Key Takeaways for SPX Technologies Stock

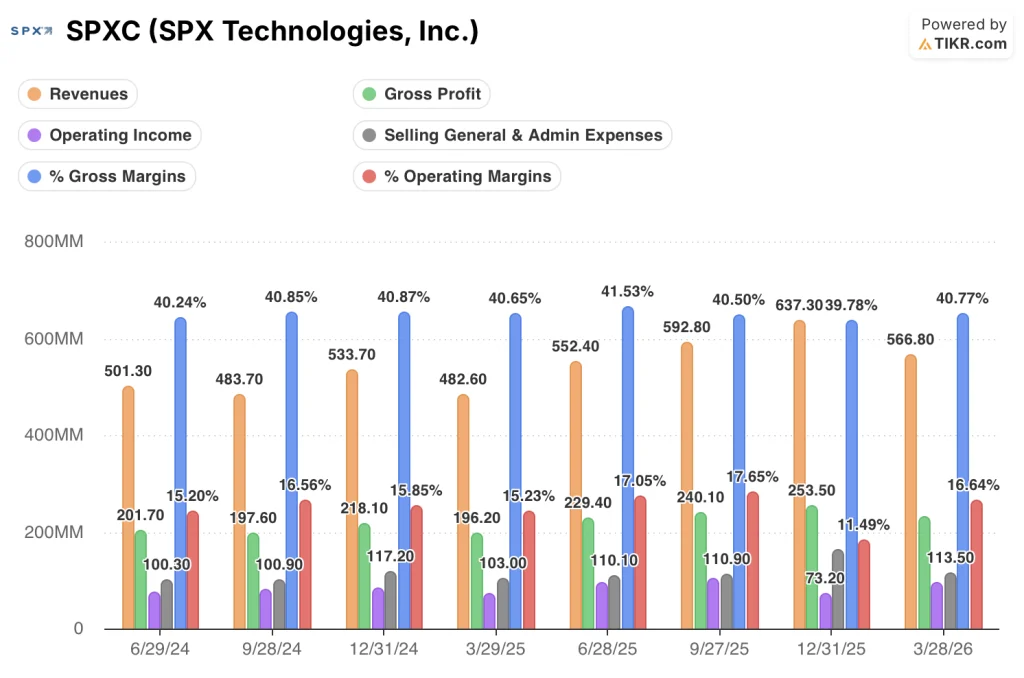

- Revenue grew 17% year-over-year to $566.8 million in Q1 2026, beating the $557.6 million street estimate.

- Operating income reached $94.3 million in Q1 2026, with operating margins expanding to 17% from 15% a year earlier.

- HVAC segment backlog grew 38% organically to $755 million, driven by data center cooling demand.

