Key Stats for United Therapeutics Stock

- Past-Week Performance: +12%

- 52-Week Range: $267 to $548.1

- Current Price: $540.02

What Happened?

Ralinepag, United Therapeutics‘ once-daily oral pill targeting pulmonary arterial hypertension (a rare, progressive lung disease), just delivered the strongest clinical worsening data ever recorded for any prostacyclin therapy, sending shares up 12% over the past week to $537.60.

On March 2, the ADVANCE OUTCOMES Phase 3 trial unblinded a hazard ratio of 0.45, meaning ralinepag cut the risk of disease worsening by 55% versus placebo, with a p-value below 0.0001, in a patient population where 80% were already on dual background therapy.

Ralinepag drove that result in the toughest possible trial conditions: a contemporarily treated cohort that selexipag, the current standard oral prostacyclin sold as Uptravi, failed to beat in its own dual-therapy studies, making the competitive displacement case essentially self-proving.

Michael Benkowitz, President and COO, stated at the TD Cowen 46th Annual Healthcare Conference on March 2 that “by 2030, we could be upwards of around $2 billion with just ralinepag,” targeting roughly 30,000 U.S. patients currently untreated by any prostacyclin pathway therapy.

United Therapeutics enters 2027 with three pending commercial launches — ralinepag, Tyvaso in IPF (idiopathic pulmonary fibrosis, a separate fatal lung scarring disease), and Tresmi (a soft-mist inhaler that cuts the leading side effect of current inhalers by 90%) — backed by a $2 billion buyback announced March 9 and a Street median price target of $575.

Wall Street’s Take on UTHR Stock

The ralinepag data, the strongest clinical worsening result ever recorded for an oral prostacyclin, shifts United Therapeutics from a single-product inhaler story into a three-launch platform company with distinct addressable markets in 2027.

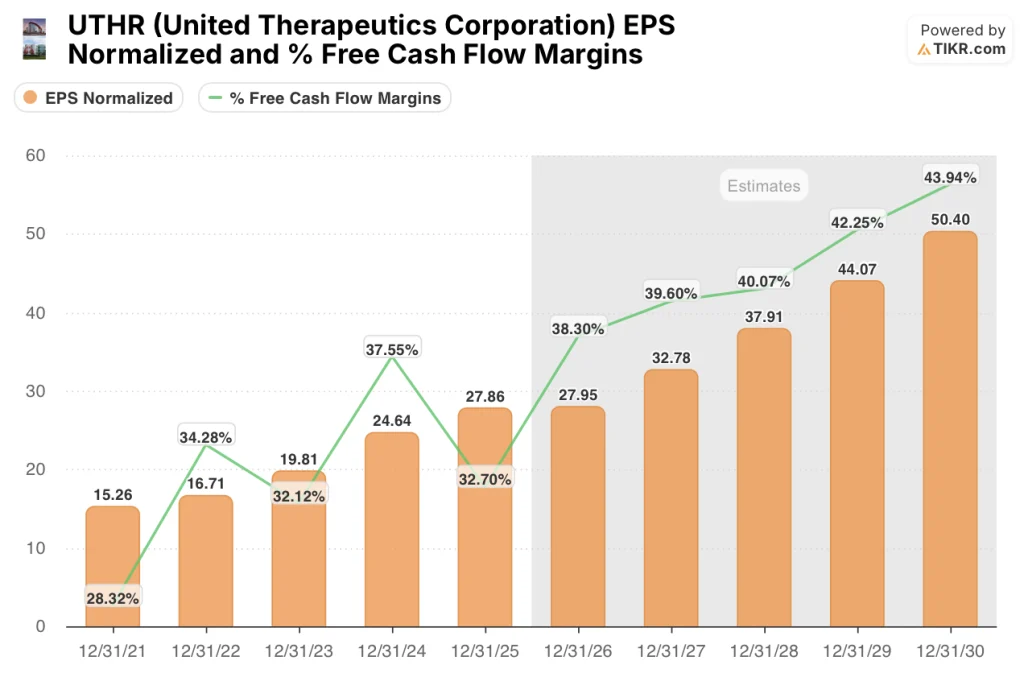

UTHR’s normalized EPS is forecast at $32.78 for 2027, a 17.3% jump from $27.95 in 2026, driven by the ralinepag NDA filing targeted for H2 2026 and the Tyvaso-IPF sNDA filing planned for mid-summer, both of which reach patients in the same launch window.

Free cash flow margins expand from 32.7% in 2025 to a projected 39.6% by 2028, supporting both the $2 billion buyback launched March 9 and the triple launch spending simultaneously.

