Key Stats for Yelp Stock

- This Week Performance: +5%

- 52-Week Range: $19.6 to $41.2

- Current Price: $22.3

What Happened?

Yelp stock (YELP) trades at $22.09, sitting just 13% above its 52-week low of $19.60 and well below its 52-week high of $41.2, underscoring how deeply the market has discounted a company that just delivered record full-year net revenue of $1.5B, record free cash flow of $323.7M, and a signed data licensing agreement with OpenAI.

Adding to the bearish pressure, JP Morgan cut its price target on February 17 to $22 from $30, reflecting Wall Street’s growing concern that RR&O advertising revenue, which fell 12% YoY in Q4, will continue dragging on overall growth even as Services advertising hit a record $948M for the full year.

Beneath the surface, the engine driving Yelp’s long-term thesis is its AI transformation, where Yelp Assistant drove a 400%-plus surge in Request-A-Quote submissions in 2025, the $270M acquisition of Hatch accelerated its lead management roadmap by roughly two years, and the OpenAI data licensing deal pushed other revenue up 33% YoY in Q4 alone.

Yet the market’s mental model of Yelp is beginning a slow but significant shift, moving from a legacy local advertising platform toward an AI-powered local discovery and SaaS business, with other revenue already carrying a better margin profile than the ad side and data licensing representing nearly pure margin contribution.

CEO Jeremy Stoppelman stated on the Q4 earnings call that “we believe we are well positioned to be the essential partner providing trusted local content and enabling actions whenever consumers are making local decisions,” contextualizing Yelp’s 330M reviews and nearly 500M photos as a proprietary data moat increasingly sought by AI platforms.

Supporting that pivot, the Board authorized an additional $500M in share repurchases in February, reinforcing institutional confidence in the stock at current levels, while the median Wall Street price target of $33 implies roughly 49.4% upside from the current price of $22.09.

Over the next 3 to 5 years, Yelp’s ability to monetize its first-party local content across AI ecosystems, combined with Hatch’s 70% YoY growth rate and a fully diluted share count already reduced 22% since 2021, positions the company to re-rate from a slow-growth ad business trading at 8x forward earnings toward a diversified AI data and SaaS platform commanding a meaningfully higher multiple.

Wall Street’s Take on YELP Stock

Yelp’s $270M acquisition of Hatch and its freshly signed OpenAI data licensing deal directly accelerate the company’s shift toward higher-margin SaaS and licensing revenue, strengthening the forward earnings picture precisely as advertising headwinds pressure near-term guidance.

Beneath the surface, however, the fundamentals tell a story of compression: FY2026 estimates project revenue growth decelerating to just 0.4% with EBITDA margins contracting to 22.0% from 25.2%, while normalized EPS slips 2.8% to $3.61, signaling the business is stabilizing rather than accelerating.

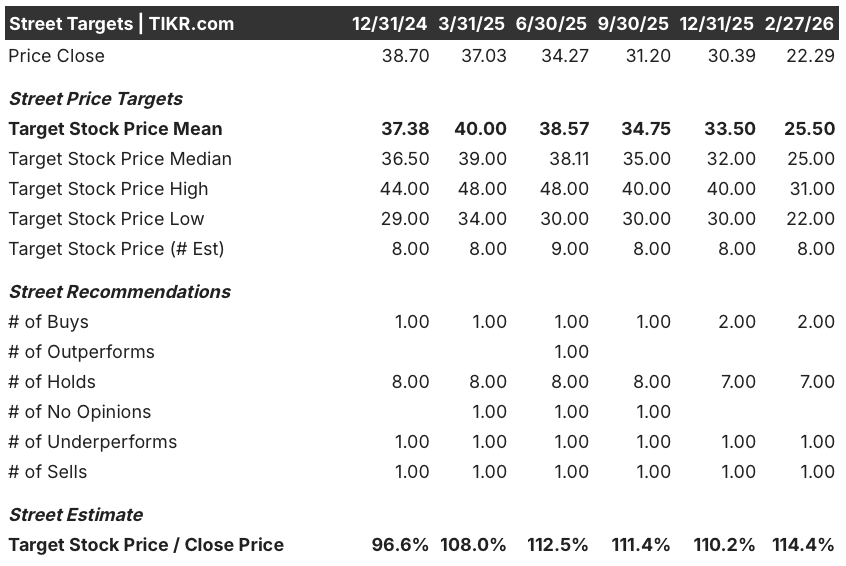

Currently, Wall Street carries 2 buys, 7 holds, 1 underperform, and 1 sell on YELP, with a mean price target of $25.50 that implies 15.4% upside from $22.09, suggesting analysts are holding conviction despite the pullback rather than upgrading into the AI transformation story.

