Key Stats for Nucor Corporation Stock

- 6-Month Performance: 23%

- 52-Week Range: $98 to $197

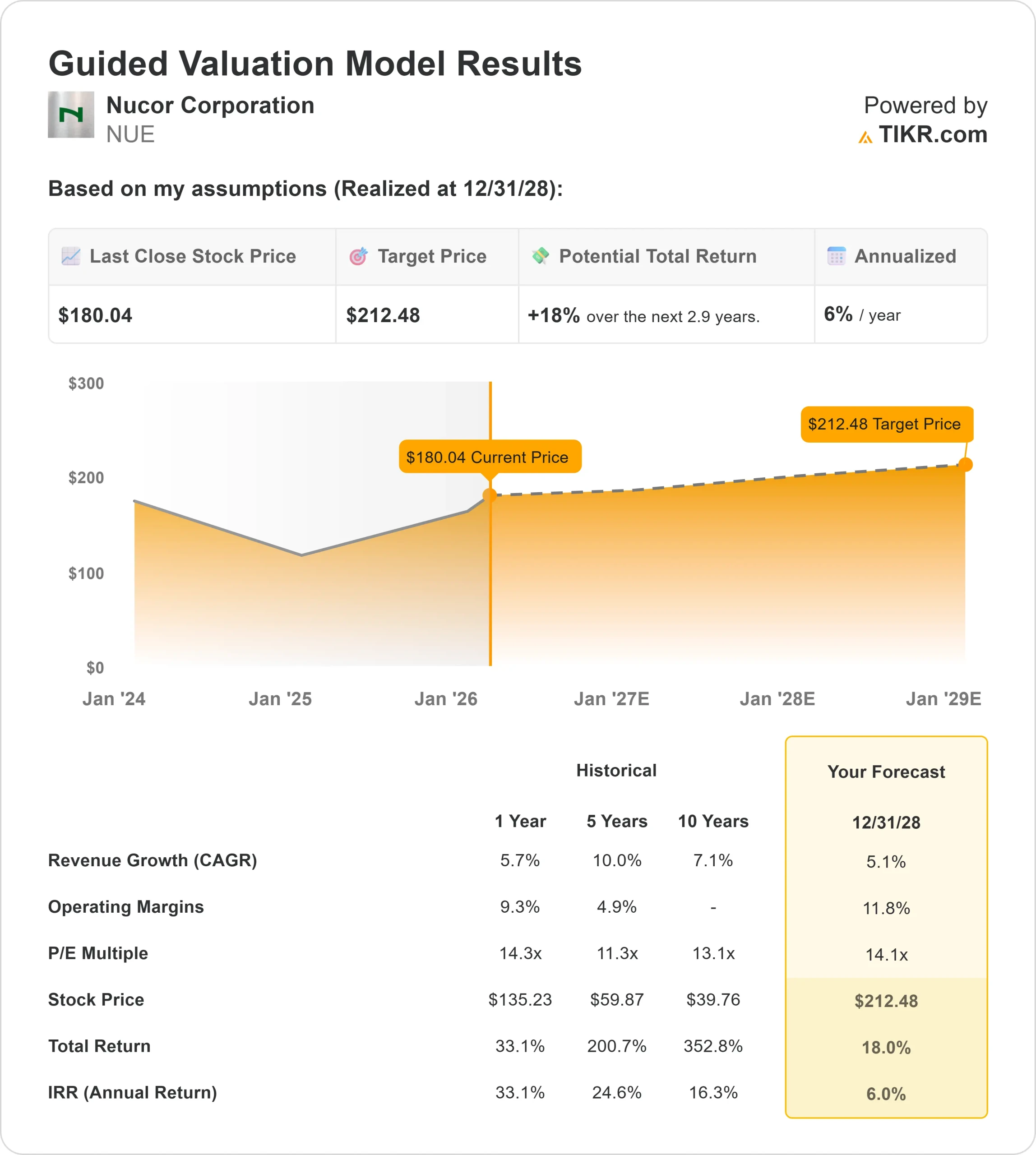

- Valuation Model Target Price: $212

- Implied Upside: 18%

Value your favorite stocks like Nucor Corporation with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Nucor Corporation stock shares finished near $180, up about 23% in the last 6 months, as investors priced in tightening steel imports, stronger backlogs, and improving forward visibility. The stock rebounded sharply from its $98 52-week low and recently approached its $197 high before consolidating.

The pullback reflects short-term earnings pressure, not weakening demand. Fourth quarter steel mills pretax earnings fell roughly 35% sequentially, and shipment volumes declined 8% due to seasonality and outages.

Sheet pricing lagged earlier in the quarter before turning higher in November and December, creating temporary margin compression.

Nucor reported adjusted earnings of $1.73 per share in Q4 and $7.71 per share for the full year, with EBITDA of $918 million for the quarter and about $4.2 billion in 2025.

Management expects steel mill shipments to rise roughly 5% in 2026, supported by backlogs that entered the year nearly 40% higher year over year in steel mills and 15% higher in steel products.

CEO Leon Topalian said the company begins 2026 “with real momentum,” citing infrastructure, energy, and data center strength.

Institutional activity reinforced confidence. Caprock Group initiated a 10,178-share position worth about $1.51 million, ABC Arbitrage SA purchased 27,975 shares valued near $3.79 million, and Diamond Hill Capital increased its stake to 1,685,250 shares worth $228.23 million.

Institutional ownership stands near 76.48%. Meanwhile, EVP Kenneth Rex Query sold 7,452 shares at $196.02, and EVP Allen Behr sold roughly 7,500 shares in early February, contributing to short-term consolidation after the rally.

See analysts’ growth forecasts and price targets for Nucor Corporation (It’s free) >>>

Is Nucor Corporation Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 5.1%

- Operating Margins: 11.8%

- Exit P/E Multiple: 14.1x

Revenue is projected to increase from about $32,494 million in 2025 to roughly $38,151 million by 2030, reflecting normalization after the steel downcycle rather than a return to the 2022 peak of $41,512 million.

Strength across infrastructure, energy infrastructure, data centers, and nonresidential construction provides structural demand support beyond short-term pricing swings.

Margin recovery remains the primary earnings lever in 2026. Recent EBIT margins sit near 8%, and a move toward mid-cycle levels closer to 12% would materially expand earnings as mill utilization improves and pricing stabilizes.

Management noted sheet prices began rising late in the fourth quarter, with most of that benefit expected to be realized in the first quarter of 2026.

Growth investments are beginning to contribute more meaningfully. Recently completed projects, including the Lexington micro mill, Kingman melt shop, new galvanizing lines, and downstream expansion, are expected to operate at positive EBITDA levels this year.

The company also expects approximately $500 million in incremental EBITDA contribution from recently completed projects and progress at Brandenburg compared to 2025.

Financial flexibility strengthens the setup. Nucor ended 2025 with $2.7 billion in cash, net debt to EBITDA near 1.07x, and a quarterly dividend recently raised to $0.56 per share, extending its 53-year record of annual increases.

With capital expenditures stepping down to roughly $2.5 billion in 2026, free cash flow is expected to improve as major projects transition from construction to earnings contribution.

Based on these inputs, the valuation model estimates a target price of $212, implying about 18% total upside, which places the stock firmly in the Undervalued category under a greater than 6% upside threshold.

At current levels near $180, Nucor appears undervalued heading into 2026, with performance likely driven by shipment growth, pricing stability, reduced import pressure, project ramp-ups, and disciplined capital allocation rather than reliance on another steel supercycle.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>