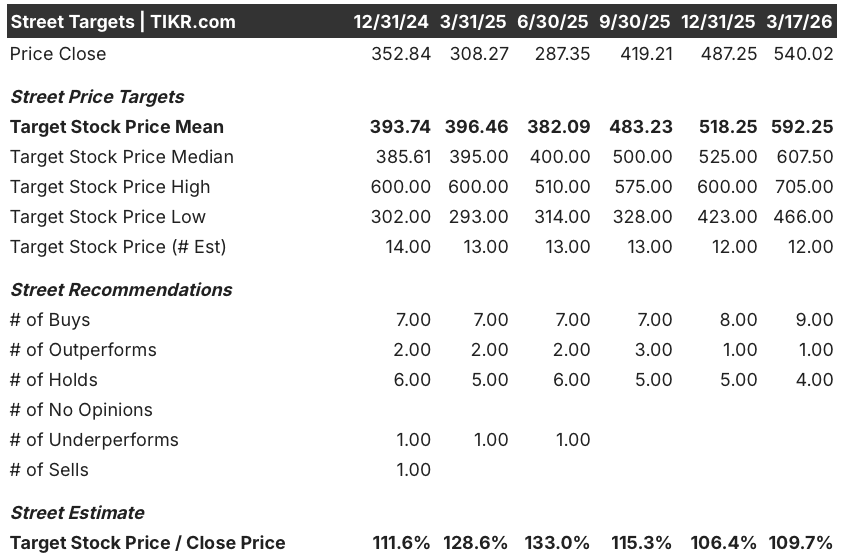

Nine of 14 analysts rate UTHR a buy or outperform, with the Street mean price target at $592.25 as of March 17, implying 9.7% upside from $540.02, a consensus anchored to the ralinepag data and the pending TETON-1 IPF readout expected imminently.

The analyst target range spans $466.00 on the low end to $705.00 on the high, with the low reflecting execution risk on three simultaneous 2027 launches and the high implying the Street begins pricing ralinepag’s $2 billion 2030 revenue potential into the multiple before approval.

What Does the Valuation Model Say?

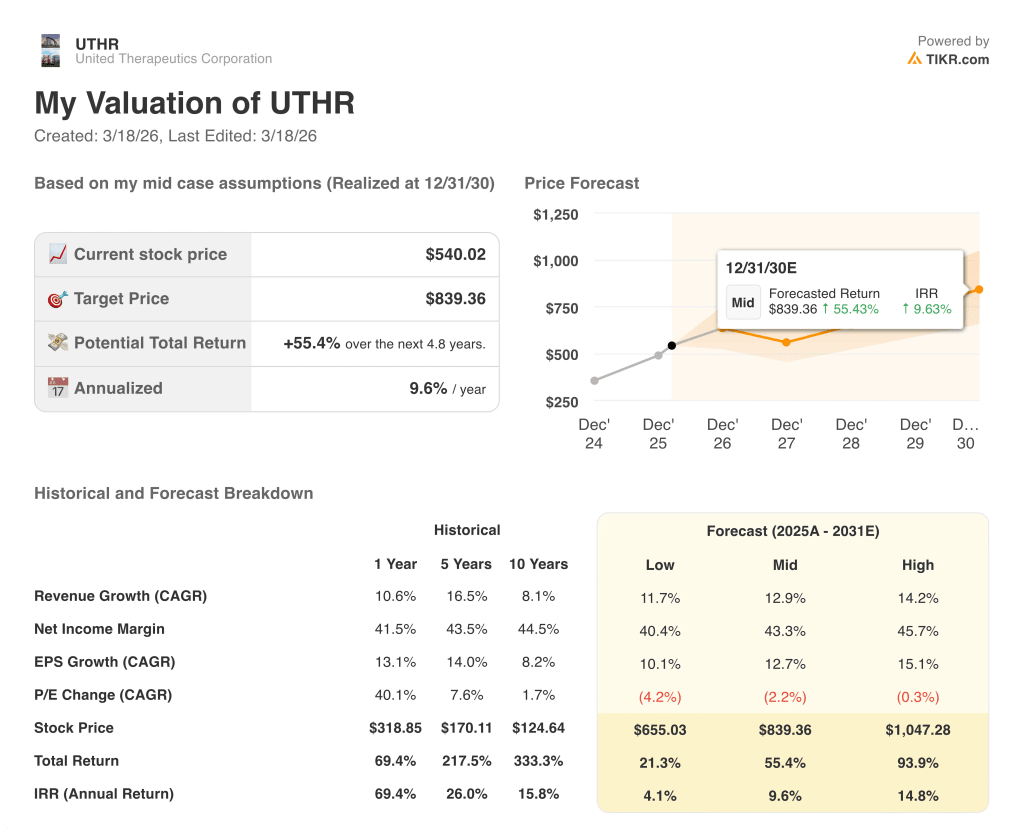

The TIKR mid-case model prices UTHR at $839.36 by December 2030, implying a 55.4% total return on 12.9% revenue CAGR and stable 43.3% net income margins, assumptions grounded in the confirmed double-digit commercial trajectory and three named product launches already in filing range.

The market is pricing UTHR at 19.4x 2027E normalized EPS of $27.95, which assigns zero option value to ralinepag’s $2 billion 2030 target and a 100,000-patient IPF market that Tyvaso has not yet entered.

Ralinepag’s hazard ratio of 0.45 in an 80%-dual-therapy population, a standard no prior oral prostacyclin has met, is the specific operational proof that justifies the TIKR model’s 12.9% revenue CAGR assumption through 2030.

Management’s commitment to a $4 billion annualized revenue run rate by H2 2027, stated explicitly on the February 25 earnings call before ralinepag data existed, signals the growth floor is the existing business, not the pipeline.

TETON-1 IPF data, expected imminently, is the single near-term risk: a failure would remove the $100,000-patient IPF opportunity from the 2027 launch slate and directly impair the TIKR model’s 2027 revenue step-up from $3.34 billion to $3.78 billion.

The TETON-1 top-line readout is the number to watch; a result consistent with TETON-2’s 95.6 mL FVC improvement over placebo confirms the sNDA filing timeline and locks in the mid-summer submission that anchors the 2027 commercial calendar.

Should You Invest in United Therapeutics Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UTHC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track United Therapeutics Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UTHC stock on TIKR for Free →