Key Takeaways for ExxonMobil Stock as of June 2026

- Analysts rate ExxonMobil stock 8 buys, 3 outperforms, 12 holds, 1 underperform, and 1 sell, with a mean target of $170, implying around 25% upside from the current price of $137.

- TIKR’s mid-case model values ExxonMobil at around $148 by December 2030, implying around 9% total return, or roughly 2% annualized.

- ExxonMobil stock looks undervalued at current levels, with Q2 2026 free cash flow expected to surge around 166% year-over-year as the Q1 accounting reversal unwinds into realized cash.

- A $3.9 billion derivatives timing loss compressed Q1 2026 free cash flow to $2.24 billion, but management confirmed the mismatch unwinds in subsequent quarters as physical deliveries complete.

Track ExxonMobil’s full FCF recovery and forward estimates as they update on TIKR for free →

ExxonMobil Stock’s Q1 $3.9B Derivatives Loss Was Accounting Noise, Not Business Damage

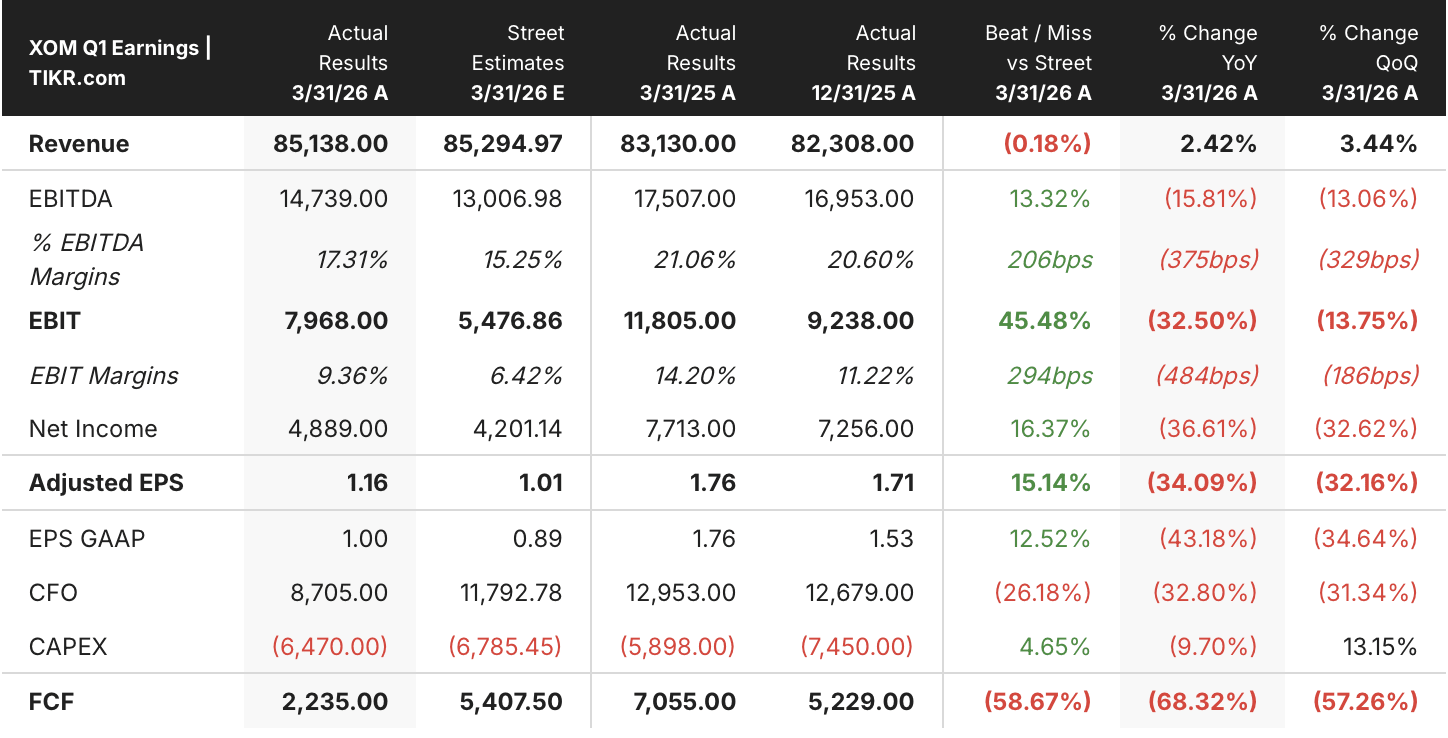

Exxon Mobil Corporation (XOM) reported a $3.9 billion paper loss from derivatives in Q1 2026 that pushed net income to its lowest level in five years, but the company’s underlying operations delivered record production across its two highest-return growth assets.

