Key Takeaways for Home Depot Stock as of July 2026

- Home Depot paid approximately $2.3 billion in dividends in Q1 alone, and CEO Ted Decker called the payout “healthy” while deflecting questions about resuming share buybacks.

- The quarterly dividend now stands at $2.33, up from $2.25 two years ago and $2.30 across the prior four quarters.

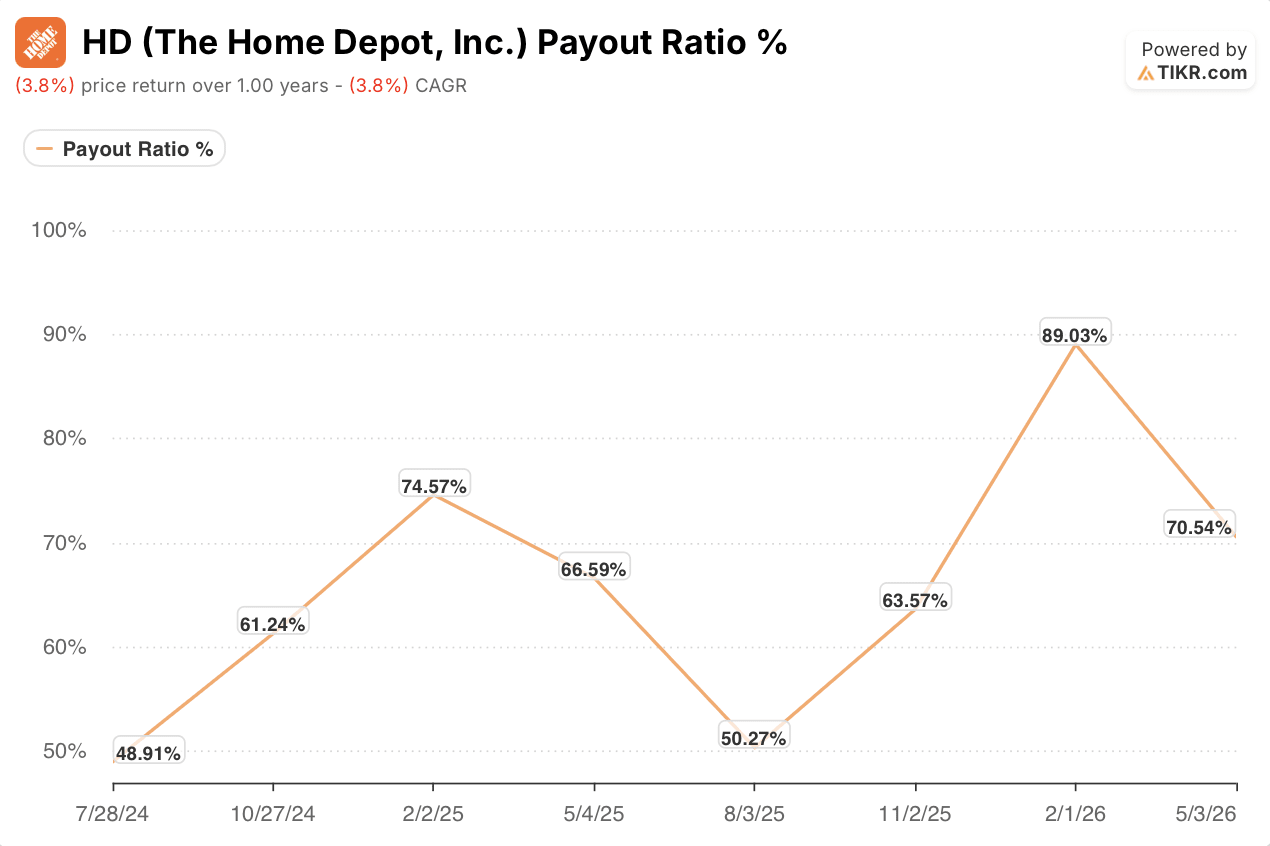

- A 71% payout ratio against a 2.7% yield: stretched for a retailer spending aggressively on acquisitions, but no longer at the 89% peak it hit one quarter earlier.

- TIKR’s mid-case model prices Home Depot stock at $543 by January 2031, a 52% total return that annualizes at 10%.

