Key Stats for Intuitive Surgical Stock Stock

- This-Week Performance: 3%

- 52-Week Range: $425 to $608

- Current Price: $501

What Happened to Intuitive Surgical Stock?

Intuitive Surgical (ISRG) shares gained roughly 3% this week, extending their rebound following fourth quarter earnings and renewed investor focus on procedure growth heading into 2026.

The move followed better-than-expected Q4 results, with adjusted EPS of $2.53 on $2.87 billion in revenue and 18% global procedure growth across da Vinci and Ion platforms.

Intuitive Surgical placed 532 da Vinci systems during the quarter, accelerated adoption of the da Vinci 5 platform across hospitals, and expanded Ion procedures by 44%, reinforcing the strength of its high margin recurring instruments and accessories revenue base.

Although management guided 2026 da Vinci procedure growth to 13% to 15%, the market appears increasingly comfortable that cardiac clearance for da Vinci 5 and deeper penetration into ambulatory surgery centers can support durable double-digit expansion.

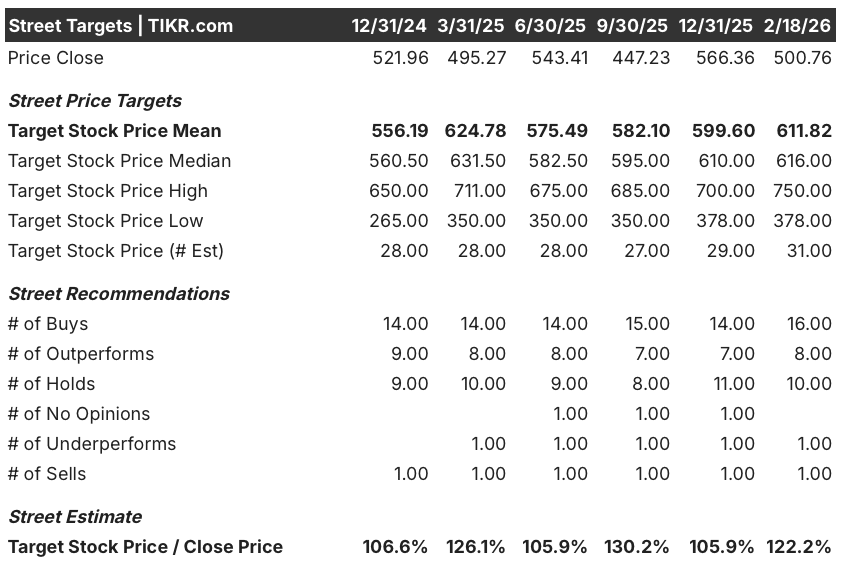

Leerink Partners maintained an Outperform rating with a $622 price target, while BTIG reiterated Buy at $616, signaling that many analysts view the company’s 2026 outlook as conservative despite tariff and China competition risks.

Where is the ISRG Stock Headed?

Intuitive Surgical’s recent 3% weekly gain reflects investors looking past cautious 2026 procedure guidance and instead focusing on expanding cardiac clearances, ambulatory surgery center penetration, and continued da Vinci 5 adoption as drivers of sustained double digit growth.

Fundamentally, revenue grew 21% in 2025 to $10.1 billion, normalized EPS is projected to rise from $8.93 in 2025 to $10.01 in 2026, and operating margins remain near 37%, supporting durable earnings compounding despite tariff pressure.

Wall Street’s mean price target now sits around $612 with 16 buy ratings and only one sell, implying roughly 22% upside from the current $500 level and signaling broad confidence in long term robotic surgery adoption.

Target dispersion is wide, with the low estimate near $378 and the high at $750, underscoring how views diverge on China competition, capital spending cycles, and whether procedure growth can reaccelerate above the 13% to 15% outlook.

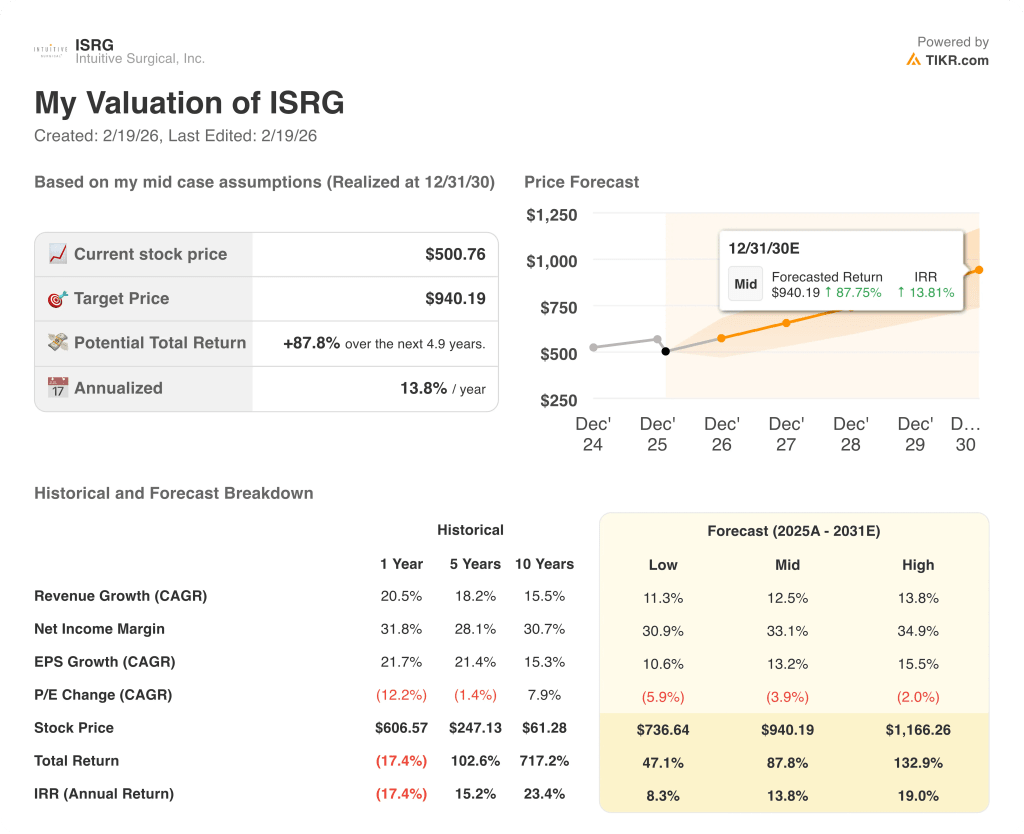

A mid case valuation model projecting a $940 price by 2030 implies nearly 88% total return and a 13.8% annualized IRR, assuming low teens revenue growth, stable margins above 30%, and modest multiple compression.

The primary risk remains multiple compression from the current premium valuation near 54 times forward earnings, especially if tariff impacts, slower Japan capital placements, or intensifying China competition weigh on margins.

Taken together, the stock appears modestly undervalued for long term investors willing to accept near term volatility, though its premium multiple leaves little room for operational missteps.

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.