Key Stats for Hasbro Stock

- This Week Performance: -1%

- 52-Week Range: $49 to $107

- Current Price: $100.4

What Happened?

Hasbro’s Wizards of the Coast division has quietly become the most powerful engine in the toy industry, generating $2.2 billion in revenue with a 44.7% surge that single-handedly kept the company afloat while shares trade near their 52-week high of $106.98, currently at $100.36.

The Supreme Court’s February 20 ruling against Trump’s IEEPA tariffs served as the immediate trigger, sending Hasbro shares up as much as 2.3% on the day as investors priced in the possibility of substantial refunds on the roughly $44.9 million in tariff costs the company absorbed in cost of sales during FY2025.

Beneath the tariff relief, the real engine driving Hasbro’s momentum is Magic: The Gathering’s record-breaking Universes Beyond partnership strategy, which pulled in landmark collaborations spanning Final Fantasy, Avatar: The Last Airbender, and Marvel’s Spider-Man while Monopoly Go! added another $168.0 million to the digital gaming ledger.

Consequently, the market is actively shedding its view of Hasbro as a struggling legacy toymaker and repricing it as a digital-and-IP platform business, evidenced by the $1.0 billion operating profit from Wizards of the Coast towering over the Consumer Products segment’s $942.6 million operating loss.

Beyond the segment reshaping, CEO Christian P. Cocks stated on the Q4 earnings call that the Wizards division delivered record performance, contextualizing a broader strategic pivot where trading card games and digital licensing are now Hasbro’s clearest path to sustained profitability.

Furthermore, Hasbro strengthened its financial foundation on February 20 by securing a $1.1 billion revolving credit facility through Bank of America, extendable by an additional $550 million and maturing in 2031, signaling lender confidence in the company’s long-term cash generation despite a net loss of $322.4 million for the full year.

Looking ahead, Hasbro’s aggressive licensing expansion announced at the February 14 Toy Fair, including multi-year deals with Warner Bros. Discovery for Harry Potter, Netflix for KPop Demon Hunters, and Amazon MGM Studios for Voltron, positions the company to compound its IP-driven revenue model across an entirely new generation of entertainment franchises over the next three to five years.

Wall Street’s Take on HAS Stock

The Supreme Court’s February 20 tariff ruling directly removes the overhang that forced Hasbro to absorb $44.9 million in tariff costs and triggered a $1.0 billion goodwill impairment, meaningfully improving the forward earnings picture as potential refunds could flow back to the bottom line.

Analysts now expect revenue to reach $4.9 billion in FY2026 with 4.0% growth, while normalized net income climbs from $780 million to $800 million, and EBITDA margins hold firm at 29.1%, confirming that the business is stabilizing around a leaner, higher-margin structure anchored by Wizards of the Coast.

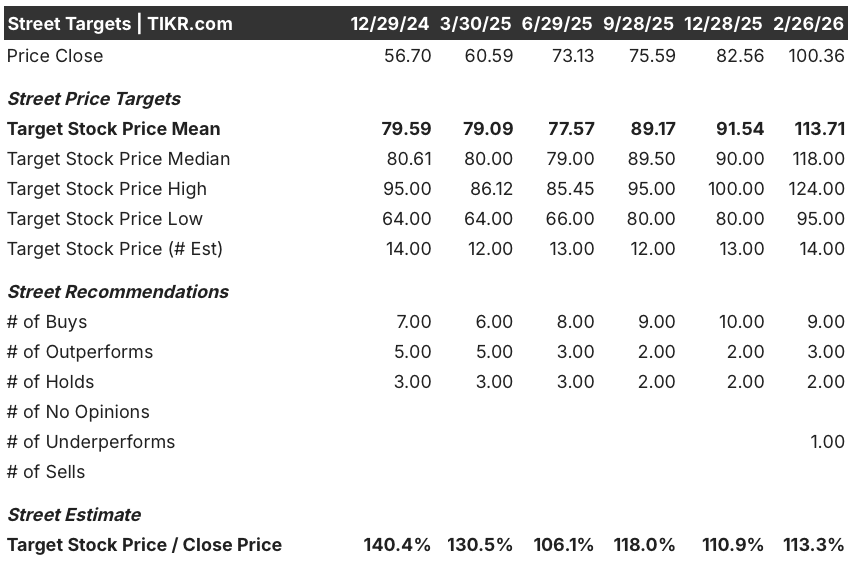

Wall Street currently fields 9 buys, 3 outperforms, 2 holds, and 1 underperform, with a mean price target of $113.7, implying roughly 13.3% upside from the current price of $100.36, reflecting analysts upgrading into strength on the back of Hasbro’s digital gaming pivot rather than despite a pullback.

