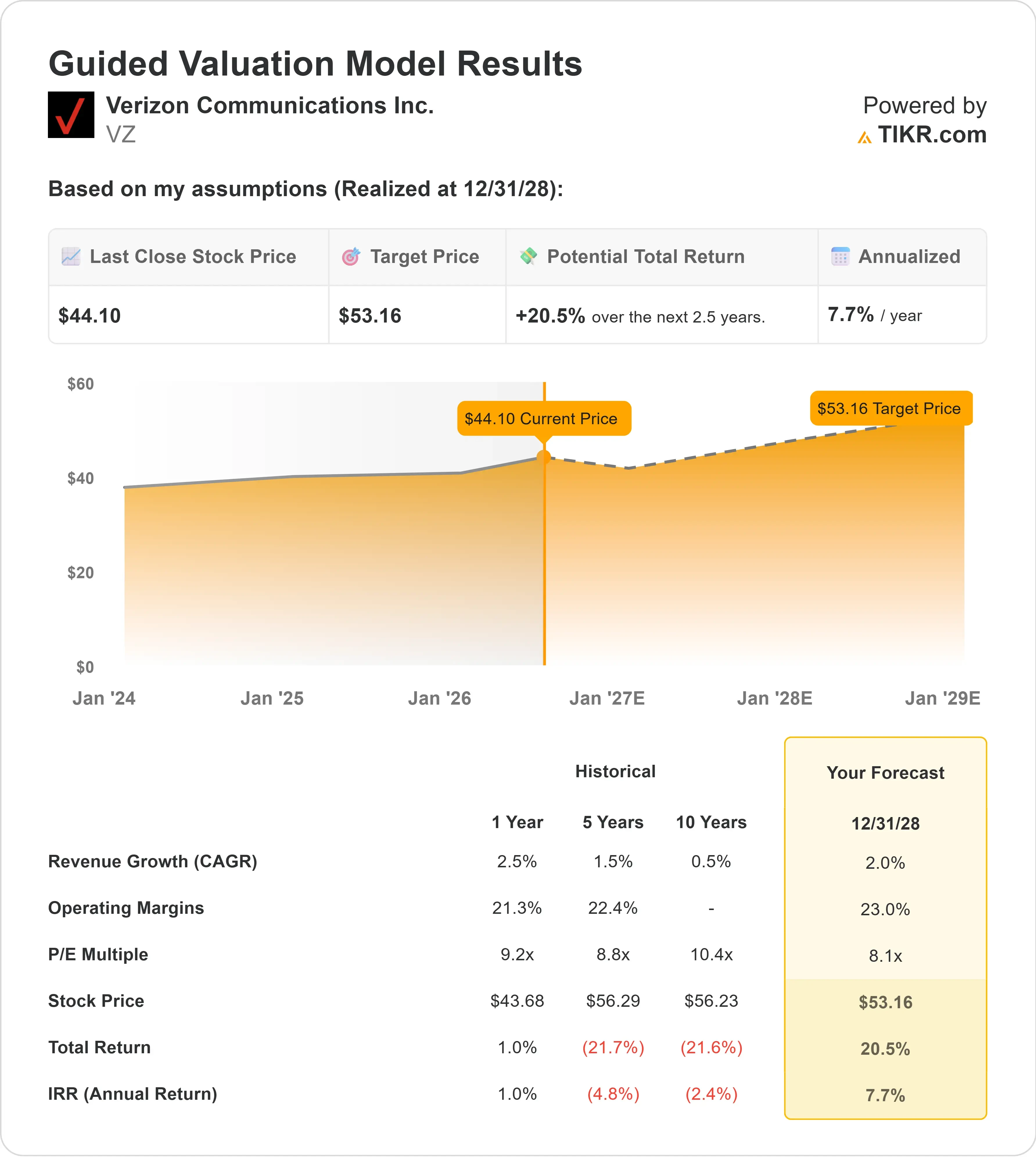

Key Stats for Verizon Stock

- Today’s Performance: -6%

- 52-Week Range: $38 to $52

- Valuation Model Target Price: around $53

- Implied Upside: around 21%

Analyze your favorite stocks like Verizon Communications with TIKR (It’s free) >>>

What Happened?

Verizon Communications Inc. stock fell about 6% today, trading near $44 per share, as investors treated the defensive telecom name like a company facing a fresh credibility test. The market is reacting to weaker index demand after Verizon’s Dow exit, expected Q2 charges tied to its BT Group joint venture, and whether CEO Daniel Schulman’s turnaround can keep improving churn, costs, and free cash flow.

The stock dropped because Verizon officially left the Dow Jones Industrial Average, with Alphabet replacing the company before trading opened on June 29. That created immediate index-rebalancing pressure from funds tied to the benchmark, while Verizon’s expected Q2 loss tied to the BT transaction gave investors another reason to sell a stock already being judged on dividend safety, cash flow, and execution.

Verizon also announced a 50:50 international enterprise joint venture with BT Group that will serve more than 3,000 customers across more than 180 countries and represent about $4 billion in combined annual revenue. Verizon agreed to pay BT a $625 million equalization payment, and the deal is expected to close in 2027, pending regulatory approvals and employee consultations. The near-term concern is that Verizon expects a $700 million to $800 million Q2 loss tied to reclassifying assets for the planned venture, shifting attention to reported earnings pressure before investors see the longer-term strategic benefit.

The selloff comes even as management has been trying to reset the Verizon story around customer retention, operating efficiency, and free cash flow. At a recent J.P. Morgan conference, CEO Daniel Schulman said, “Our turnaround is on track,” after Verizon returned to postpaid phone subscriber growth in Q1 for the first time in 13 years, reduced Consumer churn from 95 basis points in Q4 to 90 basis points in Q1, guided for free cash flow growth of at least 7%, and raised adjusted EPS growth guidance to 5% to 6%.

