Key Stats for OXY Stock

- Past week’s performance: -3.9%

- 52-week range: $39 to $67

- Valuation model target price: $54

- Implied upside: +8.5% over 2.5 years

Build your own OXY valuation in under 60 seconds with TIKR’s free Guided Valuation Model >>>

A Blowout Quarter, a New Captain, and an Oil Market in Flux

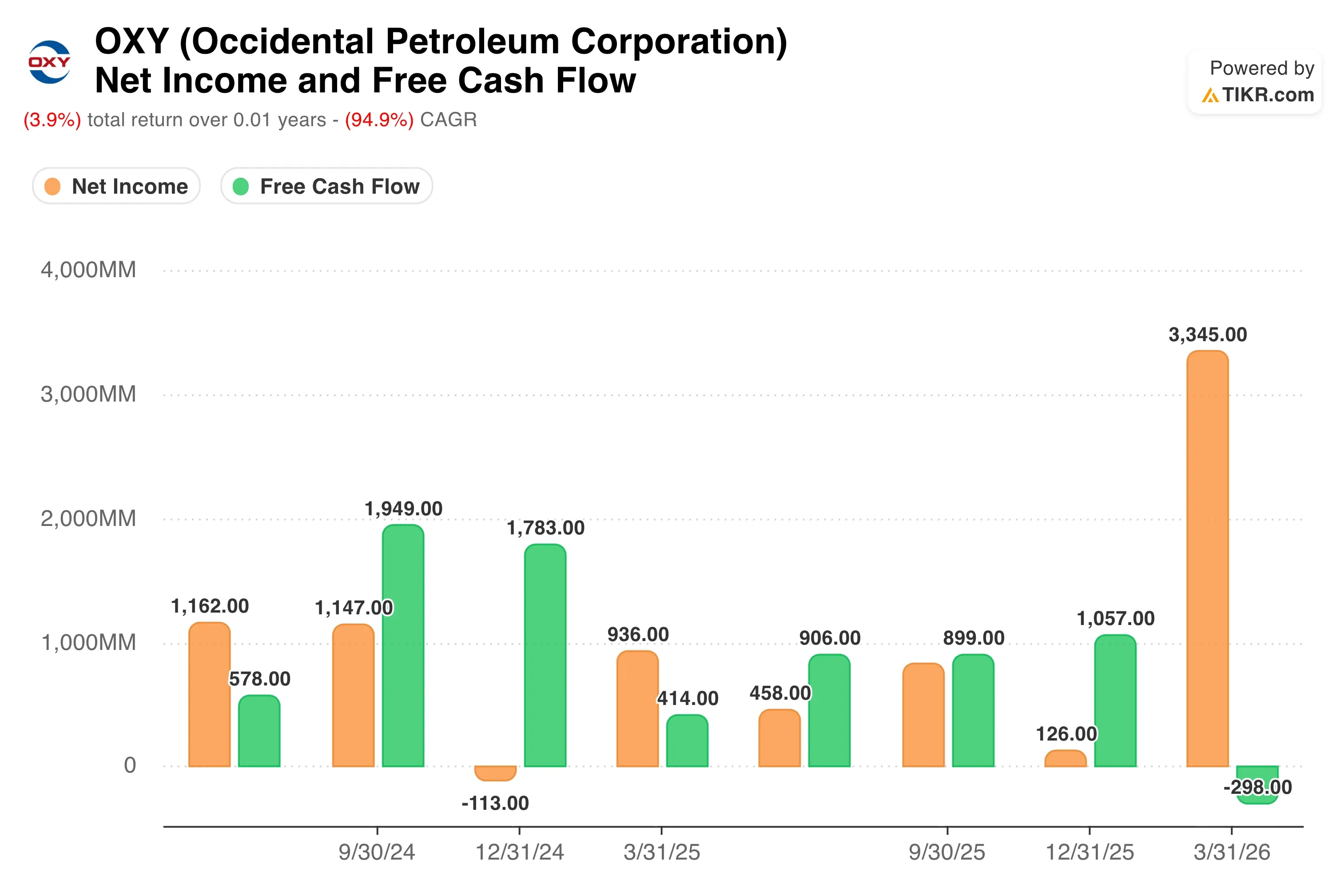

Occidental Petroleum (OXY) beat Wall Street’s first-quarter expectations by a wide margin. The company posted adjusted EPS of $1.06, topping the $0.59 consensus by nearly 80%. Net income reached $3.2 billion, and free cash flow before working capital came in at around $1.7 billion.