The spread between the analyst low target of $95.0 and the high of $124.0 signals that the stock’s path hinges entirely on whether Magic: The Gathering’s Universes Beyond momentum sustains through FY2026 or whether Consumer Products continues bleeding, with EPS normalized growth of just 2.0% in FY2026 serving as the key inflection metric to watch.

What Does the Valuation Model Say?

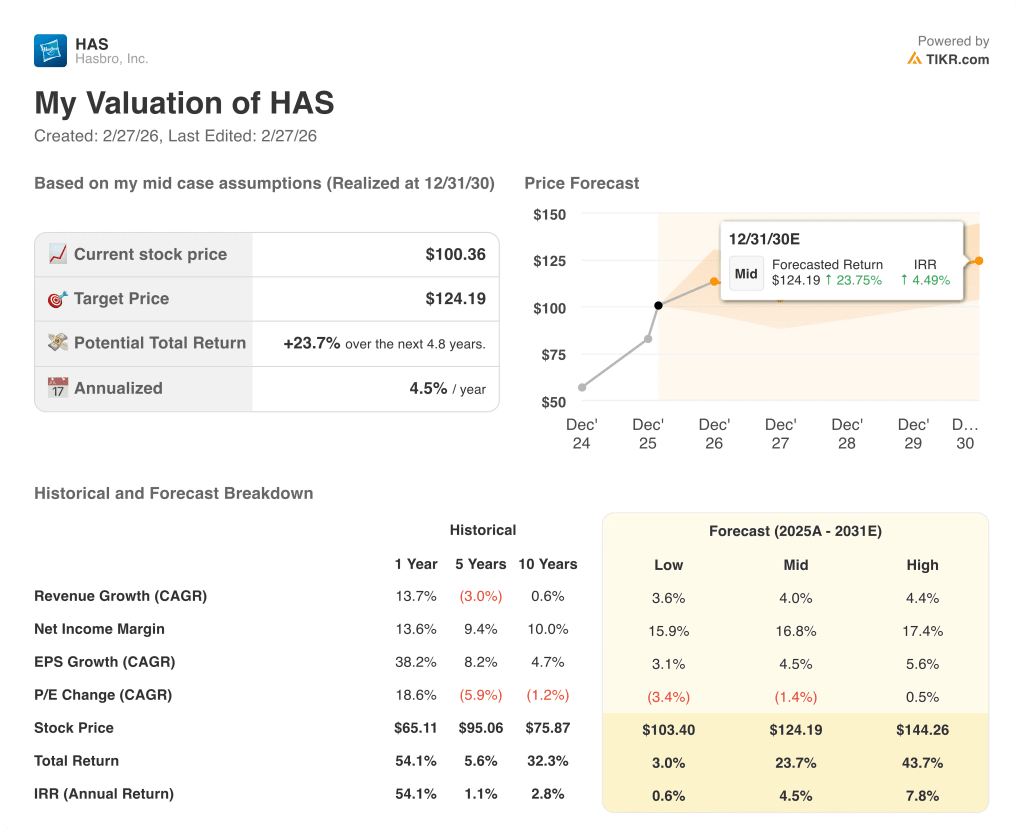

Given the Supreme Court relief and the Wizards segment’s structural dominance, TIKR’s mid-case valuation model prices Hasbro at $124.2 with a total return of 23.7% over 4.8 years and an annualized IRR of 4.5%, a modest but credible return profile for a business actively repricing from toy manufacturer to IP platform.

The most consequential bear risk remains P/E multiple compression, already visible in the model’s mid-case P/E CAGR of -1.4% through 2031, meaning Hasbro must grow earnings fast enough to offset a contracting valuation multiple or the stock stalls near current levels despite improving fundamentals.

Hasbro looks fairly valued at $100.36 with a modest tilt toward upside, but the real verdict arrives when FY2026 Magic: The Gathering partnership revenues confirm whether the Universes Beyond strategy can sustain 44.7% Wizards growth or begins to normalize toward the more conservative 4.0% revenue CAGR the model assumes.

Should You Invest in Hasbro, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up HAS stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Hasbro, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze HAS stock on TIKR for Free →