Key Stats for DoorDash Stock

- Current Price: $183.09

- Target Price (Mid): ~$960

- Street Target: ~$245

- Potential Total Return: ~423%

- Annualized IRR: ~44% / year

- Earnings Reaction: +2.01% (May 6, 2026)

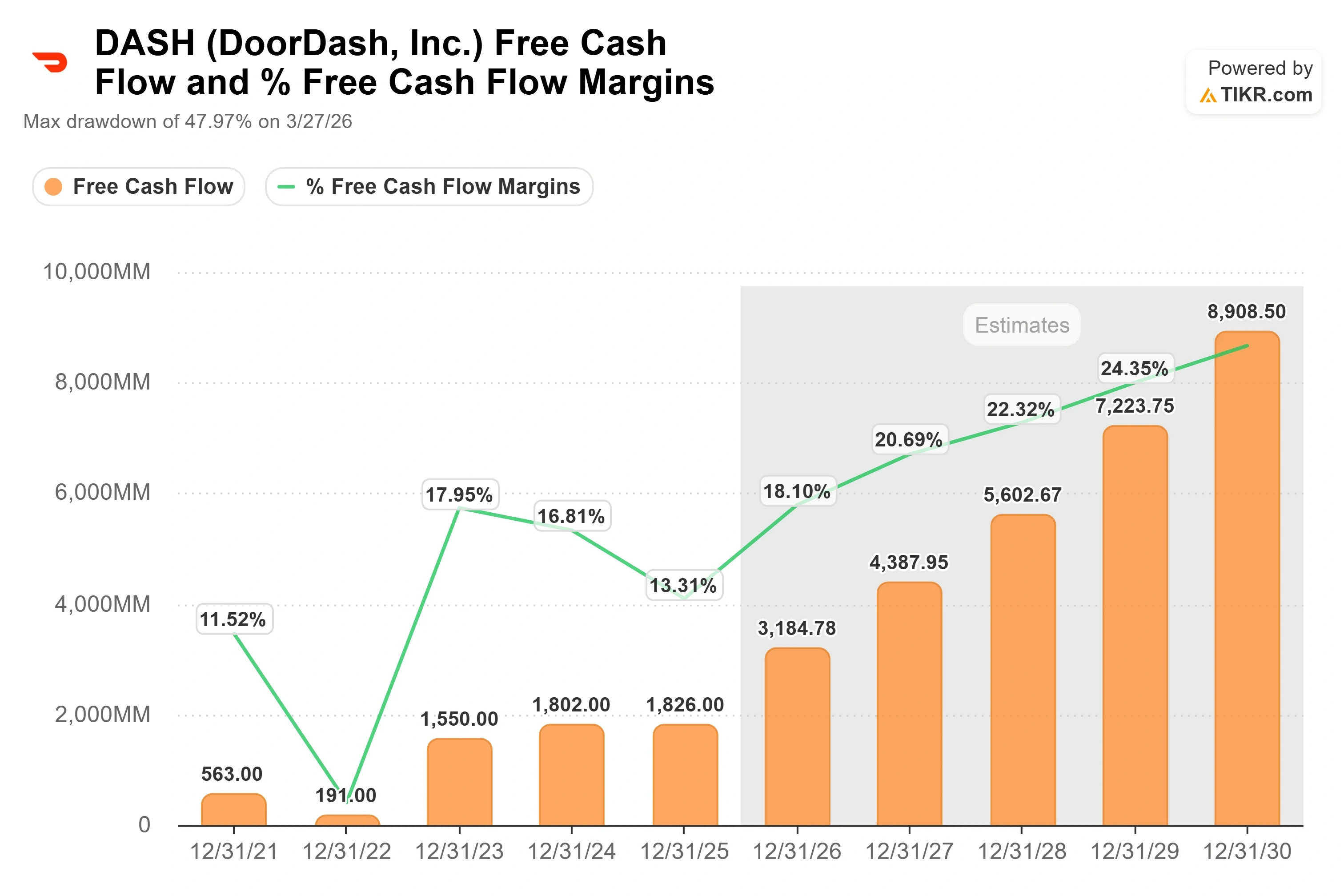

- Max Drawdown: 47.97% (March 27, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

DoorDash (DASH) closed at $183.09 on June 26, up 3.49% on the day, and yet the stock is still down around 21% in 2026 and sits roughly 36% below its 52-week high of $285.50. That gap is the whole argument. Bulls think the company is laying the foundation for years of compounding. Bears think management is torching margins on a spending binge with no promised payoff. Neither side has won yet.

Most of the recent debate has fixated on the obvious stuff: the macro bounce, the Dollar Tree rollout, the new AI ordering assistant. The piece that fewer investors are pricing carefully is the one that could quietly reset the cost structure. DoorDash is building its own autonomous delivery platform, and it owns it outright. The market mostly treats that as a science project. Management treats it as one of the core levers for the next decade.

The question this article works through is simple. If the autonomy bet works alongside the rest of the roadmap, what is DoorDash actually worth?

