Key Stats for Coherent Stock

- Current Price: $333.36

- Target Price (Mid): ~$740

- Street Target: ~$390

- Potential Total Return: ~123%

- Annualized IRR: ~22% / year

- Earnings Reaction: -7.39% (May 6, 2026)

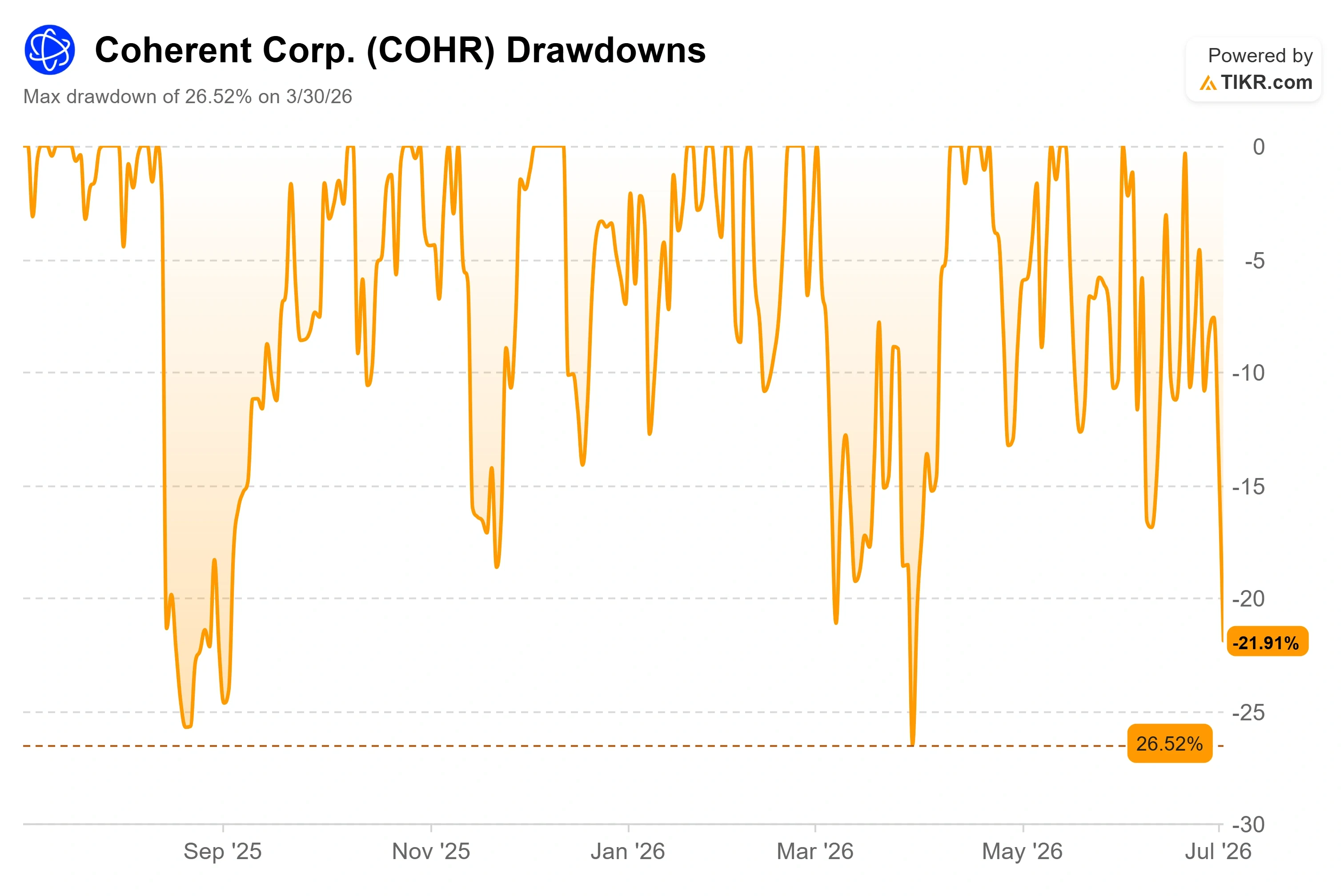

- Max Drawdown: -26.52% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Coherent (COHR) lost nearly a tenth of its value in a single session, and the strangest part is what happened a few hours earlier that same morning. On July 2, the stock closed at $333.36, down 9.57% on the day. Hours before the bell, Raymond James had raised its price target on the shares to $435 from $371 and kept a Strong Buy rating. One desk was marking the stock higher while the tape was marking it sharply lower. That gap is the whole story right now.

The selloff was not about Coherent. The entire AI photonics group dropped together. Applied Optoelectronics fell around 17%, and Lumentum fell around 10% in the same risk-off session, with no company-specific catalyst behind any of the moves. This was profit-taking in a corner of the market that had run up triple digits in 2026, not a crack in the business. That is what makes the drop worth interrogating rather than fearing.

