Key Stats for Palo Alto Networks Stock

- Current Price: $332.00

- Target Price (Mid): ~$460

- Street Target: ~$315

- Potential Total Return: ~39% (over ~4.1 years)

- Annualized IRR: ~8% / year

- Earnings Reaction: -5.64% (June 2, 2026)

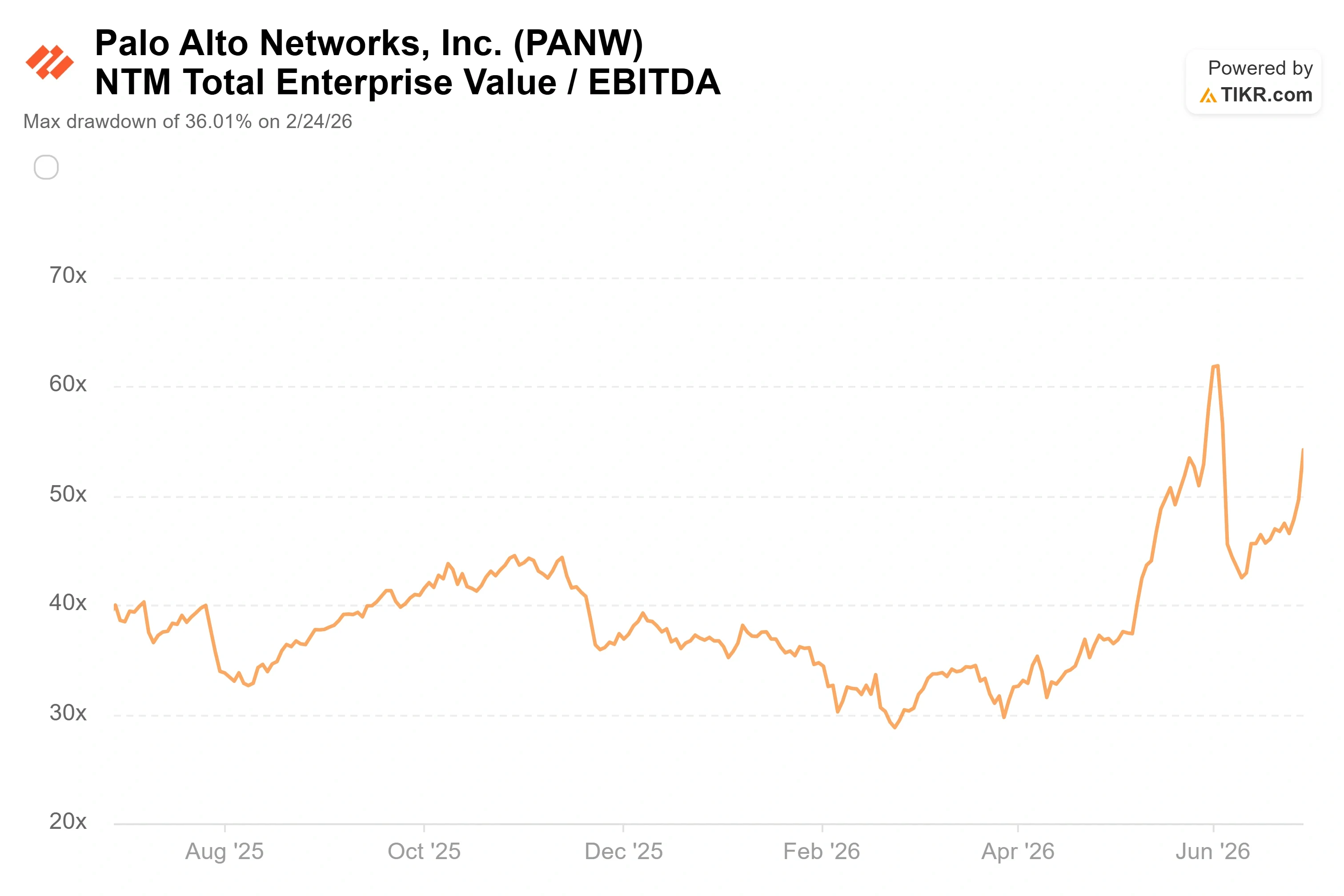

- Max Drawdown: -36.01% (February 24, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Palo Alto Networks (PANW) closed June 29 at an all-time high of $332.00, up 9.14% on the day, the kind of move that usually follows a blowout earnings report. There was no earnings report. The stock jumped on a sector-wide rotation into cybersecurity, and the rally arrived the same week that a lawsuit drew fresh attention to a question hanging over the whole industry: how reliable is AI-generated threat research?

That backdrop sharpens the debate. The market is paying a record price for an AI security leader at a moment when the accuracy of AI security tools is being argued in court. Bulls see a platform compounding through the most important demand cycle in the company’s history. Skeptics see a stock at around 85x next-twelve-months earnings, still posting GAAP losses, with insiders selling into the rally. The question neither side can fully answer yet: how much of the AI premium is already in the price?

A record close with no earnings behind it

The catalyst on June 29 was not PANW-specific. A widely circulated forecast from a major investment bank projected a sharp expansion in global security spending and named cybersecurity the largest growth driver, prompting institutional investors to rotate back into the sector’s platform leaders. Peer CrowdStrike rose the same day. PANW absorbed an outsized share of that flow and printed a fresh 52-week high of $332.88 intraday.

The move caps a stunning round trip. PANW bottomed at a 36.01% drawdown on February 24, 2026, when the market doubted both the CyberArk integration and the organic growth trajectory. From that low, the stock has more than doubled.

