Key Takeaways for Constellation Energy Stock as of June 2026

- Analysts rate Constellation Energy stock 14 buys, 6 outperforms, 3 holds, and 1 sell with a mean target of $360, implying around 39% upside from the current price of $259.

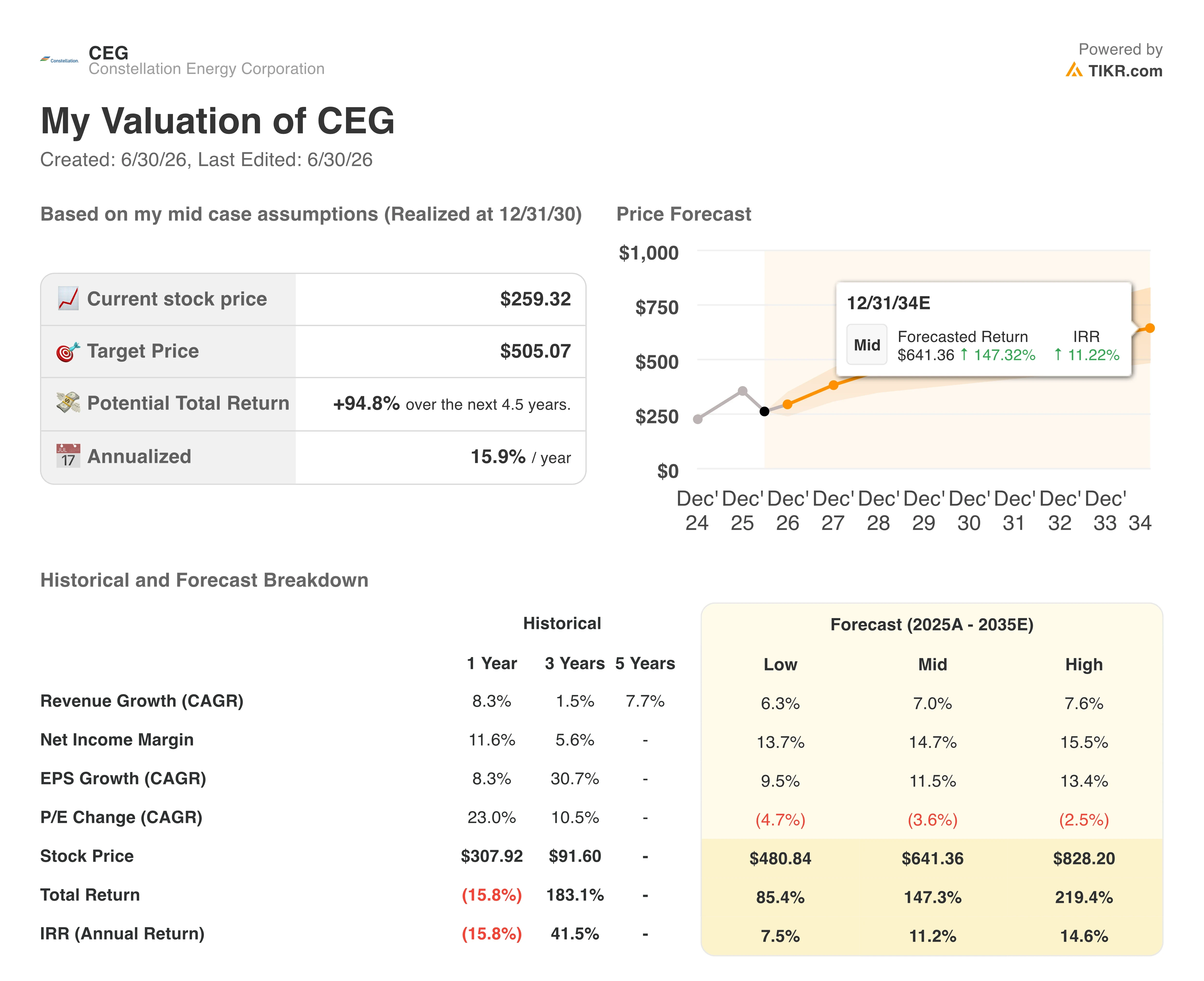

- TIKR’s mid-case model values Constellation Energy at $505 by December 2030, implying around 95% total return, or roughly 16% annualized.

