Key Takeaways for Walmart Stock as of June 2026

- 28 analysts rate Walmart stock a buy against just 1 sell across a 41-name coverage list, with the mean target of $139 implying 22% upside from the June 30 close of $113.

- Yet free cash flow swung negative $1.9 billion in Q1, missing estimates by 171%.

- Trading 22% below the Street’s mean target, Walmart stock still looks priced right on EBITDA, up 9% year over year last quarter and set to reaccelerate toward 11% growth by July 2027.

- By January 2031, TIKR’s mid-case model targets Walmart stock at $148, a 30% total return worth 6% annualized.

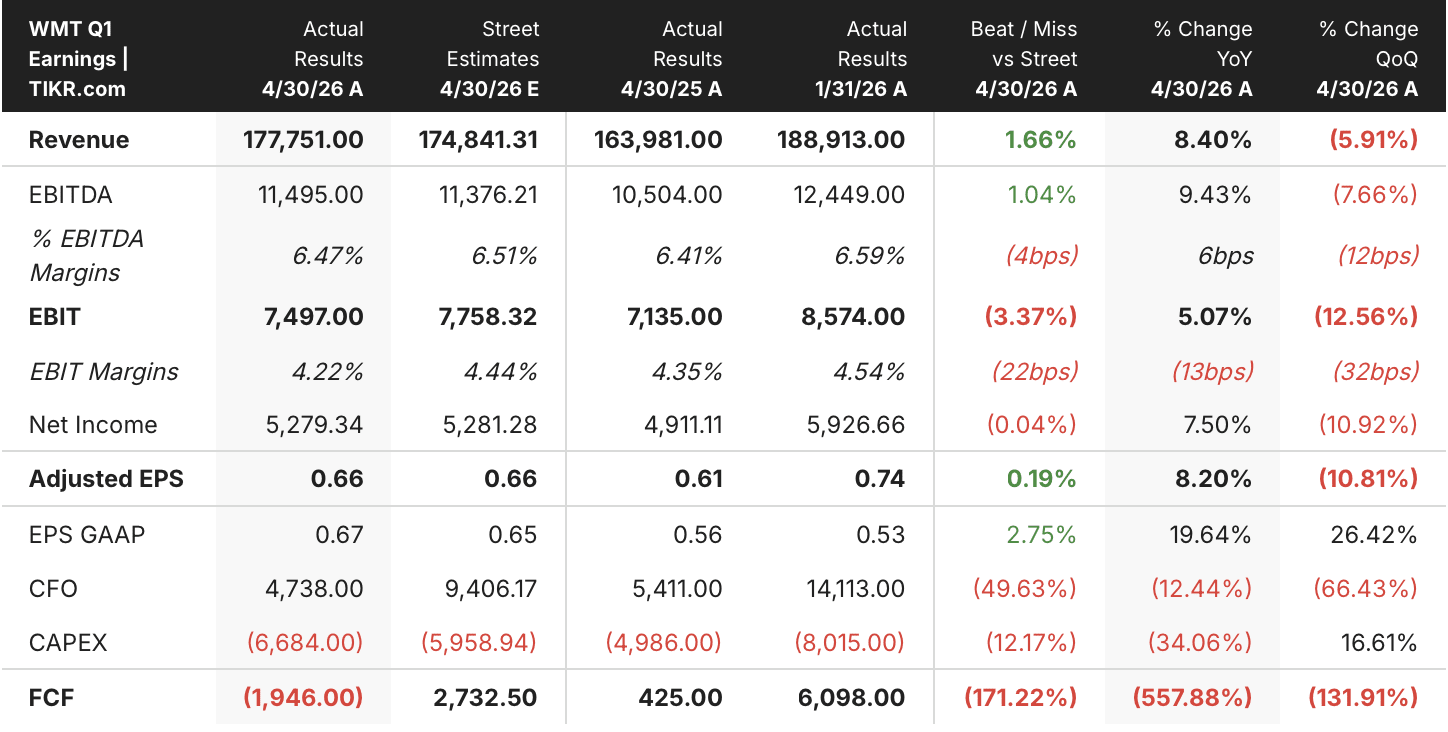

Walmart Stock Falls 14% as a Free Cash Flow Miss Overshadows Q1’s EBITDA Beat

Walmart (WMT) closed at $113.26 on June 30, 2026, down 14% from the $131.93 level it traded at just two months earlier. That slide came despite a Q1 fiscal 2027 print, reported May 21, that beat on the top line and on EBITDA.

Revenue hit $177.75 billion, topping the Street’s $174.84 billion estimate by 1.66% and climbing 8.4% year over year. EBITDA reached $11.495 billion, ahead of the $11.376 billion consensus and up 9.43% from a year ago. Adjusted EPS of $0.66 matched estimates exactly, while GAAP EPS of $0.67 beat by 2.75%.