That churn improvement matters because Verizon competes directly with AT&T and T-Mobile for the same U.S. wireless subscribers. Lower churn means fewer customers leaving, lower replacement costs, and better support for margins, which is especially important for a company valued around free cash flow and dividend durability. Verizon’s next major test is Q2 earnings on July 24, when the market will get a clearer look at wireless subscriber trends, free cash flow, and whether the BT-related pressure is mostly one-time or a sign of deeper earnings pressure.

Value Verizon Communications instantly (Free with TIKR) >>>

Is Verizon Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth: around 2%

- Operating Margins: around 23%

- Exit P/E Multiple: 8x

Verizon’s revenue outlook is modest, but that fits the business because telecom growth is usually driven by wireless service revenue, broadband additions, and customer retention rather than rapid new-market expansion.

The around 2% revenue growth assumption depends on Verizon keeping postpaid phone trends positive, growing fixed wireless and broadband, and reducing churn so the company spends less replacing lost customers.

See analysts’ growth forecasts and price targets for Verizon Communications (It’s free) >>>

The around 23% operating margin assumption depends on management turning cost cuts into lasting efficiency gains without weakening the network or customer experience.

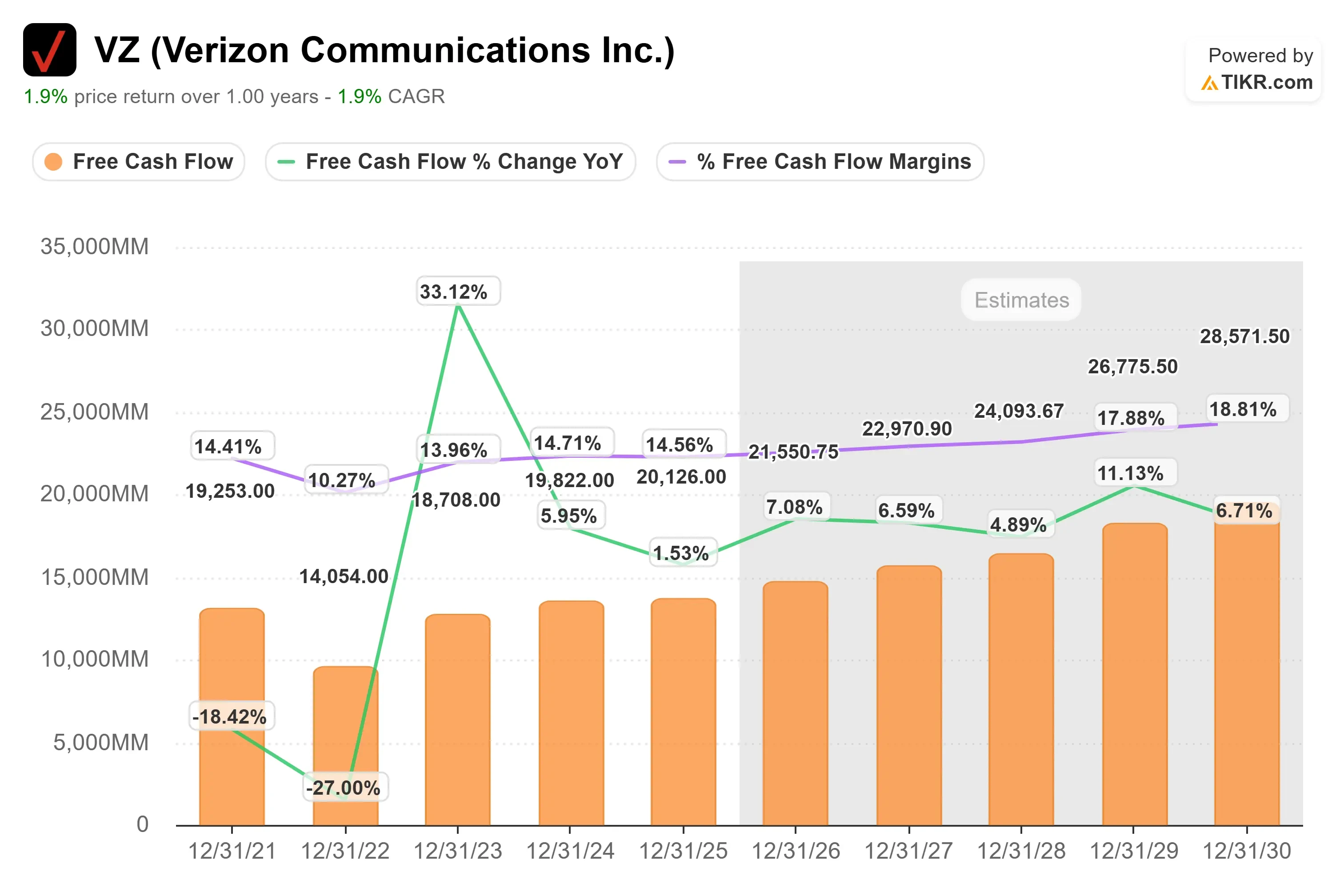

The free cash flow chart better supports the Verizon story than a revenue chart because the company is mainly valued on cash generation, dividend durability, and debt reduction rather than fast top-line growth.

Based on these inputs, the model estimates a target price of around $53, implying about 21% total upside, which suggests Verizon looks modestly undervalued at current prices.

At current levels, Verizon’s upside is likely driven less by fast revenue growth and more by stable free cash flow, debt reduction, dividend support, lower churn, and cleaner execution after the Dow removal and BT transaction.

How Much Upside Does VZ Stock Have From Here?

Investors can estimate Verizon Communications’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Verizon Communications in under 60 seconds with TIKR (It’s free) >>>