Key Stats for Zoetis Stock

- Current Price: $117

- Target Price: $181

- Target Return: 47.8%

- Annualized IRR: 8.5%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Zoetis Inc. (ZTS) has been closely tied to the broader health of the pet consumer.

Investors have debated whether inflation, student loan resumptions for younger demographics, and rising veterinary costs would finally crack the secular boom in companion animal spending.

However, Zoetis continues to demonstrate unparalleled pricing power and portfolio resilience.

During the Leerink Global Healthcare Conference in March 2026, CFO Wetteny Joseph addressed these consumer concerns head-on.

He noted that while certain demographics like Millennials and Gen Z are feeling the pinch, the baseline commitment to pet health remains ironclad.

Joseph stated verbatim: “If you look at the latest data even through Q4 of 2025, overall vet clinic revenues were up about 6% in the quarter… ultimately, if the pet is sick and has an issue, they’re going to address it.”

This resilience is most evident in the company’s parasiticides portfolio.

Its triple-combination product, Trio, delivered over $1 billion in U.S. revenues last year alone.

Crucially, Zoetis is dramatically improving revenue visibility by shifting consumers to retail auto-ship channels.

While standard industry compliance for parasiticides is roughly 6 months, dogs placed on auto-ship are treated for 11 months out of the year, a massive organic volume driver that fundamentally changes the lifetime value of a patient.

See historical and forward estimates for Zoetis stock (It’s free!) >>>

Is Zoetis Undervalued Today?

The market is currently pricing Zoetis as if its core portfolios are fully saturated, completely underestimating the massive unpenetrated Total Addressable Market (TAM) in dermatology and osteoarthritis (OA) pain.

