Key Stats for Con Edison Stock

- Past-Week Performance: +2.4%

- 52-Week Range: $94.5 to $115.3

- Current Price: $112.5

What Happened?

Con Edison (ED) just committed $37.7B in capital investment through 2030 while simultaneously raising $775.7M through a February 24 equity offering, signaling that the grid modernization buildout is accelerating faster than internally generated cash can fund it, as ED trades at $112.49.

On February 19, Con Edison reported a Q4 adjusted EPS miss of $0.89 against a $0.95 consensus estimate, hurt by operating expenses rising to $3.51B from $3.16B and interest expense climbing to $313M, yet guided 2026 adjusted EPS to $6.00–$6.20.

Still, full-year 2025 adjusted EPS of $5.70 landed at the top end of guidance, net income grew 11.2% to $2.02B, and management locked in a 6%–7% five-year EPS CAGR target anchored to the midpoint of that 2026 range.

On February 23, Jefferies raised its price target to $118 from $112 while reiterating Hold, calling ED the best “anti-data center” trade and citing a recently approved three-year rate case that supports earnings stability through 2028.

Kirk Andrews, SVP and CFO, stated on the Q4 2025 earnings call that “we expect five-year adjusted profit per share to grow at a compounded annual rate target of 6 to 7 percent with the midpoint of our 2026 adjusted EPS guidance as a baseline,” directly underpinning the $6.6B capital deployment plan for 2026 alone.

With 52 straight dividend increases, a rate-case approval that raised its authorized ROE, and $24.3B committed for 2028–2030, Con Edison is converting New York City’s electrification demand into a long-duration regulated earnings compounder.

Wall Street’s Take on ED Stock

The $37.7B capital commitment through 2030, funded partly by the February 24 equity offering, forces a re-evaluation of Con Edison from a slow-growth utility into a multi-year infrastructure compounder with rate-case-protected returns.

Revenue grew 10.9% in 2025 to $16.9B, and consensus projects $17.2B in 2026, while EPS compounded at 6.4% annually over five years and forward estimates call for $6.07 in 2026, up from $5.70 in 2025.

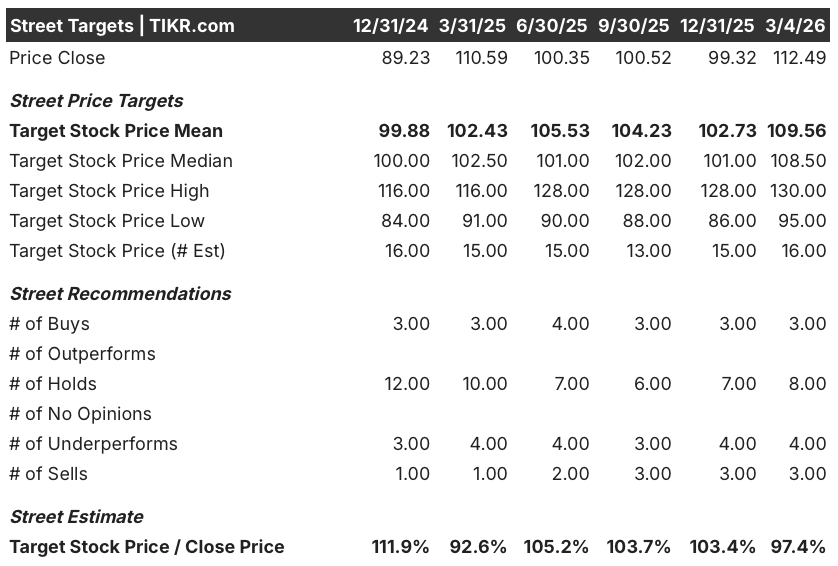

Currently, Wall Street carries 3 Buys, 8 Holds, 4 Underperforms, and 3 Sells across 16 analysts, with a mean price target of $109.6 implying 2.6% downside from $112.49, as the consensus waits for evidence that $6.6B in 2026 capex translates into authorized ROE expansion beyond 2028.

The $130 bull target rests on the approved rate plan and 52 straight dividend increases driving a re-rating, while the $95 floor reflects the risk that post-2028 rate negotiations stall on affordability concerns.

