Key Stats for AbbVie Stock

- Past-Week Performance: -4.5%

- 52-Week Range: $164.4 to $244.8

- Current Price: $219.8

What Happened?

Pharmaceutical giant, AbbVie Inc (ABBV), whose immunology drugs Skyrizi and Rinvoq now generate more combined revenue than peak Humira ever did, has structurally solved its biosimilar problem at $219.76 per share with a $67 billion revenue guide for 2026.

On March 2, AbbVie reported positive Phase 3 AFFIRM data for Skyrizi’s subcutaneous induction in Crohn’s disease (a self-injectable dosing format that removes the need for intravenous infusions), with clinical remission of 55% versus 30% for placebo at week 12.

Skyrizi and Rinvoq delivered combined 2025 revenues of approximately $25.9 billion, up more than $8 billion year-over-year, already surpassing AbbVie’s own 2027 combined guidance by $500 million and capturing roughly 75% of new frontline IBD patient starts.

Chief Commercial Officer Jeffrey Stewart stated on the Q4 2025 earnings call that “Skyrizi and Rinvoq are a great pair in IBD…together, our two brands have already exceeded peak Humira sales by more than $4.5 billion and are on pace to deliver more than 20% growth in 2026,” anchoring investor confidence heading into the subcutaneous label expansion.

AbbVie’s $21.5 billion Skyrizi guide, $10.1 billion Rinvoq guide, and a confirmed Parkinson’s franchise targeting more than $5 billion in peak sales position the company for high single-digit revenue growth through 2029, with $18.5 billion in free cash flow expected this year alone.

Wall Street’s Take on ABBV Stock

The AFFIRM data confirming Skyrizi’s subcutaneous Crohn’s induction works directly extends the drug’s frontline dominance into a more patient-friendly format, removing the IV administration barrier that still limits biologic penetration in IBD.

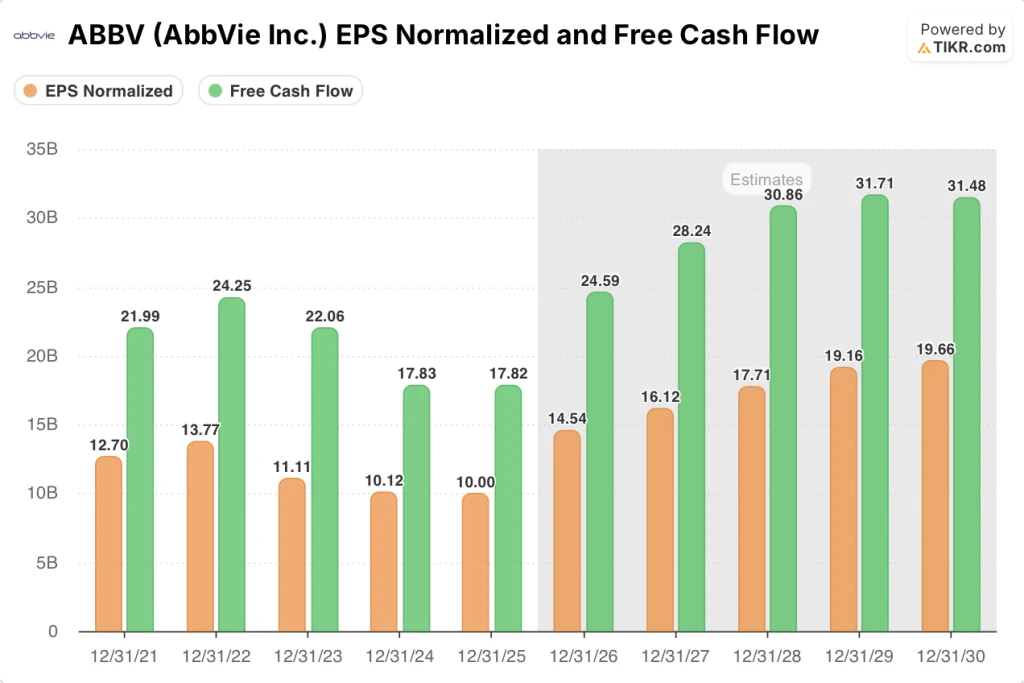

AbbVie’s normalized EPS collapsed from $13.77 in 2022 to $10 in 2025 as Humira biosimilars eroded revenue, but the TIKR model projects a 45.4% single-year snap to $14.54 in 2026, powered by Skyrizi’s $21.5 billion and Rinvoq’s $10.1 billion forward revenue guides respectively.

Supporting that EPS reset, free cash flow (the cash a business generates after capital expenditures, the clearest measure of financial health) is also projected to jump 38% from $17.82 billion in 2025 to $24.59 billion in 2026, with FCF margins expanding from 29.1% to 36.7% in a single year.

Twenty-one analysts rate ABBV a buy or outperform against eight holds and just one underperform, with a mean price target of $248.86 implying 13.2% upside from $219.76, as consensus prices in the Skyrizi and Rinvoq revenue ramp but not yet the full margin expansion.

The spread between the $184 bear target and the $299 bull target reflects a binary view on IBD competition: the low anchors to TREMFYA share erosion accelerating, while the high prices in Skyrizi’s subcutaneous label and lutikizumab’s hidradenitis suppurativa Phase 3 data landing in 2026.

What Does the Valuation Model Say?

The TIKR mid-case target of $339.60 implies 54.5% total return through December 2030 at a 9.5% IRR, driven by a 5.5% revenue CAGR and net income margins expanding to 41.6% as the high-cost Humira defense spend rolls off and Skyrizi royalty obligations absorb into a larger revenue base.

The market prices ABBV near its 52-week low relative to its mean target, yet EBITDA margins are set to expand from 40% in 2025 to 49.8% in 2026, a 980-basis-point single-year jump that consensus has not fully re-rated.

Skyrizi’s 75% frontline IBD in-play capture rate, holding firm despite TREMFYA’s entry, confirms the margin expansion is not volume-at-risk; it is volume-at-premium pricing with a durable competitive moat.

The primary risk to the TIKR model’s 5.5% revenue CAGR is accelerating IBD share loss to icotrokinra (an oral IL-23 inhibitor in late-stage development), which could compress Skyrizi’s frontline capture rate and delay the margin normalization the model prices in through 2030.

Watch the etentamig (a BCMA-targeting T cell engager for multiple myeloma) Phase 3 objective response rate readout in H2 2026; a strong result validates AbbVie’s oncology pipeline, the segment the TIKR bull case needs to carry growth after Vraylar’s 2030 patent expiry.

Should You Invest in AbbVie Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ABBV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AbbVie Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ABBV stock on TIKR for Free →