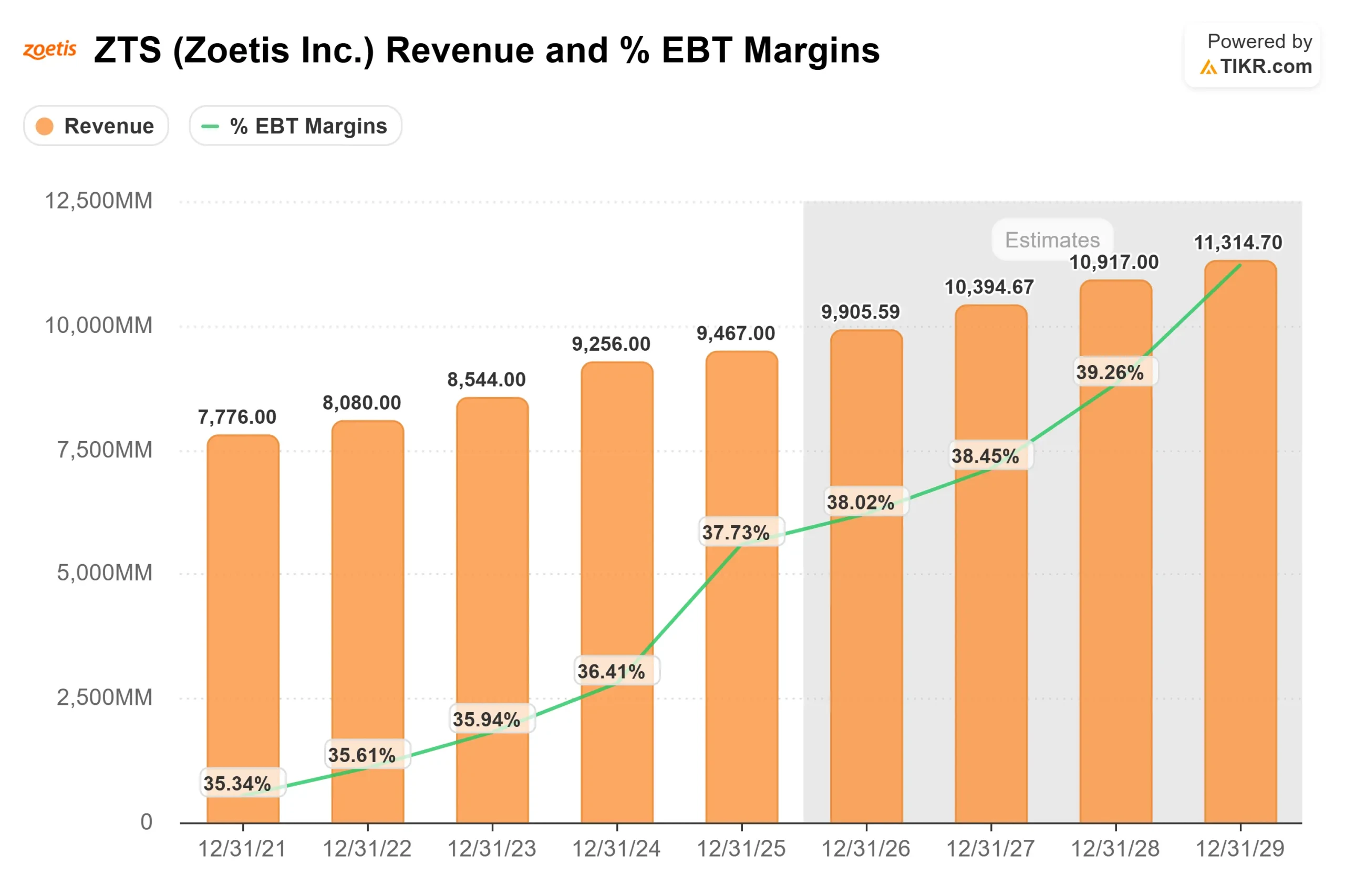

Last year, Zoetis generated $1.7 billion in key derm revenue.

Yet, according to management, fewer than 50% of itchy dogs see a veterinarian on a regular basis for treatment.

As clinical visits progressively recovered through the end of last year, foundational products like Apoquel and Cytopoint are primed to capture this massive, untreated population.

Similarly, the runway for OA pain management is immense. Management estimates there are 25 million to 27 million dogs suffering from OA pain in the U.S. alone.

Currently, only about 9 million receive any treatment, and just 1 million are on Zoetis’s Librela.

As the company expands its educational push regarding the progressive nature of joint pain, Librela is stabilizing into a massive long-term growth engine.

Beyond companion animals, Zoetis is also benefiting from an unexpected macroeconomic tailwind in its livestock business.

Driven by global urbanization and fascinating shifts in GLP-1 human consumption patterns that favor higher animal protein intake, the livestock segment is growing in the mid-single digits and providing exceptional cash flow diversification.

