Key Stats for Vertex Pharmaceuticals Stock

- Past-Week Performance: +2.8%

- 52-Week Range: $262.5 to $515.7

- Current Price: $462.5

What Happened?

Vertex Pharmaceuticals (VRTX), a drugmaker best known for dominating the cystic fibrosis market, posted its most consequential pipeline result in years when povetacicept, its experimental kidney disease drug, cut urine protein by 52% in a Phase III trial on March 9, clearing the way for a U.S. approval filing by end of March.

Maxim Group upgraded Vertex to buy from hold on March 18 and set a $575 price target for the first time, citing the 52% protein reduction result from the RAINIER trial in IgA nephropathy, a progressive autoimmune kidney disease that can lead to kidney failure within 20 years of diagnosis.

Povetacicept also reduced a harmful antibody linked to IgAN by 77% and cleared blood in the urine for 85% of patients versus placebo, results BMO Capital Markets analyst Evan Seigerman called positioning the drug as a “clear competitor and potential leader” in the indication, comparing favorably to Otsuka’s approved Voyxact.

Moreover, Chief Commercial Officer Duncan McKechnie stated on the Q4 2025 earnings call that “povetacicept’s potential best-in-class profile enables us to clearly distinguish it within the IgA nephropathy landscape, setting it apart from other therapies,” as the company reported full year 2025 revenue of $12 billion and guided for $12.95 billion to $13.1 billion in 2026.

A U.S. approval decision as early as late 2026 would add a fourth commercial franchise to a company already generating $12.3 billion in cash, buying back $2 billion in stock annually, and targeting $500 million or more in non-CF revenue in 2026 from CASGEVY and JOURNAVX alone.

Wall Street’s Take on VRTX Stock

The March 9 povetacicept Phase III result does more than validate a pipeline asset — it reframes the entire FCF trajectory, because a fourth commercial franchise arriving ahead of schedule accelerates the gross-to-net normalization already underway in JOURNAVX and the infusion ramp in CASGEVY, compressing the timeline to a materially higher cash generation base.

Vertex’s FCF surges 56.3% from $3.19 billion in 2025 to an estimated $4.99 billion in 2026, with FCF margin expanding from 26.6% to 38.3%, driven by JOURNAVX patient support program costs unwinding and CASGEVY infusion volumes accelerating off a 300-patient initiation base built in 2025.

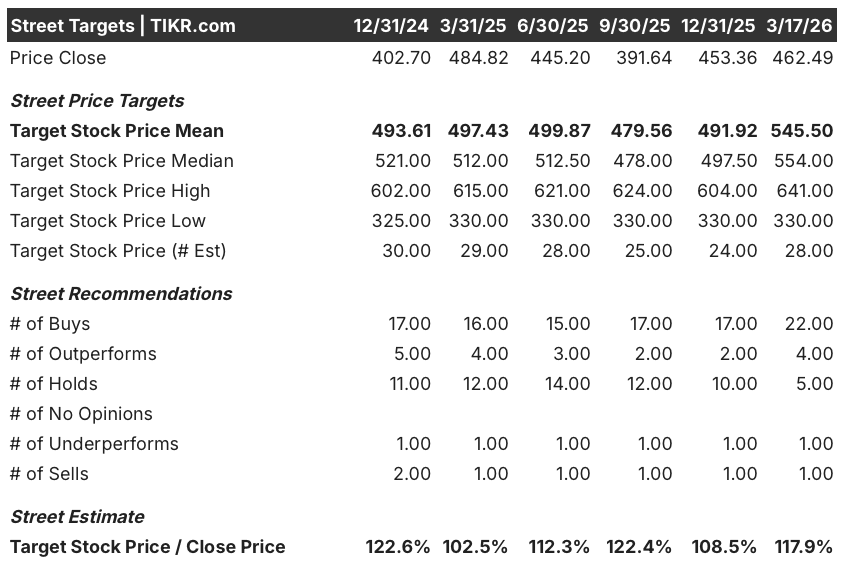

Sentiment shifted sharply after March 9, with 22 analysts now rating the stock a buy, 4 an outperform, and just 5 a hold against 2 negatives, producing a mean price target of $545.50 and a median of $554.00, both implying roughly 17.9% upside from the current $462.49, as analysts specifically price in accelerated approval of povetacicept in H2 2026 and a tripling of JOURNAVX prescriptions year-over-year.

The $330.00 analyst floor reflects a scenario where povetacicept stumbles in the full 605-patient RAINIER trial or JOURNAVX prescription growth stalls before gross-to-net normalizes, while the $641.00 ceiling prices in clean full approval for the kidney drug and a JOURNAVX revenue inflection in H2 2026 as the patient support program sunsets.

What Does the Valuation Model Say?

The TIKR mid-case target of $823.72, implying 78.1% total return at a 12.8% annualized IRR to December 2030, assumes a 10.3% revenue CAGR and FCF margin expansion to 38.8%, both grounded in a fourth franchise generating renal revenue, JOURNAVX reaching scale, and CASGEVY smoothing its infusion variability by 2027.

The market is pricing Vertex at 24x forward earnings, near its five-year average, despite FCF nearly doubling in a single year to $4.99 billion as three commercial launches simultaneously scale.

The TIKR model’s $823.72 target rests on renal becoming a fourth revenue vertical, a thesis the March 9 RAINIER data directly supports by clearing the path for a U.S. approval filing this month.

Management confirmed the signal on the Q4 call: 74 payer engagements covering 210 million lives already completed for povetacicept, before a single regulatory approval, indicating commercial infrastructure is ahead of the clinical timeline.

Meanwhile, the risk is hypogammaglobulinemia, the immune suppression that comes with blocking BAFF and APRIL, triggering serious infections in the full RAINIER trial that force a label restriction or a black box warning, collapsing the blockbuster thesis.

Watch the complete RAINIER BLA submission confirmation by end of March and the FDA acceptance letter two months after, which sets the six-month priority review clock and effectively locks in the late 2026 approval timeline the model assumes.

Should You Invest in Vertex Pharmaceuticals Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VRTX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vertex Pharmaceuticals Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VRTX stock on TIKR for Free →