Key Takeaways for Cloudflare Stock as of July 2026

- 17 buys, 6 outperforms, 9 holds, 1 underperform, 1 sell cover Cloudflare stock, with a mean target of $243.65, just below the current $246.31 price.

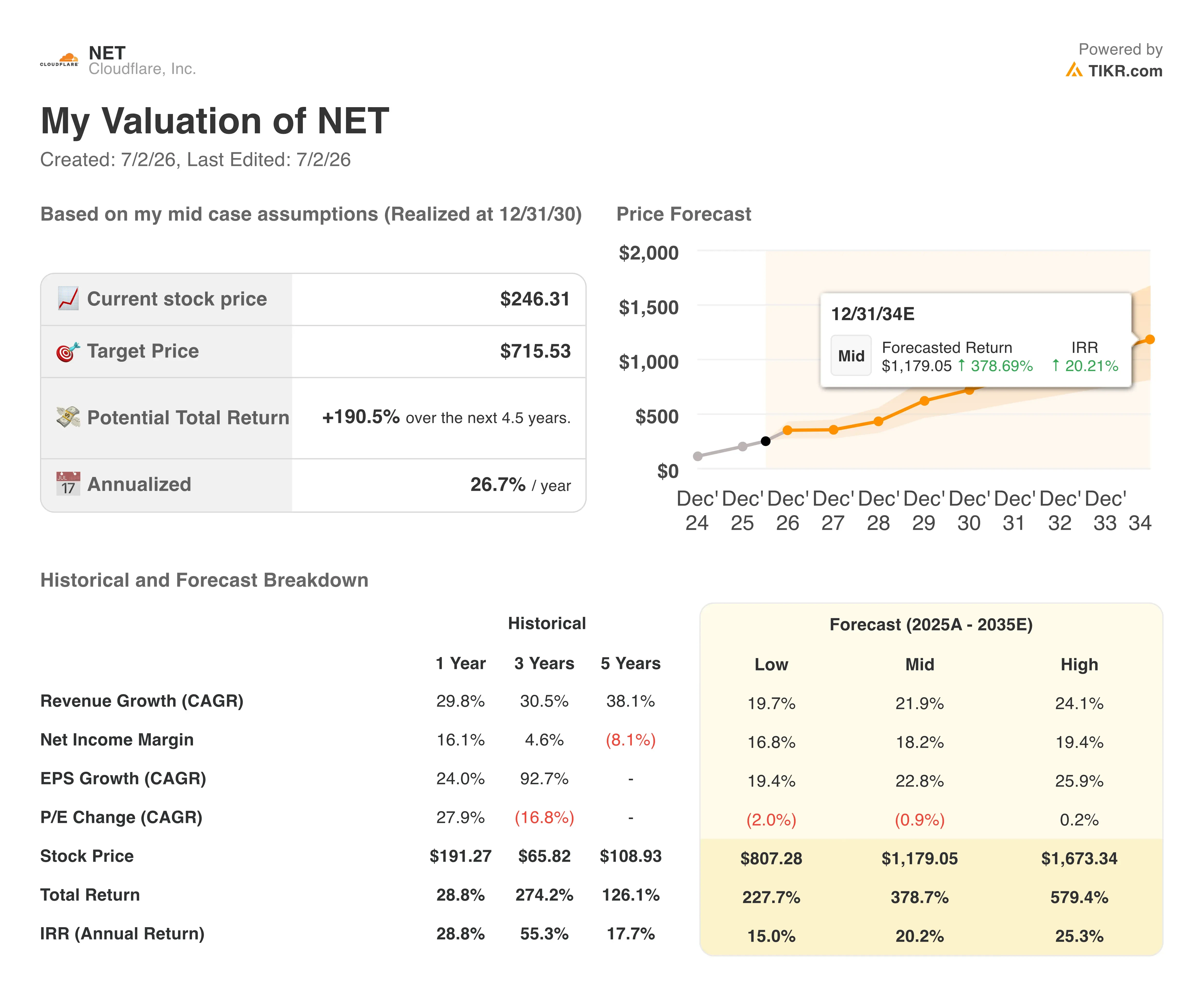

- Following a Q1 print that beat consensus revenue by $18 million, TIKR’s mid-case model targets $716 by December 2030, a 191% total return, or 27% annualized.

