Key Stats for Digital Realty Stock

- This Week Performance: -0.9%

- 52-Week Range: $ to $

- Current Price: $

What Happened?

Digital Realty (DLR) colocation business — the segment that leases smaller, highly connected data center suites to enterprises rather than bulk capacity to cloud giants — posted record bookings in 2025, signaling a platform shift that pushed full-year Core FFO per share to $7.39, 10% above 2024 and above the high end of original guidance, with shares at $177.80 reflecting growing conviction that AI infrastructure demand has a longer runway than the market priced a year ago.

Digital Realty’s Q4 2025 earnings, reported February 5, delivered $1.63B in revenue against a $1.58B consensus estimate and Core FFO of $1.86 per share versus a $1.58 estimate, while management set 2026 Core FFO guidance of $7.90–$8.00 per share, implying roughly 8% bottom-line growth at the midpoint despite a known interest expense headwind from refinancing EUR 1.075B of 2.5% Eurobonds at approximately 4%.

The 0–1 MW plus interconnection segment — the colocation and connectivity business that serves enterprises deploying AI inference workloads rather than hyperscale training clusters — posted a Q4 quarterly record of $96M in bookings, capping a full year that ran 35% above 2024 levels and left a record backlog of $1.4B at 100% share, with $634M of leases already scheduled to commence in 2026.

Chief Financial Officer Matt Mercier stated at the Morgan Stanley Technology, Media and Telecom Conference on March 2 that “in 2025, we saw roughly 20% of those bookings within that category were driven by AI had some level of inference workload,” up from mid-single digits in 2024, directly linking the colocation segment’s record output to accelerating enterprise AI adoption.

A record $10B-plus gross development pipeline at an 11.9% expected stabilized yield, a 5 GW future capacity runway, $3.225B in LP equity commitments to Digital Realty’s inaugural hyperscale closed-end fund, and continued geographic expansion into Malaysia, Bulgaria, and Portugal position the company to compound Core FFO growth well into the decade as enterprise inference demand scales from 20% of colocation bookings today toward the majority share that cloud workloads now represent.

Wall Street’s Take on DLR Stock

The record $1.4B backlog — with $634M of leases already scheduled to commence in 2026 — converts Digital Realty’s leasing momentum directly into guided Core FFO growth of $7.90–$8.00 per share, making 2026 earnings unusually visible for a company of this scale.

Revenue is forecast to grow from $6.1B in 2025 to $6.7B in 2026 and $7.4B in 2027, driven by backlog commencements, 6%–8% cash renewal spreads, and a colocation segment growing 35% annually, with EBITDA margins holding near 54%–55% across the same period.

Meanwhile DLR’s normalized EPS — the per-share earnings figure stripped of one-time items — is estimated to jump 129.4% to $3.61 in 2026 as backlog commencements accelerate and fee income from the $3.2B closed-end hyperscale fund, a private investment vehicle Digital Realty launched to co-fund large data center builds, flows through the income statement.

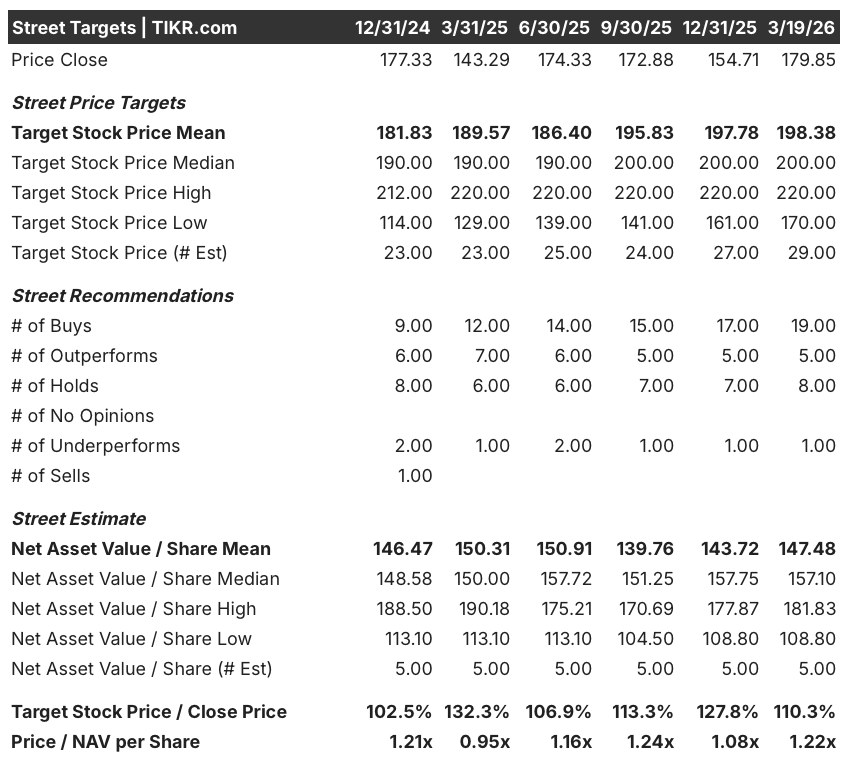

Wall Street has grown steadily more constructive: 24 analysts currently carry buy or outperform ratings against 8 holds and 1 underperform, with a mean price target of $198.38 implying roughly 10.3% upside from $179.85, anchored to the backlog visibility and the 8% guided FFO growth rate.

The $170 low target reflects the bear case that refinancing headwinds from the EUR 1.075B Eurobond rollover at roughly 4% versus the prior 2.5% coupon compress near-term FFO, while the $220 high target prices in faster-than-expected colocation bookings growth as enterprise AI inference — the use of deployed AI models to generate outputs in real time — scales beyond the current 20% share of segment bookings.

What Does the Valuation Model Say?

The TIKR mid-case model prices DLR at $268.48 by December 31, 2030, implying a 49.3% total return and 8.7% annualized IRR, supported by a 9.5% revenue CAGR assumption that the $634M of 2026 lease commencements and expanding Innovation Lab network across Singapore, Japan, and London are already beginning to validate.

The market prices DLR at 1.22x net asset value today, a premium that understates the earnings power embedded in a $10B-plus development pipeline yielding 11.9% on a stabilized basis.

AI-driven bookings in the 0–1 MW colocation segment rose from mid-single digits in 2024 to 20% in 2025, the operational confirmation that inference demand is compounding inside the segment the TIKR model relies on most.

CFO Matt Mercier confirmed on March 2 that inference adoption is “still in the early innings,” signaling that the 20% AI share of colocation bookings is a floor, not a ceiling, for the model’s growth assumptions.

The key assumption at risk is sustained 6%–8% cash renewal spreads; any softening in data center pricing, particularly in Northern Virginia where supply constraint is the primary driver, would directly compress same-capital NOI growth and erode the FFO trajectory.

Q1 2026 earnings will confirm whether the $634M of scheduled 2026 lease commencements are tracking on time and whether the 0–1 MW segment sustains its record quarterly run rate above $96M.

Should You Invest in Digital Realty Trust, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DLR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Digital Realty Trust, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DLR stock on TIKR for Free →