Key Stats for CAVA Stock

- Year-to-Date Performance: 41%

- 52-Week Range: $43 to $102

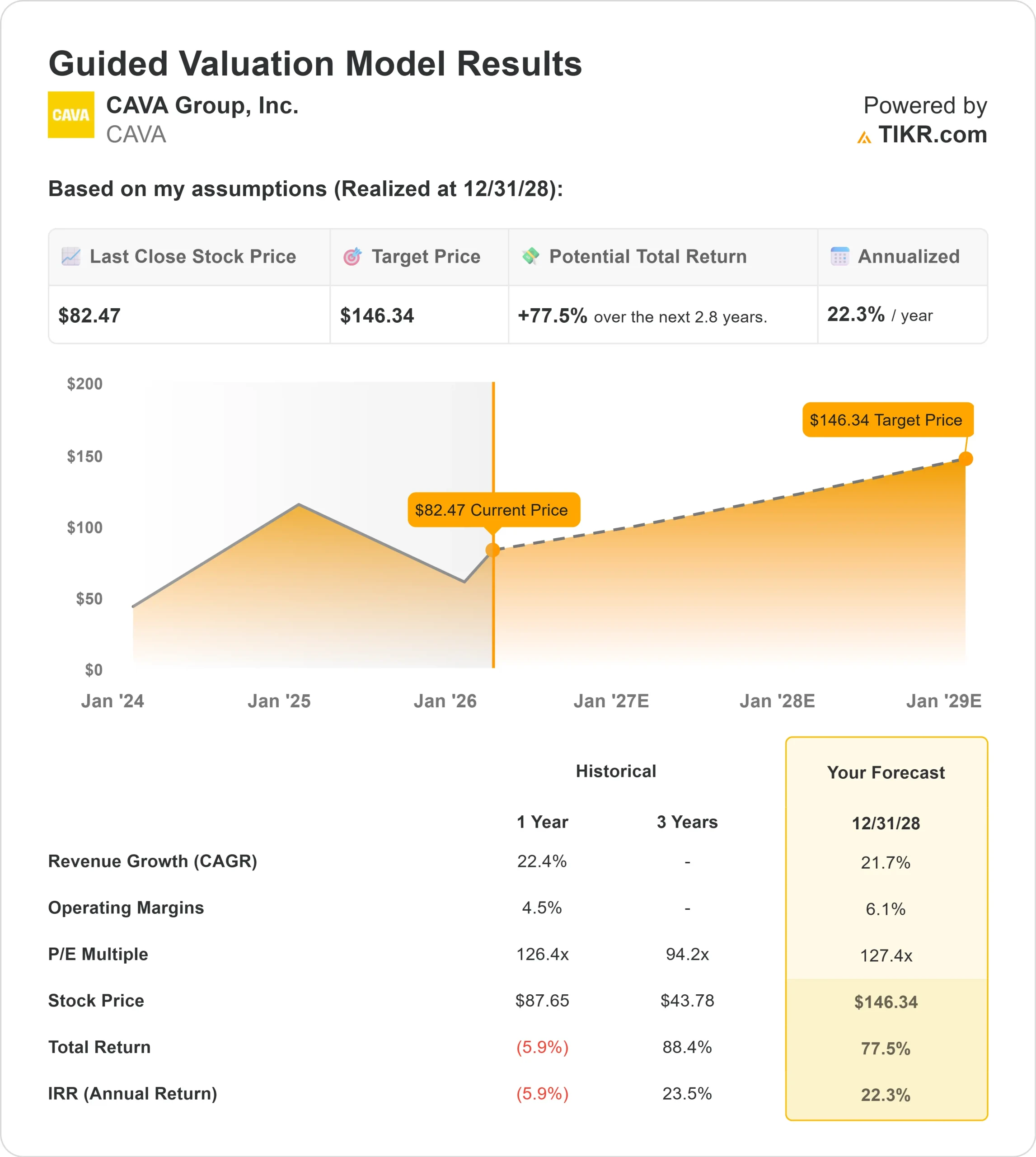

- Valuation Model Target Price: $146

- Implied Upside: 78%

Value your favorite stocks like CAVA Group with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

CAVA Group stock is up about 41% year to date, recently trading near $82 per share, as investors responded to strong earnings growth, accelerating restaurant expansion, and multiple upward analyst price target revisions.

