Key Stats for Elevance Health Stock

- Past-Week Performance: +0.7%

- 52-Week Range: $273.7 to $458.8

- Current Price: $295.8

What Happened?

Regulators handed Elevance Health (ELV), one of the largest U.S. health insurers and a Blue Cross Blue Shield licensee, a sanctions notice on February 27 that threatens to suspend new Medicare Advantage enrollment starting March 31, compressing shares to $292.16, near their 52-week low of $273.71.

Centers for Medicare & Medicaid Services (CMS) notified Elevance on February 27 that its Medicare Advantage-Prescription Drug plans face enrollment suspension over alleged non-compliance in submitting risk-adjustment data, the financial mechanism by which insurers receive higher payments for sicker members, for dates of service prior to April 3, 2023.

However, Elevance reaffirmed 2026 adjusted EPS guidance of at least $25.5 on March 10, explicitly stating the guidance includes the estimated impact of CMS sanctions if imposed, while Q1 performance is tracking modestly above the January earnings call outlook across Medicare, Medicaid, and ACA.

CFO Mark Kaye stated at the Barclays 28th Annual Global Healthcare Conference also on March 10 that “from where we stand today, we do not expect the financial impact of a resolution to change our capital deployment priorities or actions in 2026,” tying directly to the reaffirmed $5.5 billion operating cash flow floor and $2.3 billion buyback plan.

Elevance’s repositioned Medicare Advantage book, deliberate Medicaid repricing, and expanded Carelon Services platform, which handles specialty pharmacy and behavioral health for both affiliated and external clients, position the company to target at least 12% adjusted EPS growth in 2027 off the 2026 trough baseline.

Wall Street’s Take on ELV Stock

The CMS sanctions overhang that pushed shares to $292.16 obscures a straightforward trough setup: Elevance already absorbed the pain in 2025, repriced across every line of business, and management explicitly designed the $25.50 adjusted EPS floor to include sanctions impact, meaning the market is pricing a risk the guidance already contains.

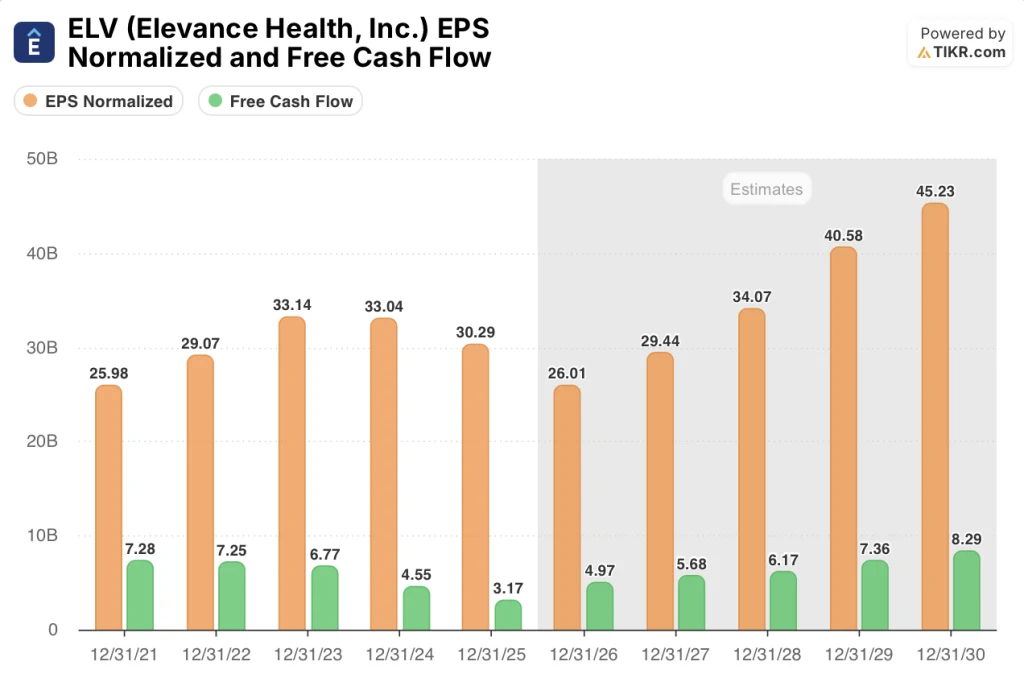

Normalized EPS bottoms at $26.01 in 2026E before rebounding to $29.44 in 2027E, a 13.2% recovery driven by Medicare Advantage margin expanding to at least 2%, Medicaid trend decelerating from double-digit to mid-single-digit, and the $2.3 billion buyback compressing the share count.

Meanwhile, ELV’s free cash flow is forecast to surge 56.7% to $4.97B in 2026E from $3.17B in 2025A, as the timing distortion from delayed Medicaid payments that depressed 2025 cash generation reverses and management targets at least $5.5B in operating cash flow.

Fourteen buys, three outperforms, and eight holds among 20 analysts price ELV at a mean target of $380.95, implying 30.4% upside from $295.75, with the bullish camp anchored specifically to Medicare margin recovery and the 2027 EPS reacceleration thesis management reaffirmed on March 10.

Analyst targets span $332.00 on the low end to $474.00 on the high end; the low reflects a scenario where CMS sanctions extend beyond March 31 and enrollment disruption bleeds into full-year Medicare membership, while the $474.00 high assumes a prompt resolution and clean execution on the Carelon Services external growth pipeline, the company’s specialty health management unit serving clients outside its own insurance plans.

What Does the Valuation Model Say?

The TIKR mid-case prices ELV at $466.87 by December 2030, implying a 57.9% total return and 10.0% IRR, anchored to 2.7% revenue CAGR through 2031E and net income margin recovering from 2.9% in 2026E to 3.0%, both supported by the Medicaid rate catch-up cycle and Carelon’s external momentum.

The market prices ELV as if the CMS sanctions permanently impair the Medicare franchise; the $5.5 billion 2026E operating cash flow floor, reaffirmed after the notice, makes that read untenable.

Director Steven H. Collis purchased 3,000 shares on March 6, days after the sanctions disclosure, and the TIKR model’s $466.87 target reflects the 2027 EPS reacceleration that management has explicitly committed to delivering off the 2026 trough.

CFO Mark Kaye reaffirmed on March 10 that Q1 is tracking modestly above the January outlook across Medicare, Medicaid, and ACA, confirming the trough assumption is holding in real time, not just on paper.

A prolonged CMS sanctions period extending past March 31 breaks the Medicare margin recovery to at least 2% that anchors 2027 EPS growth; delayed resolution directly delays the multiple re-rating.

First-quarter results in April are the first hard confirmation point: watch the Medicare benefit expense ratio and whether Medicaid trend holds in the mid-single-digit range management embedded in guidance.

Should You Invest in Elevance Health, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ELV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elevance Health, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ELV stock on TIKR for Free →