Home Depot’s Q1 Call Showed a Company Choosing Acquisitions Over Buybacks While Defending Its Dividend

Home Depot (HD) reported $41.8 billion in first-quarter revenue on its Q1 fiscal 2027 call, a 5% increase over the prior year, and disclosed that it returned approximately $2.3 billion in dividends to shareholders during the quarter. That $2.3 billion figure arrived alongside a conspicuous absence: no mention of share repurchases at all.

CEO Ted Decker framed the capital allocation picture plainly on Q1 2027 earnings call when an analyst pressed on whether Home Depot would resume buybacks by 2027. “We certainly pay a healthy dividend at the moment,” Decker told the call. He then redirected to the company’s three-pronged investment strategy: core business, interconnected experience, and winning the Pro customer.

The Pro push absorbed real capital in Q1. Home Depot completed its acquisition of Mingledorff’s, a 42-location HVAC distributor across five Southeastern states, which expanded the company’s total addressable market to $1.2 trillion. SRS, the specialty distribution platform, delivered $4 billion in sales with positive organic growth, though comps turned slightly negative in roofing.

Total company comp sales landed at positive 0.6%, with U.S. comps at 0.4%. Adjusted diluted earnings per share fell to $3.43 from $3.56 a year earlier, a decline CFO Richard McPhail attributed partly to the GMS acquisition’s effect on the gross margin mix. Gross margin dropped 75 basis points year over year to 33%, and adjusted operating margin landed at 12.3%.

Management reaffirmed its full-year guidance: comp sales flat to 2%, total sales growth of 2.5% to 4.5%, and adjusted EPS growth of flat to 4% versus fiscal 2025. McPhail acknowledged “a more volatile external environment” but said the company had “observed kind of the demand that we expected” through the first weeks of Q2.

The message from the call was clear enough: Home Depot is pouring capital into distribution acquisitions and Pro capabilities, not into buying back stock, and the dividend remains the primary vehicle for returning cash to shareholders.

HD Stock Pays $2.33 a Quarter Now, and Its Payout Ratio Finally Stopped Climbing

Home Depot’s quarterly dividend reached $2.33 as of the most recent payment, up from $2.30 across the prior four quarters and $2.25 before that. Each step higher landed while the company was digesting its largest acquisition cycle in decades.

That trajectory looked precarious one quarter ago, when the payout ratio spiked to 89%. It has since dropped to 71%, still elevated by Home Depot’s historical standards but directionally in the company’s favor. The decline coincides with the first full quarter of GMS contribution flowing through the income statement.

A 71% payout ratio leaves less margin for error than the sub-50% levels Home Depot ran at in mid-2024 and mid-2025. But it sits well below the 89% figure that briefly raised questions about whether the dividend could keep growing at all.

Home Depot stock yields 2.7% at its current price of $358. That yield has hovered between 2.5% and 2.9% over the past year, and it sits at the higher end of that range now because the stock price has drifted lower while the dividend moved up.

Whether the payout ratio continues falling depends on whether the EPS trajectory Decker and McPhail guided to, flat to 4% growth for the full year, materializes against a backdrop of rising input costs and still-muted housing turnover.

TIKR’s $543 Target Prices Home Depot Stock for a Rebound That Hasn’t Started Yet

TIKR’s mid-case model sets a $543 target for Home Depot stock by January 2031, implying a 52% total return from the current $358 price, or 10% annualized over 4.6 years.

That return would require Home Depot stock to recover from a stretch where it has lost ground: the stock carries a negative 4% one-year price return as of the model’s creation date. A 10% annualized figure bakes in both capital appreciation and the income from the current 2.7% yield.

Management’s own guidance supplies the building blocks. Revenue growth of 2.5% to 4.5%, SRS delivering mid-single-digit organic growth, and a $1.2 trillion addressable market anchored by the Pro customer all feed the mid-case thesis. If the company’s adjusted EPS growth lands at the top end of its flat-to-4% guide for fiscal 2026, the margin expansion story that the TIKR model requires begins to take shape within the next two years.

Should You Invest in The Home Depot, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up The Home Depot, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Home Depot, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HD stock on TIKR for Free →