What Management Actually Said About Robots

On the Q1 2026 earnings call (May 6), CFO Ravi Inukonda framed the strategy plainly. He said DoorDash is building an autonomous delivery platform because different formats suit different deliveries, and that mix is how you build the most efficient network. That word, efficient, is the tell. Every per-order dollar that comes out of delivery cost can flow toward the bottom line.

CEO Tony Xu went further, and his framing is the most useful thing on the call. He drew a line between shipping a vehicle for a demo and running one at scale under any condition. His analogy: he can shoot a three-pointer, and so can Steph Curry, but one of them is the greatest shooter of all time, and the other hits it once in a while. The point lands. Plenty of companies can show a delivery robot. Very few can operate a hardened fleet across messy real-world cities. DoorDash is spending 2026 climbing that curve with its “Dot” ground robot, drone partnerships, and the remote operations and regulatory work underneath.

Autonomy is not the only story, and Xu was careful about that. He spent more of the call on the end-to-end shopping experience, grocery, and advertising than on robots. But autonomy is the lever that bears most often dismiss, and it reframes the spending they hate. The 2026 investment is not just a tech replatforming bill. Part of it is building a delivery network that can get structurally cheaper to run over time.

See historical and forward estimates for DoorDash stock (It’s free!) >>>

The Numbers Behind the Story

DoorDash is not a speculative cash-burner, which is what makes the autonomy bet fundable. The company posted Q1 2026 revenue of $4,036 million, up around 33% year over year, and actual EBITDA of $754 million against a consensus near $742 million, a clean beat. Trailing twelve-month free cash flow sits at $2,296 million. This is a business throwing off real cash while it invests.

The balance sheet backs the ambition. DoorDash carries net cash, not debt, with LTM net debt of negative $2,246 million. That means the autonomy and platform spending are funded from the company’s own resources, not borrowed money. A delivery peer carrying heavy leverage could not run this playbook. DoorDash can.

The growth engine has two clear drivers. First, U.S. share gains in restaurant delivery plus the expansion into grocery and retail, where DoorDash became the volume leader, and where Xu argues the category should eventually be larger than restaurants once the experience improves. Second, the international portfolio, where Deliveroo is expected to contribute around $200 million of EBITDA in 2026, and where Xu said the brand is seeing its highest growth rate in four years.

Where the Premium Is, and Whether It’s Earned

DoorDash trades richer than its delivery peers on revenue, and the comparison cuts both ways depending on the multiple you pick. On NTM enterprise value to revenue, DASH at 4.2x towers over India’s Eternal Limited at 2.4x and Germany’s Delivery Hero at 0.8x. On NTM EV/EBITDA, the order flips: DASH at around 20x sits below Eternal’s 66x and above Delivery Hero’s 13x.

The premium to Delivery Hero is defensible. DoorDash grows faster, generates positive free cash flow, and holds net cash instead of the debt that weighs on parts of the European sector. Investors are paying up for the highest-quality operator in delivery, and the autonomy platform is the asset that could widen that quality gap further. The risk is that the premium leaves little room for error if execution slips.

The single biggest risk is duration. If the tech replatforming stretches deep into 2027, or if autonomous delivery needs more capital than current estimates assume, the free cash flow inflection bulls are counting on gets pushed out. Inukonda said the redundant cost of running three tech stacks in parallel will mostly run through 2026, with some bleeding into early 2027. Watch that timeline. It is the difference between the bull case and a value trap.

See how DoorDash performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $183.09

- Target Price (Mid): ~$960

- Potential Total Return: ~423%

- Annualized IRR: ~44% / year

See analysts’ growth forecasts and price targets for DoorDash stock (It’s free!) >>>

This analysis uses the TIKR model’s mid case, which assumes DoorDash executes the operational roadmap it has already laid out rather than anything heroic. The mid case points to a target near $960, a total return around 423%, and an IRR around 44% a year over roughly the next 4.5 years.

Two revenue drivers anchor it: U.S. share gains across restaurant, grocery, and retail delivery, and the international portfolio led by a reaccelerating Deliveroo. The margin driver is operating leverage, as the autonomy platform lowers per-order delivery cost and one global tech stack replaces three, removing redundant spend. The primary risk is duration: a prolonged investment cycle that delays the margin inflection.

The upside: if grocery scales toward restaurant size and autonomy compresses delivery cost, DoorDash compounds at a rate the current price does not reflect.

The downside: if spending extends again without offsets, the margin story slips, and the premium multiple has little support.

Conclusion

The catalyst to watch is Q2 2026 earnings, due in early August. The specific number that matters is second-half EBITDA. Inukonda told investors second-half EBITDA dollars and margins should land above the first half, even after roughly $50 million in quarterly gas-rewards costs, and the full-year EBITDA guide held steady.

Here is the threshold. If second-half EBITDA clearly outpaces the first half and management reaffirms the autonomy and tech timeline, the investment cycle is working, and this year’s discount looks like an entry point. If margins slip and the spending extends again without offsets, the bears are right, and the premium deserves to compress. The August print settles which story is true.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in DoorDash?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DoorDash, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DoorDash alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DoorDash on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!