- Constellation Energy stock is undervalued at current levels, with normalized EPS forward growth of 26% implied for fiscal 2027 not yet reflected in the share price.

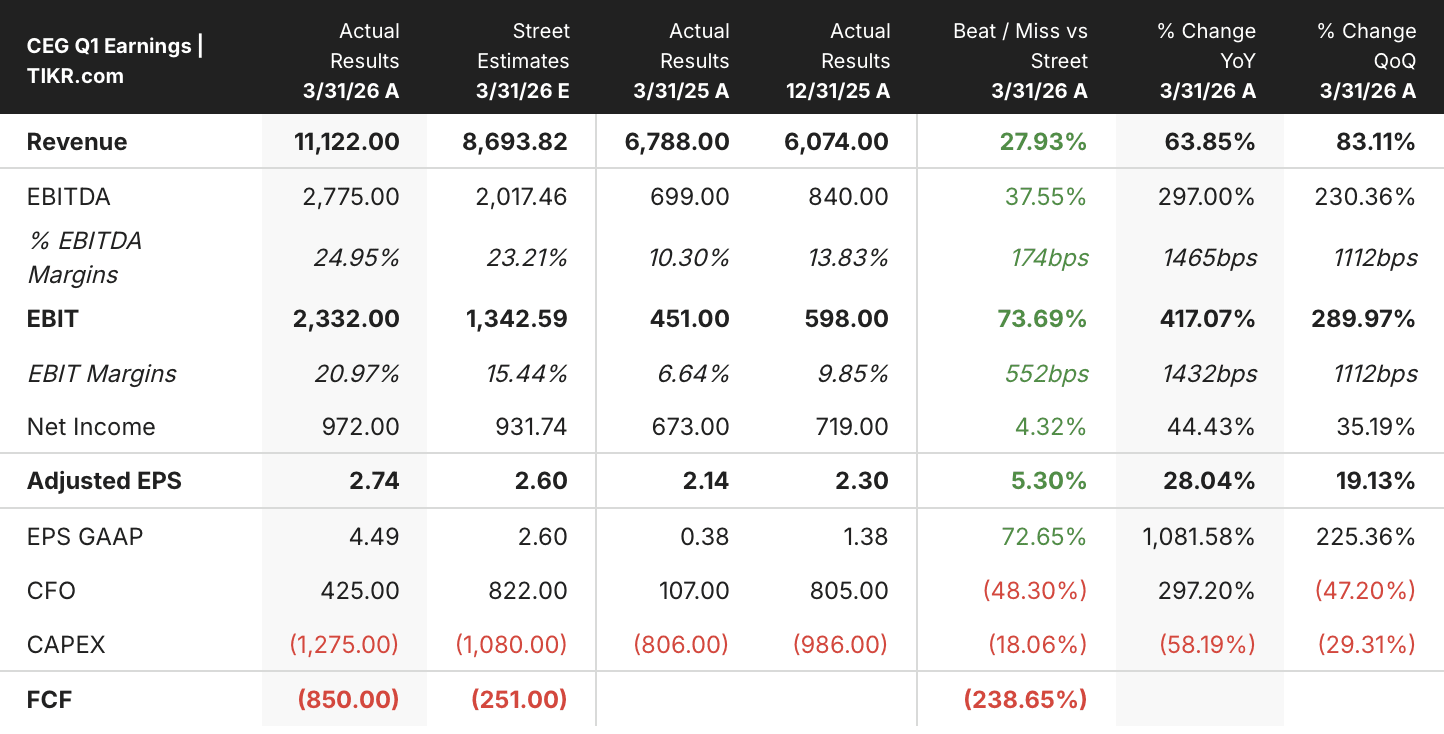

- Constellation posted Q1 adjusted EPS of $2.74, beating the $2.57 consensus, while reaffirming full-year guidance of $11 to $12 per share.