The recovery rests on real numbers. In fiscal Q3 2026, reported June 2, revenue grew 31% year-over-year to $3.0 billion, and adjusted EPS of $0.85 beat the high end of guidance by $0.05. Next-generation security ARR, meaning the annualized value of the company’s recurring subscription products, reached $8.13 billion, up 60%. Management raised full-year guidance across every metric. Yet the stock fell 5.64% the day those results dropped, then climbed steadily for four weeks to a record. That gap between the earnings-day reaction and the rally since is itself a signal: the recent buying has been about the AI narrative, not the print.

See historical and forward estimates for Palo Alto Networks stock (It’s free!) >>>

What management actually said about the AI threat

The bull case has a specific author. On the Q3 call, CEO Nikesh Arora argued that frontier AI has compressed attack timelines from months to minutes and that this raises, rather than lowers, the value of cybersecurity platforms. “Mark my words, Mythos has increased the terminal value of the entire cybersecurity industry,” he told analysts, referring to the emergence of cyber-capable frontier models. He added that six months earlier, investors feared AI would make security vendors obsolete, and instead, “you actually just created a longer-term G in your model for long-term growth rate for cybersecurity.”

That reframes the debate. If Arora is right, the demand driving PANW’s ARR is not a cyclical software-spending wave that can roll over, but a structural escalation that intensifies as AI capability advances. CFO Dipak Golechha reinforced the financial side, saying the company is running three to six months ahead of schedule on converging CyberArk’s profitability with its own, which keeps it on track for a 40% adjusted free cash flow margin in fiscal 2028.

The proof points are concrete. Next-generation firewall bookings rose nearly 40% year-over-year, the strongest hardware quarter in a decade, driven by AI data center build-outs and a new buyer class of sovereign infrastructure providers and frontier labs. Prisma AIRS, the company’s AI security product, tripled its customer count in a single quarter to over 300. As a result, the demand story is broad, not concentrated in one line.

The risk the bull case has to carry

There is a tension inside the AI story, and a current lawsuit illustrates it. According to reporting from Axios, videoconferencing startup MeetingTV is suing Palo Alto Networks and Koi Security, the threat-intelligence firm PANW acquired in April, over a research report that linked MeetingTV’s infrastructure to a Chinese hacking operation. MeetingTV alleges the finding stemmed from an AI error and says its domains remain blocked across security products, even after Koi removed one domain and stated there was no evidence it connected to the threat actor. Axios notes that no court filing has provided direct evidence that AI systems generated the disputed finding, and Palo Alto Networks has said it expects the dispute to be resolved through the legal process. The allegations are unproven.

The financial exposure here is small relative to a $270 billion company, and the case predates the acquisition, having been filed against Koi before PANW was later named. The reason it is worth a mention is thematic, not legal. On the same call where Arora pitched the AI defense story, he warned that frontier models carry false-positive rates often reaching 25%, and that “one wrong enforcement decision can take down a global production network.” Whatever the merits of this specific suit, it is a reminder that AI-driven threat research carries reliability risk, which is the exact challenge management says its platform exists to solve.

Where the valuation sits versus peers

PANW trades at extreme multiples, and that is the heart of the skeptics’ case. The stock carries an NTM EV/EBITDA, meaning enterprise value over next-twelve-months earnings before interest, taxes, depreciation, and amortization, of 54.21x, against a software peer-group median near 13x. Among direct comparables, CrowdStrike trades richer still at roughly 98x NTM EV/EBITDA, reflecting its faster growth, while Fortinet sits far cheaper at about 38x. PANW occupies the middle, priced like a high-growth platform rather than a maturing firewall vendor.

Is that premium justified? The bull answer is that PANW is growing 31% with a 38.5% trailing free cash flow margin and a path to 40% by fiscal 2028, a combination few software companies at this scale can match. The bear answer is that the forward earnings multiple of around 85x leaves almost no room for execution stumbles, that the company still reports a GAAP net loss, and that insiders sold tens of millions of dollars of stock over the prior three months into this exact rally. Both can be true. The valuation prices in years of flawless platformization raise the stakes for every quarter ahead.

See how Palo Alto Networks performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $332.00

- Target Price (Mid): ~$460

- Potential Total Return: ~39% (over ~4.1 years)

- Annualized IRR: ~8% / year

- Revenue growth assumed: ~14% per year

See analysts’ growth forecasts and price targets for Palo Alto Networks stock (It’s free!) >>>

The two revenue drivers behind that target are platformization, as customers consolidate network, cloud, identity, and observability spending onto a single platform and lift revenue per account, and AI-security attach, as Prisma AIRS, XSIAM, and the CyberArk identity suite expand the products sold into the existing customer base. The margin driver is operating leverage from the recurring-revenue mix.

The primary risk is multiple compressions. The model already assumes the forward P/E falls from today’s premium toward historical norms, so even strong execution produces a return that is solid rather than spectacular, and any slip in platformization velocity or margin timing pulls it lower.

- Upside (high case): if AI-driven demand lifts growth and margins, total return rises toward around 180%.

- Downside (low case): with growth near 13% and slower margin expansion, total return is around 51% over the period, still positive but well below the rally’s recent pace.

Conclusion

The single number to watch is fiscal Q4 NGS ARR, reported in August, guided to $8.9 billion. Hitting or beating that confirms the platformization engine is still accelerating and supports the premium. A miss, or any wobble in the organic growth rate that the company will soon stop breaking out separately, would hand the skeptics their first real evidence that 85x earnings was too much. Good looks like ARR at or above guidance with the FY28 margin target reaffirmed. Bad looks like decelerating organic growth masked by acquisition contribution. Watch the August print. The record high bought PANW a high bar, and August is when it has to clear it.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Palo Alto Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Palo Alto Networks, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Palo Alto Networks alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Palo Alto Networks on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!