The Iran conflict drove oil prices sharply in both directions this year. Energy stocks surged when geopolitical risk escalated, then sold off when ceasefire signals emerged. OXY moved with the broader energy group through each swing. Strong fundamentals are fighting a crude market that swings on every diplomatic headline, and that tension is the real story for investors right now.

Production averaged 1.43 million BOE, or barrels of oil equivalent, per day in the first quarter. Occidental exceeded the high end of its guidance in both Oil and Gas and Midstream and Marketing. However, management trimmed the production outlook, citing Iran-related operational disruption. That adjustment clouded near-term earnings power even as the balance sheet and cash flow looked strong.

The leadership transition adds another layer. Occidental’s board named Chief Operating Officer Richard Jackson to succeed Vicki Hollub as President and CEO, effective June 1, 2026. Hollub will remain on the board following her retirement, ensuring continuity.

On the Q1 call, Hollub said: “I’ve worked with Richard for almost 20 years and have always been impressed with his drive for excellence, his integrity and ethics.” Going forward, investors will watch whether Jackson maintains the same capital discipline that defined Hollub’s decade in charge.

See analysts’ growth forecasts and price targets for OXY (It’s free) >>>

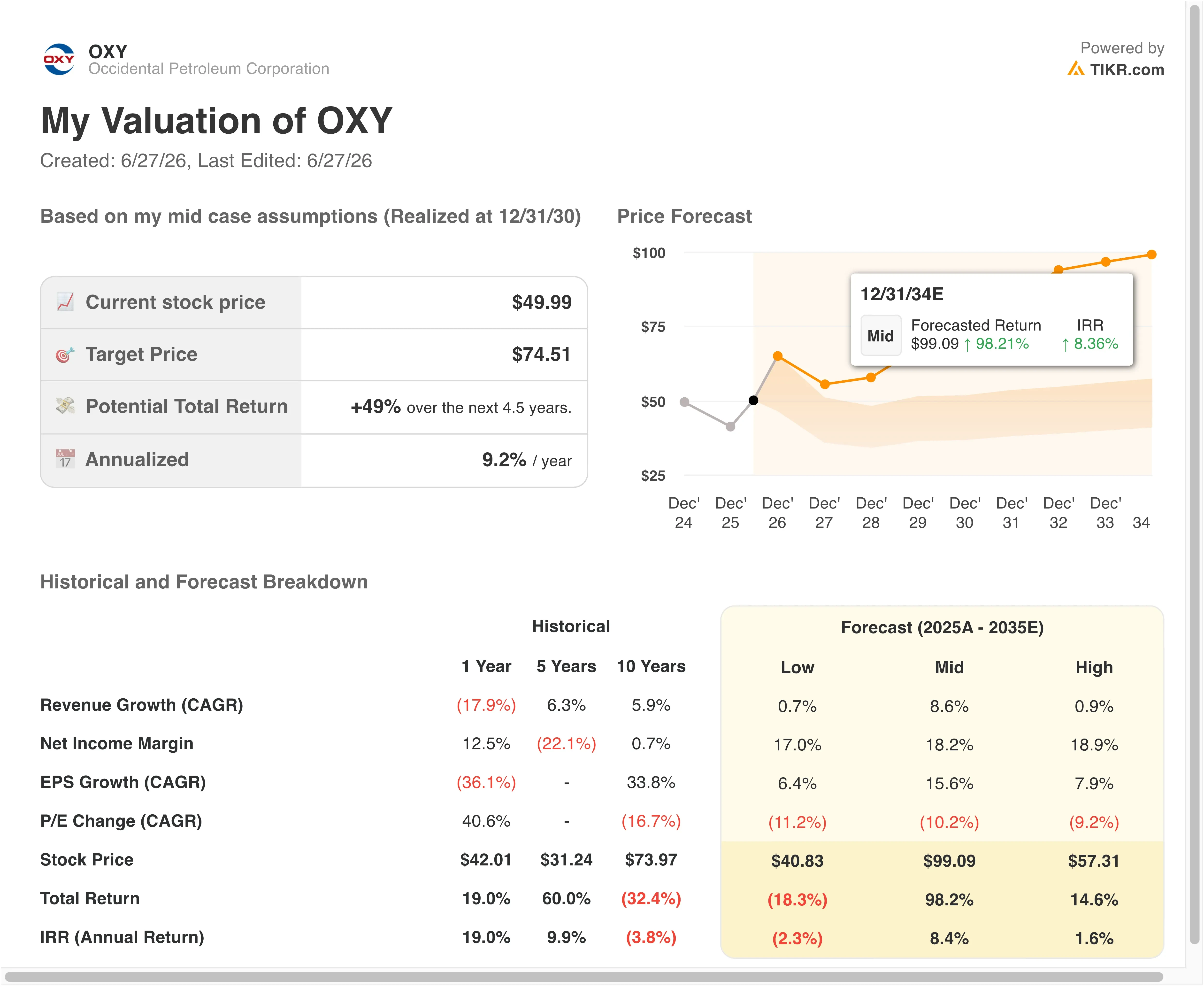

Is OXY Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue Growth (CAGR): 9.0%

- Operating Margins: 31.0%

- Exit P/E Multiple: 8.6x

Based on these inputs, the model estimates a target price of $54, implying an 8.5% total return from the current share price of $50 and an annualized return of 3.3% over the next 2.5 years.

That 3.3% annualized figure sits below what most investors want from a cyclical energy stock. It signals that OXY at $50 is not obviously cheap on a forward-looking basis. The model’s exit multiple of 8.6x reflects the compressed valuations energy companies receive during periods of price uncertainty.

OXY’s operating margin assumption of 31% looks achievable if crude stays range-bound. The 27.1% LTM EBIT margin shows the business is already running close to that target. But the five-year historical margin picture was painful, with negative free cash flow tied to the CrownRock leverage cycle. Margin recovery is a process here, not a finished story.

Revenue growth is the bigger swing factor. OXY’s realized oil price in Q1 averaged $69.91 per barrel, lagging broader crude benchmarks even as the Iran conflict pushed prices higher. If the ceasefire holds and oil drifts lower, OXY’s revenue could disappoint the model’s 9% CAGR assumption. Management did reduce principal debt to $13.3 billion, down $7.5 billion since December, which meaningfully improves the earnings floor.