- Cloudflare stock looks fairly valued to slightly ahead of itself here: EBITDA consensus calls for $150 million in the September quarter, up 32% year over year, but the stock already trades near the Street’s mean target.

- Matthew Prince cut headcount by roughly 20% on the Q1 call while guiding full-year revenue to $2.805 billion to $2.813 billion, betting that agentic AI infrastructure spend offsets the restructuring charge.

Cloudflare Stock Absorbs a 1,100-Person Cut While Guiding for 30% Growth

Cloudflare (NET) operates a global network that sits in front of roughly 20% of the internet, selling security, performance and developer tools to companies that need to protect and accelerate their websites and applications.

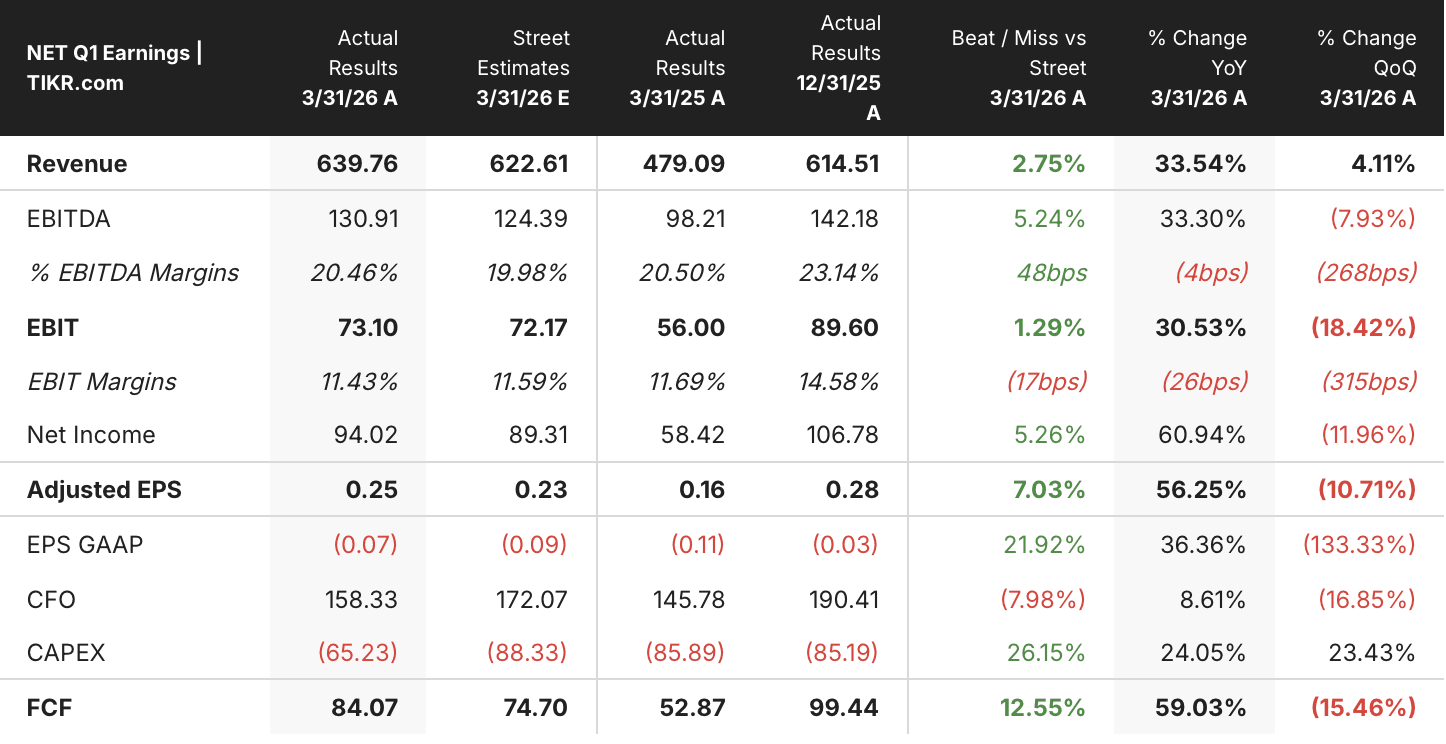

The company posted first quarter 2026 revenue of $639.8 million, up 34% year over year and ahead of the $621.9 million analysts had modeled.