The tension sits below the operating line. EBIT of $7.497 billion missed the Street’s $7.758 billion estimate by 3.37%, and CFO John Rainey pointed to roughly $175 million in unplanned fuel costs across global distribution and fulfillment. Cash flow took a bigger hit: operating cash flow of $4.738 billion missed estimates by 49.63%, and free cash flow fell to negative $1.946 billion against a Street estimate of positive $2.733 billion, a 171% miss. Capital expenditures of $6.684 billion, tied to automation and fulfillment center buildouts, ran well ahead of plan.

Management framed the miss as timing, not deterioration. Addressing concerns about the path to double-digit operating income growth, Rainey told analysts on the Q1 earnings call, “We are probably as excited about the potential for our business today than at any point in time in the last few years.” The company reiterated full-year guidance of 3.5% to 4.5% constant-currency sales growth and 6% to 8% operating income growth, guiding Q2 operating income growth of 7% to 10%.

Behind that confidence is a shifting profit mix. Advertising grew 36% in Walmart U.S., membership fee revenue rose 17% enterprise-wide, and those two categories alone made up roughly a third of operating income in the quarter. Marketplace sales grew nearly 50%. U.S. eCommerce incremental margins ran near 12%. That’s operating leverage showing up in EBITDA, long before it ever reaches free cash flow.

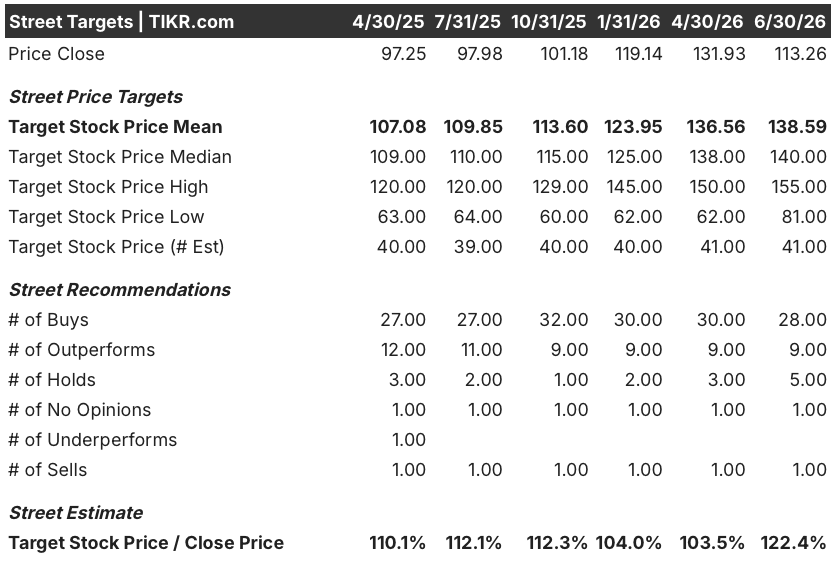

Wall Street Rates Walmart Stock a Buy With a Widening Gap to Its Mean Target

Walmart stock carries 28 buy ratings and 9 outperform ratings against just 5 holds, 1 no opinion, and 1 sell as of June 30, 2026, one of the more lopsided splits in large-cap retail.

The mean target price sits at $139, up from $137 three months earlier even as the stock fell 14% over the same stretch and that combination pushed the target-to-close ratio to 122%, up from 104% at the end of April, meaning analysts grew more confident on Walmart stock precisely as the market grew less so.

Wall Street Expects Walmart Stock’s EBITDA to Reaccelerate Toward 11% Growth by Mid-2027

Walmart posted $11.495 billion in EBITDA in the quarter ended April 30, 2026, up 9.43% year over year and ahead of the Street’s estimate. Consensus now expects EBITDA of $12.41 billion for the quarter ending July 31, 2026, up 9% from a year earlier, followed by $11.92 billion in the October quarter, a step down to 7.4% growth in the January 2027 quarter, then $13.37 billion.

From there, the estimates climb faster. Analysts model $12.42 billion in EBITDA for the April 2027 quarter, up 8%, before growth accelerates to 11.4% in the July 2027 quarter at $13.83 billion. That path implies the Street sees this quarter’s fuel and capex pressure as transitory rather than structural.

That back-half reacceleration only happens if advertising, membership, and marketplace keep compounding at their current pace. If automation-driven capex stays elevated, the pressure just shows up further down the income statement while the EBITDA line keeps looking fine

TIKR’s $148 Target on Walmart Stock Holds if EBITDA Keeps Outrunning Capex

TIKR’s mid-case model values Walmart stock at $148 by January 2031. That’s a 30% total return from the current price of $113, or 6% a year over roughly 4.6 years.

That 6% is well below Walmart stock’s own 5-year annualized return of 19.4%. The target reads as cautious, not a sign the growth story is over. It’s a conservative number for a stock still digging out of a rough cash flow quarter.

Getting there means EBITDA keeps growing faster than capex and fuel costs weigh on the business. Advertising and membership need to keep compounding well ahead of the core retail business. Free cash flow already swung from positive $6.10 billion in January to negative $1.95 billion in April. The Street sees it bouncing back to $5.49 billion by July. That recovery will say a lot about whether April was a blip or the new normal.

Should You Invest in X?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up X stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track X alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze WMT stock on TIKR for Free →