What Does the Valuation Model Say?

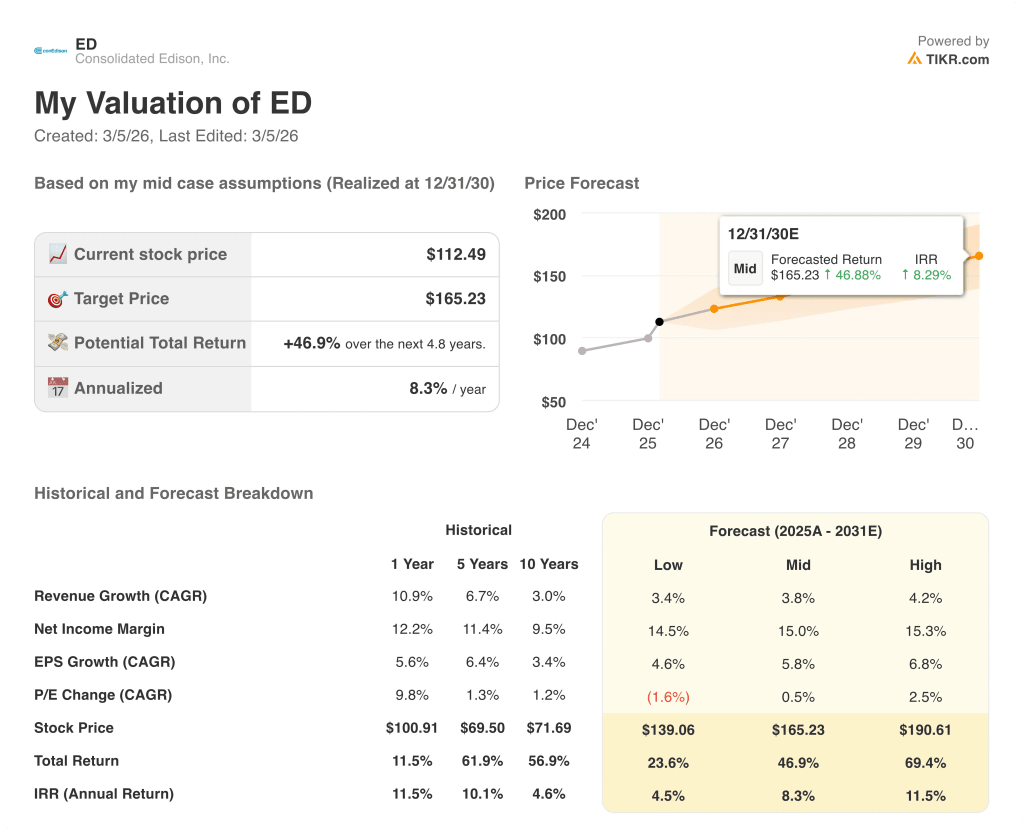

TIKR’s mid-case model targets $165.23 by December 31, 2030, a 46.9% total return from current levels. An 8.3% annualized IRR is unusually strong for a regulated utility trading at $112.49.

The market is underpricing the earnings durability embedded in the newly approved rate case, which raised Con Edison’s authorized ROE and locked in revenue visibility through 2028.

The P/E expanded from 16x to 19x in just three months, yet the stock still trades 2.6% below the analyst mean target of $109.6: this suggests that the multiple expansion has not caught up to the improved regulatory backdrop.

Management’s decision to hit the top end of 2025 adjusted EPS guidance while simultaneously committing $24.3B in capital for 2028–2030 confirms this is a growth story in utility packaging, not a stagnant income play.

The single most credible risk is that the post-2028 rate-case cycle requires higher capital spending approval that regulators deny, potentially compressing the 6%–7% EPS CAGR target and pressuring the $130 high target scenario.

The forward catalyst to watch is the settlement timing of the February 24 forward equity agreement, which must occur by December 31, 2026, and will confirm whether capex deployment stays on schedule.

ED is a regulated compounder with 52 years of dividend growth and a $37.7B investment pipeline; monitor authorized ROE trends in the next rate-case filing as the key valuation driver.

Should You Invest in Con Edison Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ED stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Con Edison Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ED stock on TIKR for Free →