That beat came alongside a decision that overshadowed the print itself. CEO Matthew Prince announced a reduction of more than 1,100 employees, about 20% of Cloudflare’s workforce, tied to what he called a shift to an “agentic AI-first operating model.”

Prince framed the cuts as a productivity story rather than a cost-cutting one. On the Q1 earnings call, he told investors: “I think just because you’re fit doesn’t mean you can’t get fitter.” The restructuring will run $140 million to $150 million in charges for the year, concentrated in the second quarter, with about $40 million of that non-cash.

Sales capacity was explicitly protected. CFO Thomas Seifert said the company touched “hardly” any quota-carrying account executive roles, instead cutting support ratios that no longer scale the same way once AI tools handle more of the workload.

The number that matters most sits underneath the headline cut. Cloudflare’s $100,000-plus customer count grew 25% year over year to 4,416, and customers spending over $5 million annually grew 50%, with the company adding as many of those accounts in Q1 alone as it did in all of 2025.

Net retention held at 118%, and Q2 guidance calls for revenue of $664 million to $665 million, 30% growth. Full-year guidance sits at $2.805 billion to $2.813 billion, also implying 30% growth at the midpoint, a number Cloudflare set even as it absorbed the restructuring charge into the same guide.

Wall Street Analysts Are Split on Cloudflare Stock After a Run to $246

Wall Street’s coverage of Cloudflare stock leans bullish but has grown more divided over the past year, with 17 buys and 6 outperforms against 9 holds, 1 underperform and 1 sell. The mean target of $244 sits just below the current price of $246, implying essentially no upside from here at the average estimate.

That mean has moved sharply, rising from $156 a year ago to $244 today as the stock climbed from $196 to $246 over the same period. The gap between target and price has closed from 80% upside a year ago to under 1% today, with 31 analysts still covering the name and the high target sitting at $305.

Wall Street Expects Cloudflare Stock’s EBITDA to Grow 25% Through Q3 2026

Cloudflare posted EBITDA of $130 million in the March 2026 quarter, up 33% year over year and representing a 21% margin, the softest EBITDA margin of the past five quarters shown in the data.

Consensus expects that to reaccelerate to $150 million in the September quarter, 32% growth, with margins recovering to 25%. By December 2026, EBITDA is modeled at $200 million, 42% growth, with margins climbing to 26%, the fastest EBITDA growth rate in the forward estimate table.

The trajectory extends further out. Analysts model EBITDA of $230 million by June 2027, 59% year-over-year growth, with margins reaching 28%, even as revenue growth is expected to moderate from 30% to 28% over the same window.

That EBITDA growth outpaces revenue growth by roughly 30 percentage points within a year, and the G&A and support-ratio cuts Seifert flagged on the Q1 call have to actually show up in the numbers to fund it.

Cloudflare Stock’s EBITDA Still Trails Fortinet and Palo Alto Networks by a Wide Margin

Cloudflare’s EBITDA reached $130 million in the March 2026 quarter, well behind Fortinet’s (FTNT) $580 million and Palo Alto Networks’ (PANW) $840 million over the same period

That gap persists through the forecast: consensus models Cloudflare’s EBITDA at $230 million by June 2027, against $750 million for Fortinet and $1.42 billion for Palo Alto Networks, leaving Cloudflare the smallest of the three on absolute EBITDA even as its growth rate outpaces both peers.

TIKR’s $716 Target on Cloudflare Stock Holds if the Restructuring Delivers Margin

TIKR’s mid-case model values Cloudflare at $716 by December 2030, a 191% total return from the current price of $246, or 27% annualized over 4.5 years.

That annualized return sits well above the 21% IRR the same model shows for the trailing three-year period, when Cloudflare stock already delivered a 274% total return.

Cloudflare stock has to sustain revenue growth near 22% annually under TIKR’s mid case, below the 34% posted in Q1, while net income margin expands from negative territory over the trailing five years to a modeled 18%.

That combination is only reachable if the headcount reduction lowers the cost structure the way Seifert described without slowing the sales capacity growth Mark Anderson detailed at Investor Day, since the model’s return depends on margin expansion carrying more of the weight as revenue growth normalizes.

Should You Invest in Cloudflare, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cloudflare, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cloudflare, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NET stock on TIKR for Free →