The spread between the low analyst target of $22.00 and the high of $31.00 is significant, with the low anchored by continued RR&O deterioration and EBITDA margin compression, while the high depends on Hatch’s 70% growth rate sustaining and Yelp Assistant driving measurable Services revenue re-acceleration.

What Does the Valuation Model Say?

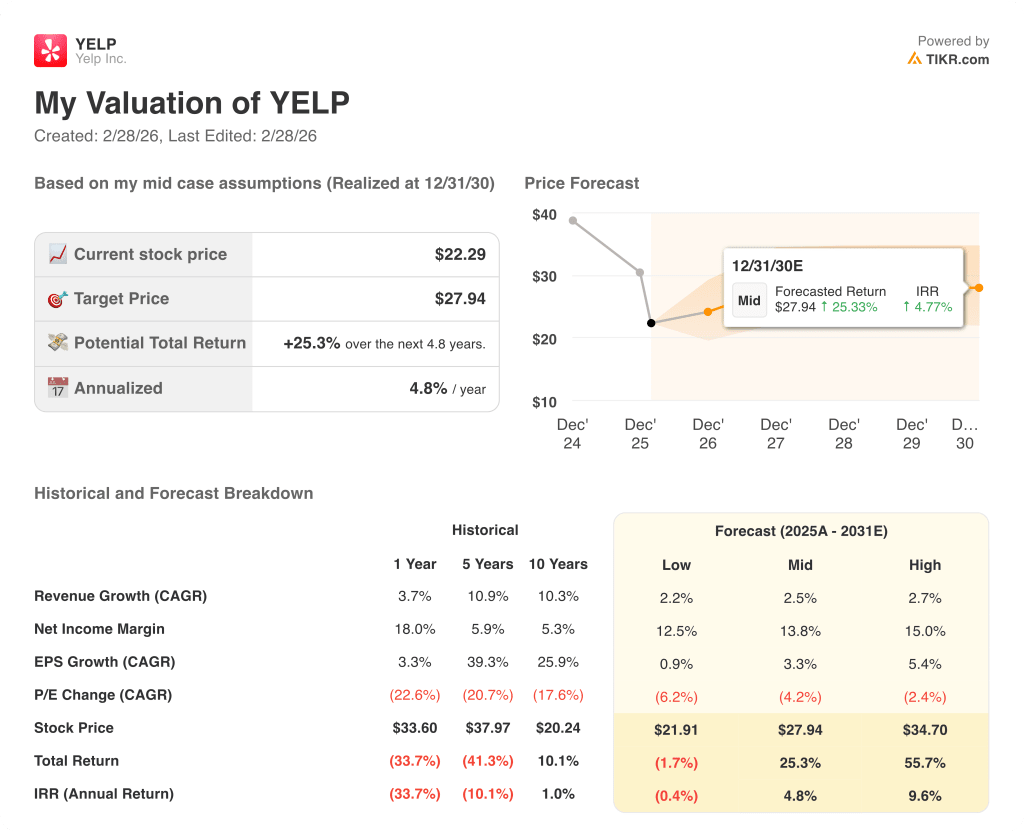

Given Yelp’s record $323.7M free cash flow, its $500M buyback authorization, and a growing data licensing business now up 30%+ in Q4, a mid-case valuation model prices YELP at $27.94, implying a 25.3% total return over 4.8 years at a 4.8% annualized IRR.

At just 8x forward earnings and trading 46.3% below its 52-week high of $41.2, YELP appears mispriced relative to its AI data monetization runway, with the OpenAI agreement and Hatch integration providing credible re-rating potential that analysts with a $25.50 mean target have yet to fully reflect.

The most consequential risk remains EBITDA margin compression, with FY2026 estimates projecting a 12.5% YoY EBITDA decline to $320M as Hatch operating costs, paid traffic acquisition spending, and AI investment collectively pressure profitability before the new revenue streams scale meaningfully.

The single most important inflection point to watch is the full rollout of cross-category Yelp Assistant expected by end of Q1, where a measurable uptick in Request-A-Quote volumes and Services revenue growth will determine whether the AI transformation thesis converts from narrative to numbers.

Altogether, YELP looks modestly undervalued at $22.09 for patient investors with a 3 to 5 year horizon, but the near-term setup demands Yelp Assistant’s Q1 launch delivers tangible engagement gains and Hatch sustains its 70% growth trajectory to justify re-rating above the $25.50 consensus target.

Should You Invest in Yelp, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up YELP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Yelp, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze YELP stock on TIKR for Free →