the new platform is now a third of total software revenue and growing far faster than the rest.

FICO’s premium valuation is the crux of the debate. The stock trades at an NTM P/E, the price-to-earnings ratio on next-twelve-month estimates, of about 26 times, against a software peer group mean near 14 times that includes Oracle at roughly 17 times and SAP near 19 times. On EV/EBITDA, FICO sits around 19 times versus a peer mean of near 10 times. That premium is steep, but it is attached to a business with an 84.2% gross margin, a 50.9% EBIT margin, and a return on invested capital of 73.8%, efficiency none of those peers come close to matching. The premium holds only if the mortgage franchise holds, which is exactly what the July 1 data helps FICO defend.

The counterweight is real. The Mortgage Bankers Association, while supportive of testing 10T, has warned it expects further FICO price hikes this fall and continues pressing the FHFA for cheaper alternatives to the tri-merge requirement. If pricing power erodes faster than volume recovers, the whole premium unwinds.

See how FICO performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,270.83

- Target Price (Mid): ~$2,440

- Potential Total Return: ~92%

- Annualized IRR: ~17% / year

See analysts’ growth forecasts and price targets for FICO stock (It’s free!) >>>

The two revenue CAGR drivers are mortgage scores pricing, where FICO’s direct licensing program lets it capture value it previously left with the credit bureaus, and FICO Platform expansion at a 136% net retention rate. The margin driver is the Scores segment’s largely fixed cost structure, which pushes net income margins toward the low-40s range as volumes grow. The primary risk is regulatory: faster-than-expected VantageScore adoption or a forced move to a bi-merge system that cuts score volume per application.

The upside case: 10T validation and direct licensing let FICO grow mortgage revenue through both price and share while software compounds, and the multiple re-rates back toward its history.

The downside case: pricing scrutiny and VantageScore adoption compress the Scores premium, and the stock stays range-bound with the multiple reset.

Conclusion

The next real test is FICO’s fiscal fourth-quarter report, expected in late October or early November 2026, and specifically the go-live of the direct licensing program for 10T. Watch two things. First, does 10T direct licensing reach general availability, and do lenders begin adopting it at the pace management implied when it said roughly half the market could prefer the performance model within a year. Second, watch the fall pricing announcement, typically published to partners around September for a January 1 start. “Good” looks like 10T adoption climbing with mortgage revenue growth staying above 20% and no volume erosion. “Bad” looks like VantageScore winning early conforming-market share or the FHFA moving toward a bi-merge mandate. The July 1 data advanced the whole modernization process. Whether lenders read it as a reason to stay with FICO is the question the next two quarters will answer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in FICO?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FICO, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FICO alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!