See how OXY compares to other energy stocks on TIKR’s free stock screener >>>

OXY vs. the Energy Majors: Exxon and Chevron

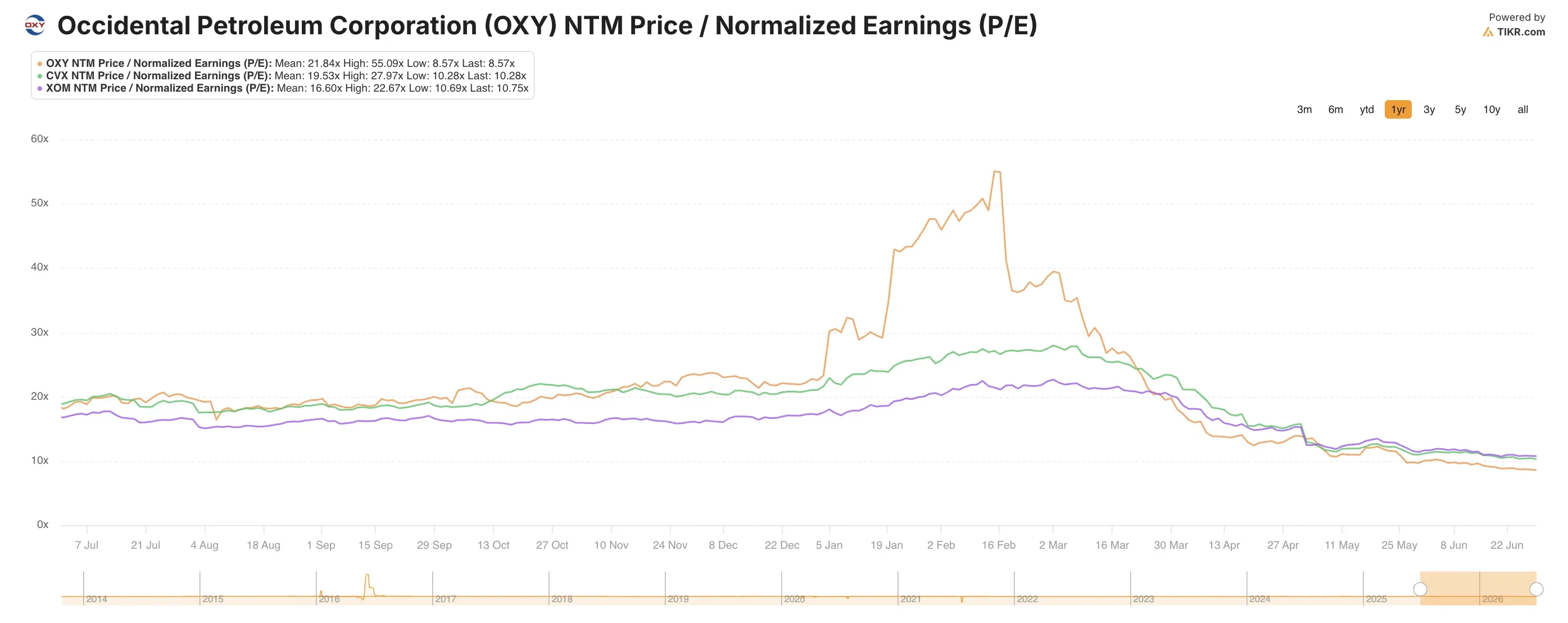

Exxon Mobil (XOM) and Chevron (CVX) are OXY’s most direct large-cap comparators. Exxon trades at roughly 14x forward earnings, and Chevron trades near 13x. Both command meaningful premiums to OXY’s NTM P/E of approximately 8.6x. That discount reflects OXY’s higher leverage and greater oil-price sensitivity, since the company carries more net debt relative to EBITDA than either major.

Devon Energy is a better shale comparison for OXY’s U.S. onshore business. Devon trades at similar or slightly higher forward multiples, reflecting its cleaner balance sheet. OXY’s LTM net debt to EBITDA stands at 1.09x today, which is lean by historical standards. But the market still prices in cycle risk, and that compression versus Exxon and Chevron reflects lingering caution.

Where OXY stands apart is in its direct air capture business and its former OxyChem segment. The Q1 release included a gain from the OxyChem sale within discontinued operations. That gain helped lift the headline net income figure above the adjusted number. The carbon removal optionality differentiates OXY from Devon, but it does not yet move the valuation needle for most investors.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What’s Driving OXY Stock Going Forward?

The biggest near-term catalyst is the Q2 earnings report, expected August 6, 2026. Analysts will watch whether the production trim proves to be a one-quarter issue. Jackson’s first full period as CEO will also draw scrutiny, since investors want continuity in capital discipline and free cash flow priorities.

Oil price direction will matter just as much as any company-specific development. OXY scrapped new hedges during Q1 given price volatility, so the second half of 2026 is fully exposed to spot prices. The company reported lower realized oil prices even as the Iran conflict drove up crude benchmarks, which means its exposure is real and asymmetric. A sustained price decline would hurt earnings more than the Q1 beat suggests.

Capital allocation is also developing in interesting ways. Occidental completed cash tender offers for senior notes in early 2026, continuing its deleveraging effort. Lower interest expense directly boosts free cash flow available for dividends and buybacks. The quarterly dividend of $0.26 per share represents a yield of roughly 2.1% at current prices.

Jackson’s strategic moves will attract attention as his tenure matures. He has emphasized continuity, but investors will listen for any shift in acquisition appetite. Occidental’s 10% stake in an Exxon deepwater block offshore Trinidad suggests the new team is still willing to add to the portfolio. That international exposure adds diversification but also complexity, and managing both will define whether the new CEO earns a re-rating over the next two years.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Occidental Petroleum?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up OXY, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track OXY alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze OXY stock on TIKR Free→

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!