Why Coherent stock fell when nothing changed

The question investors are actually asking is simple. Is a nearly 10% single-day drop in a name with a record order book a warning that the optics trade is topping, or a discount on a structural winner? The bears have a real argument. Coherent trades at a rich multiple, its trailing free cash flow is negative, and public data shows insiders were net sellers over recent months with no buying. After a run this size, there is little room for error if AI spending sentiment softens.

The bulls point to the fundamentals, which did not move on July 2. In its fiscal third quarter, reported May 6, Coherent posted record revenue of $1.81 billion, up 21% year-over-year, with non-GAAP earnings per share of $1.41, up 55%. The Datacenter & Communications segment, its optical products for AI data centers, grew more than 40% year-over-year and made up 75% of revenue.

See historical and forward estimates for Coherent stock (It’s free!) >>>

The backlog is the real signal

Revenue growth was strong, but visibility was the standout. On the earnings call, CEO Jim Anderson described “another step function increase in our order book,” with customer orders now reaching into calendar 2028 and long-term agreements extending to the end of the decade. That matters because it turns a hot quarter into a multi-year pipeline the market can underwrite. Demand, in his words, “remains exceptionally strong with no signs of attenuation.”

The supply side is where the leverage sits. Coherent is racing to expand indium phosphide capacity, the compound semiconductor at the heart of its lasers and the key industry bottleneck. Management now expects to double internal output a full quarter ahead of schedule, then more than double it again by the end of 2027. That is roughly a fourfold increase in two years. The shift to 6-inch wafers is the margin engine underneath it. Anderson put the economics bluntly: “6-inch versus 3-inch is more than 4x as many devices at less than half the cost.” That single line explains both the revenue runway and the gross margin expansion to 39.6% last quarter, with management targeting above 42% over time.

Layered on top is the NVIDIA partnership announced in March, which includes a $2 billion equity investment and a multiyear co-packaged optics supply agreement running through the end of the decade. NVIDIA made a matching $2 billion investment in rival Lumentum the same day, so Coherent is a lead partner rather than an exclusive one. Co-packaged optics, or CPO, moves the laser onto the same package as the switch chip to cut power and boost bandwidth. Coherent sizes that the incremental market is worth more than $15 billion. First CPO revenue starts in the second half of this calendar year, which means the payoff is close enough to model, not a distant promise.

See how Coherent performs against its peers in TIKR (It’s free!) >>>

Is the premium justified

Coherent is not cheap, and the peer comparison shows exactly how much investors are paying for the growth. On a next-twelve-months basis, Coherent trades at roughly 30x EV/EBITDA, against Corning near 32x and Fabrinet near 25x, and its NTM price-to-earnings of about 45x sits well above Eoptolink near 23x. The premium is real. It is defensible only if Coherent’s growth and margins genuinely outpace the group, which the 6-inch cost edge and the NVIDIA-anchored pipeline argue they will. That is a case, not a certainty, and it is the exact case the July 2 tape started to question. With trailing free cash flow still negative as capital spending ramps, the market is paying today for cash flows it expects to arrive later.

TIKR Advanced Model Analysis

- Current Price: $333.36

- Target Price (Mid): ~$740

- Potential Total Return: ~123%

- Annualized IRR: ~22% / year

See analysts’ growth forecasts and price targets for Coherent stock (It’s free!) >>>

Using TIKR’s mid-case scenario, realized in mid-2030, the model points to a target of around $740, an approximately 123% total return, and an annualized IRR of about 22% per year. Two revenue drivers carry the forecast: the transceiver ramp across 800-gig and 1.6T, the data rates moving AI traffic inside data centers, and the newer layers in co-packaged optics and optical circuit switches. The margin driver is the 6-inch indium phosphide transition, which lowers unit cost as it scales across three production sites. The primary risk is valuation compression: at a rich multiple with negative trailing free cash flow, any slip in AI capex or the CPO ramp hits the stock hard. The upside case is that CPO and additional hyperscaler agreements ramp ahead of plan, and margins push past the 42% target. The downside case is that capacity expansion outruns demand, margin gains stall, and the multiple resets toward the peer group.

Conclusion

The next real test is fiscal fourth-quarter earnings, due later this summer. Management guided revenue to $1.91 billion to $2.05 billion, so anything at or above the midpoint confirms the sequential acceleration the bull case depends on, and gross margin holding at or above 39% keeps the 42% target credible. A miss on either, or any softening in the order book, Anderson called a “step function increase,” would tell you the July selloff was early rather than wrong. Watch the backlog commentary as closely as the revenue line. That is where a demand-driven story cracks first, and right now it is the strongest part of the case.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Coherent?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Coherent, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Coherent alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Coherent on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!