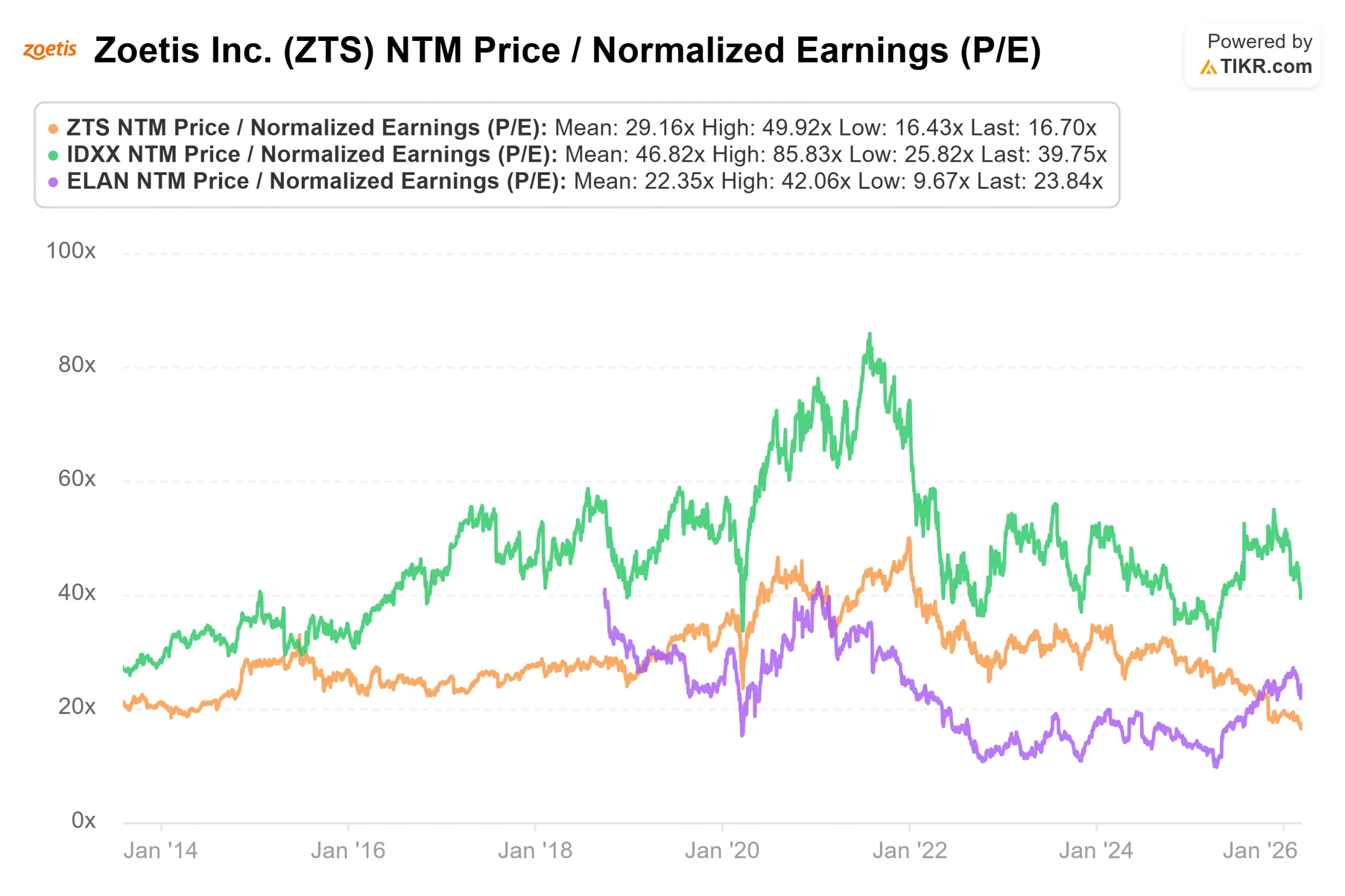

When benchmarked against animal health peers like IDEXX Laboratories (IDXX) and Elanco (ELAN), Zoetis clearly deserves a premium valuation.

See how Zoetis performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

The TIKR Advanced Model identifies Zoetis as a premier compounding asset. The company successfully leverages its massive scale to fund R&D innovation while relentlessly expanding the TAM of its core therapeutic categories.

- Current Price: $117

- Target Price: $181

- Target Return: 47.8%

- Annualized IRR: 8.5%

Build a 4-year Valuation Model for Zoetis for yourself (It’s free) >>>

The “Compliance” Margin Lever: The mechanical path to the $181 target relies heavily on Zoetis’s ability to drive sustained volume growth through better pet owner compliance. The model’s Mid Case assumes a highly resilient 4.5% Revenue CAGR over the forecast period. This steady top-line expansion is driven directly by the auto-ship adoption of Trio, the unpenetrated OA pain market for Librela, and mid-single-digit stability in the livestock segment.

By funneling massive volumes through highly efficient alternative channels and leveraging its established key derm dominance, Zoetis is forecast to achieve a pristine 31.1% Net Income Margin over the forecast period. This combination of relentless revenue compounding and expanding margins easily justifies the modeled 8.5% annualized return, making Zoetis an exceptionally strong long-term opportunity.

Conclusion: The market’s persistent focus on macroeconomic friction ignores the structural adherence occurring within Zoetis’s core categories. By actively shifting consumers to 11-month auto-ship compliance, penetrating the massive 25 million-dog OA pain market, and successfully executing strategic M&A like the Neogen genomics deal, Zoetis is future-proofing its dominance. The fundamental upside to a $181 valuation makes Zoetis a highly compelling, defensive growth opportunity.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Zoetis?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Zoetis, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Zoetis alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!