XOM is one of the world’s largest integrated energy companies, producing and refining oil and natural gas across the upstream (exploration and production), energy products (refining), and chemical products segments.

The derivatives loss stems from an accounting mismatch: ExxonMobil’s trading organization locks in forward prices on physical cargo movements, but the financial hedge marks to market at period-end while the corresponding physical barrel only enters earnings upon delivery.

CEO Darren Woods addressed this directly on the Q1 2026 earnings call: “The timing impact here is primarily driven by the fact that the trading organization is taking advantage of the opportunities in the marketplace and locking in profit.”

Excluding identified items and estimated timing effects, Q1 2026 normalized EPS came in at $1.16, down 34% year-over-year, a figure that reflects real underlying performance rather than the accounting distortion dominating the headline.

Guyana delivered record production above 900,000 bpd in Q1 against installed capacity of around 800,000 bpd, and the Permian Basin remains on track for 1.8 million boe/day in full-year 2026, the two growth engines that generate the forward FCF the thesis depends on.

Bank of America also upgraded ExxonMobil stock to Buy on June 16, projecting approximately $3.3 billion in annualized incremental free cash flow at $70 per barrel Brent once Strait of Hormuz shipping volumes normalize, the first major bank to price in the reversal explicitly.

Wall Street Rates ExxonMobil Stock a Majority Hold Despite 25% Mean Upside

Wall Street rates ExxonMobil stock 8 buys, 3 outperforms, 12 holds, 1 underperform, and 1 sell, across 25 analyst estimates as of June 2026.

The mean price target stands at $170, with a high of $185 and a low of $130, implying around 25% upside from the current price of $137.

Bank of America, which upgraded to Buy in June 2026, cited Strait of Hormuz reopening tailwinds and $3.3 billion in projected annualized FCF uplift at $70 per barrel Brent as the core upgrade rationale.

Wall Street Expects ExxonMobil Stock’s Free Cash Flow to Surge 166% in Q2 2026

Free cash flow collapsed to $2.24 billion in Q1 2026, a 68% year-over-year decline, driven entirely by the $3.9 billion derivatives timing mismatch rather than operational deterioration.

Analysts expect free cash flow to recover to around $14 billion in Q2 2026, a 166% year-over-year increase, as physical deliveries complete and the accounting offset unwinds.

The recovery extends through the second half, with Q3 2026 FCF estimated at around $14 billion (+127% YoY) and Q4 2026 FCF at around $12 billion (+124% YoY).

The key question is whether Strait of Hormuz normalization and crude price softening compress realized margins enough to interrupt the FCF trajectory that underpins the upgrade thesis.

XOM’s FCF Rebound Dwarfs CVX and SHEL Through 2026, Per Consensus Estimates

ExxonMobil’s free cash flow fell 68% year-over-year in Q1 2026, the steepest decline among its three closest peers, with Chevron (CVX) down 45% and Shell (SHEL) down 219% in the same quarter.

Analysts expect XOM’s FCF to surge around 352% year-over-year in Q2 2026, outpacing CVX at around 152% and SHEL at around 34%, the widest recovery spread among the three majors.

The gap widens further into Q1 2027, where XOM’s estimated FCF growth reaches around 1,165% year-over-year against CVX at around 654% and SHEL at around 117%, a trajectory that reflects both the low Q1 2026 base and the compounding of Permian and Guyana volume growth.

TIKR’s $148 Target on XOM Stock Holds If the FCF Reversal Reaches the Balance Sheet

TIKR’s mid-case model values ExxonMobil at around $148 by December 2030, implying around 9% total return from the current price of $137, or roughly 2% annualized over 4.5 years.

That return profile suggests the market prices ExxonMobil stock closer to a mature capital-return vehicle than a growth compounder, consistent with the heavy hold weighting in the analyst consensus.

The case for reaching $148 rests on the FCF recovery already built into Q2 through Q4 2026 estimates: if $14 billion in Q2 free cash flow reaches the balance sheet as management’s timing-unwind thesis predicts, the stock at $137 absorbs that cash without repricing, creating a compressed valuation base that supports the long-term path.

ExxonMobil generated $20 billion in share buybacks in 2025 and targets $20 billion again in 2026, a capital return program that supports per-share earnings growth independent of commodity price direction.

See if ExxonMobil’s $148 target holds at current prices on TIKR for free →

Should You Invest in Exxon Mobil Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Exxon Mobil Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Exxon Mobil Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze XOM stock on TIKR for Free →