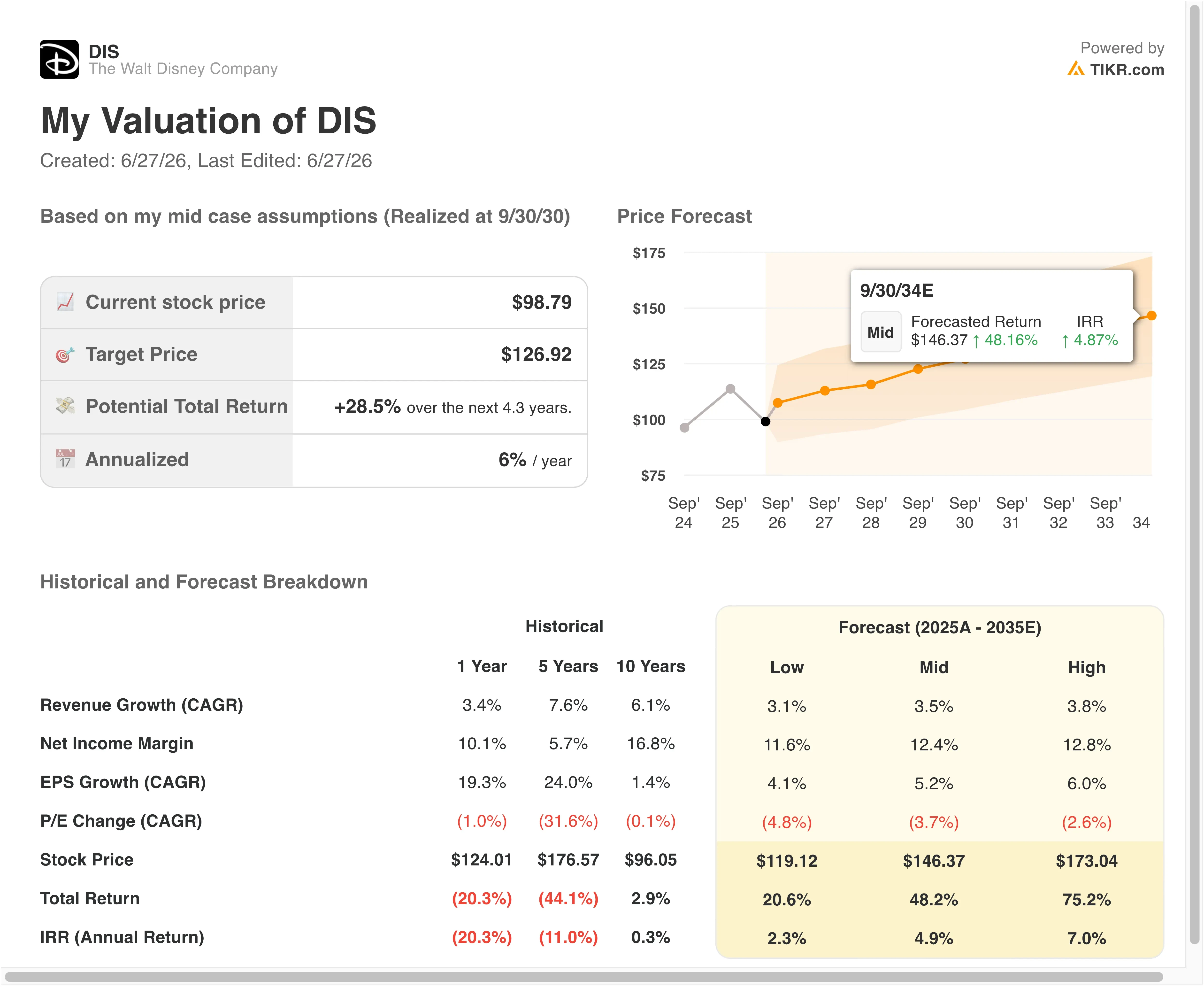

Key Stats for DIS Stock

- Past week’s performance: -2.4%

- 52-week range: $92 to $125

- Valuation model target price: $116

- Implied upside: +17.9% over 2.3 years

Run your own DIS valuation with 5 years of analyst forecasts using TIKR (It’s free) >>>

A New CEO, a Q2 Beat, and a Regulatory Storm Around ABC

The Walt Disney Company (DIS) reported second-quarter fiscal 2026 earnings on May 6 and beat Wall Street expectations. Disney posted adjusted EPS of $1.57, topping the $1.49 estimate. Revenue rose 7% to $25.2 billion. Yet the stock fell from its early-year highs and has not recovered, because two parallel storylines are pulling investor attention in opposite directions.

The positive storyline is real. Disney targeted $8 billion in share repurchases, and new CEO Josh D’Amaro outlined a growth strategy including streaming expansion, parks investment, and a possible super-app combining theme park ticketing, movie purchases, and content into one platform. D’Amaro, the former Disney Experiences chairman who took the CEO role in February 2026, is pushing toward more aggressive capital deployment after years of caution under Bob Iger.