The rally reflects growing confidence in the company’s ability to scale nationally while sustaining double-digit revenue growth.

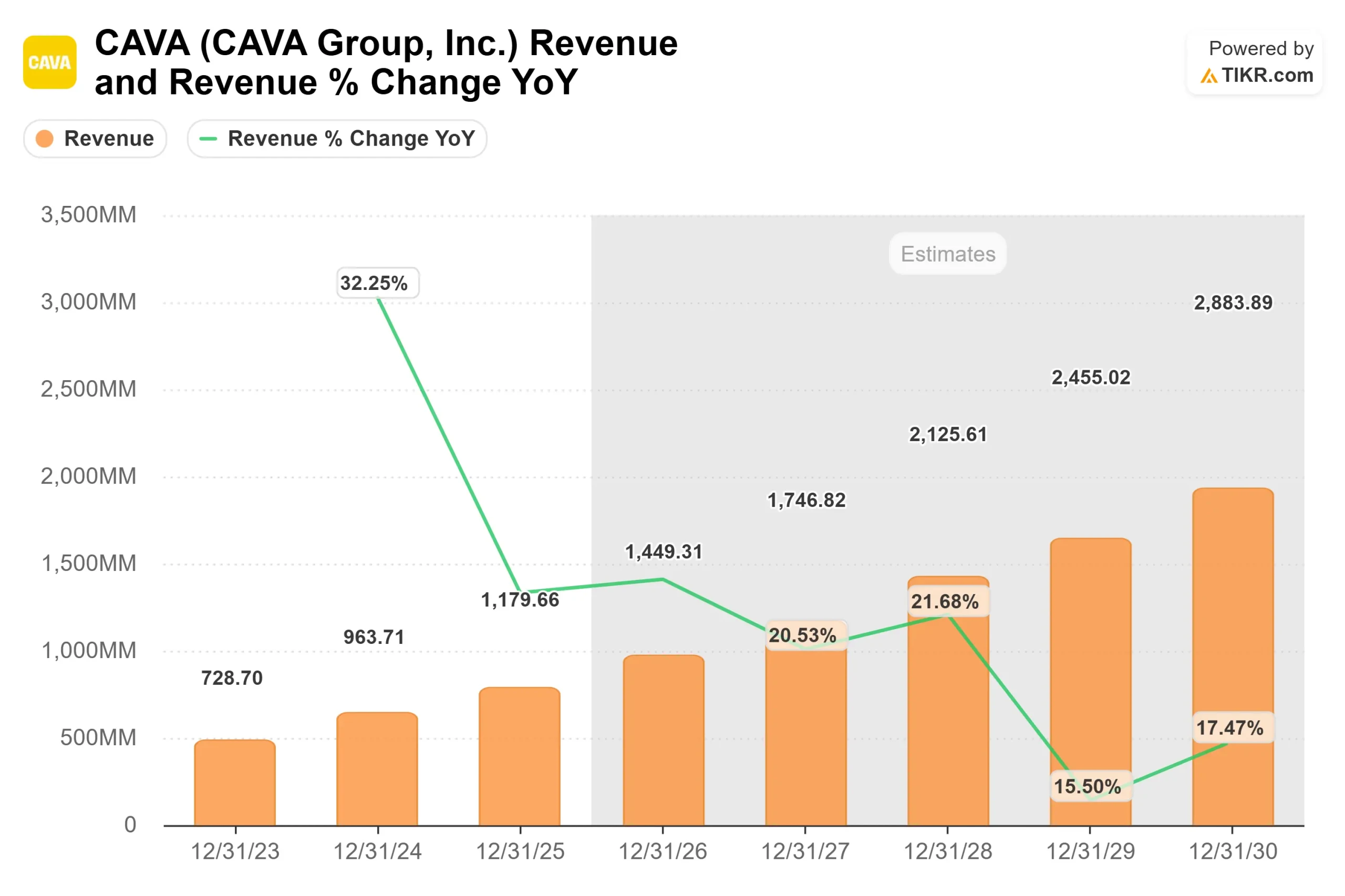

Shares moved higher after CAVA reported Q4 revenue up 21.2% year over year to $272.8 million and full-year revenue growth of 22.5%, pushing annual sales above $1 billion for the first time.

