Key Stats for HP Stock

- This Week Performance: -3.4%

- 52-Week Range: $17.6 to $29.6

- Current Price: $18.5

What Happened?

Memory costs that once represented 15-18% of HP (HPQ) Inc.’s PC bill of materials now consume roughly 35%, forcing the personal computer and printer maker to guide fiscal 2026 earnings toward the low end of its $2.90-$3.20 range even as Q1 revenue beat consensus by $500 million, with the stock sitting at $18.21, near its 52-week low of $17.56.

HP’s Q1 results, reported February 24, delivered non-GAAP EPS of $0.81 against an IBES estimate of $0.77 and revenue of $14.44 billion against a $13.94 billion consensus, driven by Personal Systems, the company’s consumer and commercial PC division, which grew revenue 11% on 12% unit growth as the Windows 11 hardware refresh and AI PC adoption pulled forward demand.

AI PCs, laptops and desktops with on-device artificial intelligence processors that reduce reliance on cloud computing, represented 35% of Q1 shipments, up from 25% just two quarters earlier, and HP gained share in premium commercial and consumer categories in all three major regions even as rival Dell separately forecast its AI server revenue would double to $50 billion in fiscal 2027, underscoring how memory demand from AI infrastructure is simultaneously pressuring HP’s cost structure.

CFO Karen Parkhill stated on the Q1 2026 earnings call that “memory and storage costs made up roughly 15% to 18% of our PC bill of materials, and we now currently estimate this to be roughly 35% for the year,” a cost escalation HP is countering through long-term supply agreements, new supplier qualifications including evaluation of Chinese chipmaker CXMT for non-U.S. markets, targeted price increases, and an AI-enabled cost savings program targeting $1 billion in gross annualized run-rate savings by fiscal 2028.

HP’s return of $19 billion to shareholders over the last five years, a $2.8-$3.0 billion free cash flow target for fiscal 2026, and a print division posting 18.3% operating margins at the upper end of its long-term range provide financial ballast as the company searches for a permanent CEO to replace interim leader Bruce Broussard and positions AI PCs, now at 35% of shipments and rising each quarter, as the primary unit economics driver of a multi-year recovery toward its 5-7% Personal Systems margin target.

Wall Street’s Take on HPQ Stock

The memory cost shock that drove HP’s Personal Systems operating margin to 5.0% in Q1 and forced full-year EPS guidance toward the low end of $2.90-$3.20 is cyclical, not structural, and the market’s decision to reprice HPQ from 8x to 6x forward earnings in three months creates the entry point the TIKR model is built around.

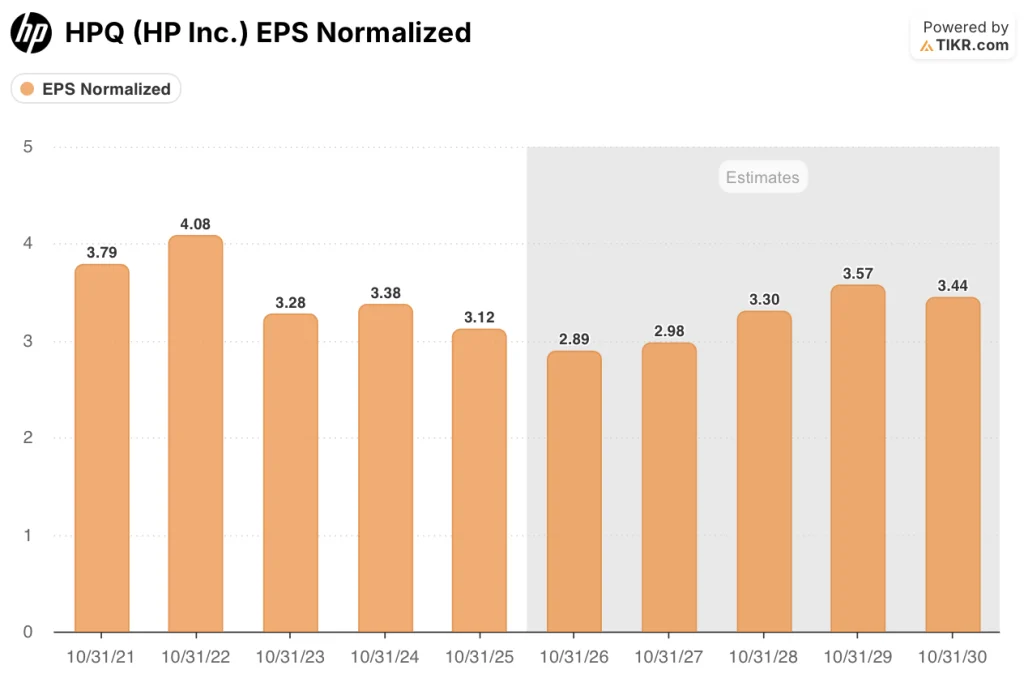

HP’s TIKR mid-case assumes only 1.7% revenue CAGR through October 31, 2030, a deliberately conservative input that requires no meaningful PC market recovery, yet normalized EPS still climbs from $2.89 in FY2026 to $3.30 in FY2028 and $3.57 in FY2029 as memory costs normalize and pricing actions taken in Q1 and Q2 fully flow through the income statement.

The 16 analysts covering HPQ as of March 19 reflect genuine division, with 3 buys, 1 outperform, 8 holds, 2 underperforms, and 3 sells producing a mean price target of $19.43, just 5.1% above the current price, suggesting the street is anchored to near-term memory headwinds rather than the 2027-2028 EPS recovery the TIKR model is pricing.

The spread between the street’s $16.00 low and $26.40 high targets is the widest it has been in over a year, with the bear case resting on memory costs persisting into FY2027 and further demand destruction in PC units, while the bull case requires only that HP’s pricing actions and $1 billion AI-enabled cost savings program, targeting $300 million in FY2026 alone, compress the cost gap faster than consensus expects.

What Does the Valuation Model Say?

The TIKR mid-case target of $29.19, implying a 58% total return and 10.4% annualized IRR by October 31, 2030, rests on a 3.0% annual P/E re-rating off today’s depressed 6x multiple, driven by EPS normalization as the memory-to-BOM ratio retreats from 35% and free cash flow recovers from $2.85 billion in FY2026 toward $3.12 billion in FY2028.

The market is treating a 35%-of-BOM memory cost spike as a permanent earnings impairment, but HP’s $2.85 billion FY2026 free cash flow estimate shows the cash engine remains intact even at peak memory pressure.

AI PCs at 35% of Q1 shipments and rising each quarter, combined with the print division sustaining 18.3% operating margins at the top of its 16-19% long-term range, confirm HP’s two-segment cash generation is structurally more resilient than the stock’s 6x multiple implies, supporting the TIKR $29.19 target.

Interim CEO Bruce Broussard’s February 24 confirmation that the board is considering CEO candidates outside the PC and print industry signals HP may be entering a strategic repositioning, not just a cyclical trough, which the current multiple does not price in at all.

If memory prices do not begin normalizing by the second half of FY2026 as HP’s supply agreements and new supplier qualifications assume, Personal Systems operating margins stay below the 5-7% long-term target range through FY2027, compressing the EPS recovery trajectory the TIKR $29.19 target requires.

The Q2 FY2026 earnings call, where HP will report whether the $0.70-$0.76 non-GAAP EPS guidance held and whether Personal Systems margins showed sequential stabilization, is the first hard data point confirming whether the memory mitigation playbook is tracking on schedule.

Should You Invest in HP Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HPQ stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track HP Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HPQ stock on TIKR for Free →