The regulatory storyline is also real. The FCC began reviewing Disney’s ABC station licenses after a dispute that started with a Jimmy Kimmel joke and escalated into a formal proceeding. The FCC chair said all options remain on the table. ABC filed early license renewals and launched an on-air campaign asking viewers to support the network. That public fight with a federal agency has introduced a license-risk overhang that is difficult to price.

Content momentum is building despite the regulatory noise. Toy Story 5 drove the busiest domestic box office weekend of 2026, and the new Star Wars film opened to $165 million worldwide. D’Amaro confirmed plans to keep ESPN in-house rather than spin it off and secured a new WWE content deal for ESPN. Going forward, the third-quarter earnings report on August 5 will test whether content momentum translates into a durable streaming lift.

See analysts’ growth forecasts and price targets for DIS (It’s free) >>>

Is DIS Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 5.3%

- Operating Margins: 19.4%

- Exit P/E Multiple: 13.3x

Based on these inputs, the model estimates a target price of $116, implying a 17.9% total return from the current share price of $99 and an annualized return of 7.5% over the next 2.3 years.

A 7.5% annualized return is honest about where Disney sits right now. The stock is not obviously cheap, but it is also not expensive for the quality of the asset. The $8 billion buyback program adds a capital-return component that the model does not fully capture. Applied against a market cap of roughly $172 billion, it represents about 4.6% of shares outstanding if executed at current prices.

The revenue CAGR of 5.3% is reasonable and reflects the breadth of Disney’s business. Parks, streaming, theatrical, and sports rights all contribute, and each has a different growth driver. The forward two-year revenue CAGR implied by the street sits at 6.0%, close to the model’s assumption, which suggests consensus is not banking on a dramatic acceleration either.

The operating margin assumption of 19.4% is where the story gets interesting. Disney’s LTM EBIT margin is 14.7%, so the model asks for roughly 4.7 points of margin improvement over two years. That is achievable if streaming losses narrow and content spending stays disciplined. D’Amaro has made efficiency a stated priority, and his experience background means he knows where cost levers exist.

DIS vs. Netflix and Comcast

Netflix (NFLX) is the most useful streaming comparison. Netflix trades at roughly 33x to 35x forward earnings, a premium that reflects its near-monopoly on global streaming profitability. Disney’s streaming business includes Disney+, Hulu, and ESPN+, which together are approaching profitability but have not yet matched Netflix’s margin consistency. The valuation gap essentially asks when, not whether, Disney’s platform reaches Netflix-level economics.

Comcast (CMCSA) is the more direct conglomerate comparison. The company owns NBC broadcast assets, Universal theatrical, and Peacock streaming, mirroring Disney’s mix. Comcast trades at roughly 10x to 11x forward earnings, a discount to Disney’s 13.3x. Yet Comcast generates stronger free cash flow from its cable infrastructure business, which Disney does not have, and that structural difference explains much of the gap.

Disney’s moat is its IP. No other media company commands the same franchise depth across Marvel, Star Wars, Pixar, and core Disney animation. That IP drives theme park pricing power and streaming retention in ways Netflix and Comcast cannot replicate.

The bear case is regulatory: if ABC’s license is threatened and streaming margins take longer to recover, the multiple could compress further. The bull case, implied by the $129 street target, is that D’Amaro’s operational push plus the buyback plus a working content pipeline pushes the stock back toward prior highs.

Read our full take on Disney’s turnaround, earnings, and valuation >>>

What’s Driving DIS Stock Going Forward?

The Q3 2026 earnings report on August 5 is the most important near-term catalyst. Analysts will focus on streaming subscriber growth, particularly whether the Hulu profile-linking feature and new music festival livestreams are driving engagement. Parks’ performance will also matter, since Disneyland Paris expansion and Shanghai’s continued growth are incremental revenue sources the market has not fully priced.

The ABC/FCC situation is an overhang that will not resolve quickly. The FCC chair’s statement that all options remain on the table creates legal uncertainty around the broadcast business. Democratic senators called the review an abuse of power, and ABC has pursued legal challenges. The regulatory process is slow by design, so this fight will cost management time and attention.

ESPN’s future is the most consequential long-term decision on Disney’s table. Keeping ESPN in-house means Disney must keep funding rights payments for NFL, NBA, and WWE content while building the direct-to-consumer streaming service. The upcoming ESPN launch in 53 international countries is a meaningful step toward monetizing sports rights beyond cable. Management must execute this expansion without overpaying for rights renewals that could squeeze the margins the model depends on.

Content momentum is building in ways that matter for the stock. Toy Story 5 drove record domestic attendance, Star Wars opened strongly worldwide, and Marvel’s Doomsday with Robert Downey Jr. and Chris Evans is generating heavy pre-release attention. If theatrical performance keeps beating expectations and streaming profitability turns the corner in fiscal 2027, the combination of buybacks and margin expansion could push DIS toward the model’s $116 target and beyond.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in The Walt Disney?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DIS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DIS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze DIS stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!