Same-restaurant sales increased 0.5% in Q4 and 4% for the full year, while net income reached $63.7 million and adjusted EBITDA totaled $152.8 million in 2025.

CEO Brett Schulman called it “a record-setting year,” and management guided 2026 for 74 to 76 net new restaurants, 3% to 5% same-restaurant sales growth, and adjusted EBITDA between $176 million and $184 million, reinforcing expectations for continued expansion this year.

Analyst activity supported sentiment. Sanford C. Bernstein raised its price target from $75 to $84, Morgan Stanley lifted its target to $83 with an equal weight rating, Piper Sandler increased its target to $85 with an overweight rating, Truist raised its target from $78 to $80 while maintaining a buy rating, and Telsey Advisory Group boosted its target from $85 to $88 with an outperform rating.

Consensus across brokers remains a Moderate Buy with average targets clustered in the mid-$80s, placing shares close to current fair value estimates even after the strong year-to-date rally.

Institutional ownership remains elevated. Vanguard increased its stake by 3.5% to 9,345,976 shares, representing about 8.06% of the company, while Citigroup expanded its position by 138.2% to 886,666 shares.

Envestnet Asset Management raised its stake by 57.7%, ABN Amro Investment Solutions boosted holdings by 262.8%, Ameritas Advisory Services increased its position significantly, and Rhumbline Advisers added 9.8%.

Institutional investors now own roughly 73% of the company, underscoring continued professional accumulation even as valuation remains premium at about 153x trailing earnings.

See analysts’ growth forecasts and price targets for CAVA Group (It’s free) >>>

Is CAVA Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 21.7%

- Operating Margins: 6.1%

- Exit P/E Multiple: 127x

Revenue is projected to rise from about $964 million in 2024 to roughly $2.9 billion by 2030, reflecting sustained unit growth and strong new restaurant productivity, with 2025 AUVs trending above $3 million.

The model assumes operating margins expand from about 5.1% today toward the low 6% range as corporate overhead leverages across a larger restaurant base and supply chain efficiencies improve.

Based on these inputs, the valuation model estimates a target price of $146, implying about 78% upside over the next several years, indicating the stock appears undervalued at current levels.

At around $82 per share, the stock trades near 8.2x EV to revenue and about 153x trailing earnings, which reflects a premium multiple. However, that valuation can be supported if CAVA continues delivering 20% plus revenue growth and gradual margin expansion as the system scales.

In 2026, performance will likely be driven by three core areas. First, delivering 74 to 76 new restaurants with productivity near recent levels supports continued revenue acceleration.

Second, same-restaurant sales growth of 3% to 5%, supported by menu innovation such as the Pomegranate-glazed Salmon launch and loyalty engagement initiatives, strengthens operating leverage.

Third, restaurant-level margin guidance of 23.7% to 24.2% will be critical in demonstrating that scale can translate into expanding profitability despite modest inflation and incremental labor investments.

If CAVA sustains strong unit growth while expanding margins gradually, earnings power can compound meaningfully into 2026 and beyond.

At current levels, the stock appears undervalued, with future returns driven primarily by execution on restaurant productivity and margin scaling rather than further multiple expansion.

Estimate a company’s fair value instantly (Free with TIKR) >>>

How Much Upside Does CAVA Stock Have From Here?

Investors can estimate CAVA Group potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See CAVA Group true value, or any stock’s, in under 60 seconds (Free with TIKR) >>>