Constellation Energy Stock Beats EPS but the Real Story Is the Earnings Power Ahead

Constellation Energy stock (CEG) has fallen roughly 19% year to date even as the company just posted one of its strongest quarters on record. The largest U.S. nuclear power operator reported first-quarter adjusted operating earnings of $2.74 per share, beating the $2.57 consensus estimate, while GAAP earnings reached $4.49 per share on a one-time tax benefit.

That GAAP number masks the more durable story underneath. Total operating revenue climbed 64% year over year to $11.12 billion, driven largely by the completed acquisition of Calpine’s gas-fired generation fleet in January.

CFO Shane Smith addressed the earnings mix directly on the Q1 call, framing the quarter’s strength around the integration: “Higher earnings for the quarter can mostly be attributed to the EPS accretion from Calpine.” That accretion, he noted, was already baked into guidance at roughly $2 per share for the full year.

Beneath the segment numbers, nuclear output slipped slightly to 44,666 gigawatt-hours from 45,582 a year earlier, due to planned refueling outages rather than operational weakness. Even so, the company affirmed its full-year adjusted operating earnings guidance of $11 to $12 per share, a range that implies continued acceleration from the Calpine contribution.

The bigger story, though, is regulatory. CEO Joe Dominguez told investors that Constellation hopes for a federal decision as early as June on restarting the Three Mile Island plant, now renamed Crane Clean Energy Center, under contract to serve Microsoft data centers. Management is also pressing PJM for faster clarity on a capacity framework tied to surging data center demand.

What that means for investors is a company executing on two fronts at once: integrating a transformative acquisition while positioning for a wave of nuclear and gas demand from hyperscale customers that has not slowed.

Wall Street Stays Bullish on Constellation Energy Stock Despite the YTD Slide

Analysts remain firmly bullish on Constellation Energy stock, with 14 buy ratings, 6 outperforms, 3 holds, and 1 sell as of June 2026. The mean price target sits at $360, implying around 39% upside from the current price of $259.

That target has held remarkably steady through the year’s volatility, moving from $312 in June 2025 to $397 in March 2026 before settling near current levels, even as the stock itself swung from $323 to $279 to $259 over the same stretch.

The conviction held even through a $3.1 billion secondary share offering in early June that pressured the stock further.

Wall Street Expects Constellation Energy Stock’s Normalized EPS to Grow 26% Through Fiscal 2027

Constellation Energy posted normalized EPS of $2.74 for the quarter ended March 2026, up 28% from a year earlier. The Street expects that momentum to continue, with normalized EPS forecast to reach $3.71 for the quarter ending June 2026, a 26% increase year over year.

Looking further out, consensus estimates show normalized EPS of $2.69 for the quarter ending March 2027, even as full-year guidance for 2026 stays anchored at $11 to $12 per share. The trajectory steps forward into a clear tension: estimates show meaningful deceleration in the March 2027 quarter before reaccelerating to 18% growth by June 2027.

The unresolved question now is whether Constellation’s earnings power proves as durable through 2027 as the current quarter suggests, or whether the deceleration already visible in the estimates table becomes the dominant trend.

TIKR’s $505 Target on Constellation Energy Stock Holds if Capacity Clarity Arrives on Schedule

TIKR’s mid-case model values Constellation Energy at around $505 by December 2030, implying around 95% total return from the current price of $259, or roughly 16% annualized over 4.5 years.

That annualized rate would place Constellation Energy stock well ahead of typical utility-sector return profiles, which rarely clear double digits on a forward basis.

The target is reachable if PJM delivers the capacity framework clarity management expects by year-end and the Crane restart proceeds on its 2027 capacity-credit timeline, both catalysts already in motion following the company’s regulatory filings and FERC engagement.

Should You Invest in Constellation Energy Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Constellation Energy Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Constellation Energy Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CEG stock on TIKR for Free →