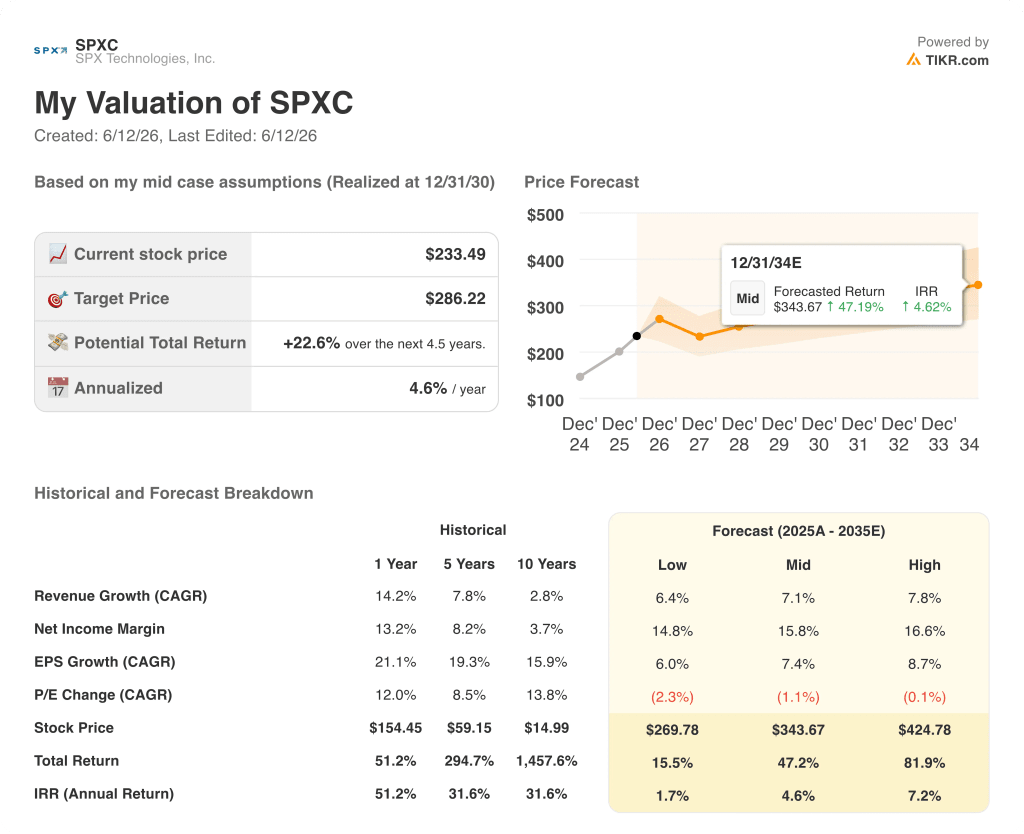

- TIKR’s mid-case values SPXC stock at approximately $344 by December 2034, implying around 47% total return from the current price of $233.

SPX Technologies Stock Beat Q1 Estimates and Raised Guidance as Data Center Demand Accelerated to 70% Growth

SPX Technologies (SPXC), a Charlotte-based supplier of engineered cooling towers, custom air handlers, and detection systems, reported Q1 2026 results on April 30 that beat estimates on every major metric and prompted a full-year guidance raise.

Revenue of $566.8 million grew 17% year-over-year, led by 22% growth in the HVAC segment and 8% growth in Detection and Measurement (D&M), the division that supplies underground pipe locators, robotic inspection systems, drone detection technology, and transportation platforms.

Adjusted EPS of $1.69 beat the $1.56 street estimate by $0.13 and grew 22% year-over-year, while adjusted EBITDA grew 23% with 90 basis points of margin expansion.

The single most consequential development from the call was the acceleration of data center cooling revenue guidance from 50% growth to 70% growth for 2026, implying approximately $350 million in data center revenue this year against a $200 million base in 2025.

CEO Gene Lowe explained the mechanism on the Q1 earnings call: “The demand is extremely strong. At our last quarterly update, we guided that to $350 million. We’re really focusing on expanding our capacity, and we’re making great progress there.”

The capacity program underpinning that guidance is three facilities in Olathe, Kansas; Nashville, Tennessee; and Madison, Alabama, which together with existing infrastructure give SPX Technologies the ability to serve approximately $750 million of data center revenue at full build-out.

HVAC backlog ended Q1 at $755 million, up 38% organically, a figure that directly captures how far forward demand visibility extends beyond the current quarter.

The D&M segment delivered its own surprise: a scope expansion on an existing transportation project pushed high-margin software revenue into Q1, driving segment margin expansion of 410 basis points and prompting management to raise full-year D&M margin guidance by 75 basis points.

Management raised full-year adjusted EPS guidance to a midpoint of $7.95, up $0.15 from prior guidance, and full-year revenue guidance to a $2.575 to $2.645 billion range, despite absorbing a $0.05 to $0.10 tariff headwind expected predominantly in Q2.

SPXC Stock’s Operating Leverage Is Widening, but Start-Up Costs Are Temporarily Obscuring the Signal

SPX Technologies stock’s revenue compounded from $482.6 million in Q1 2025 to $566.8 million in Q1 2026, a 17% year-over-year gain that reflects both acquisition contribution and 7% organic growth across both segments.

Gross profit grew 18% year-over-year to $231.1 million in Q1 2026, with gross margins holding at 41%, a figure that has remained in a tight band between 40% and 41% across the past eight quarters on the income statement.

The more revealing dynamic sits one level lower: operating income grew 28% year-over-year to $94.3 million in Q1 2026, outpacing revenue growth by 11 percentage points and confirming that fixed cost leverage is working.

Operating margins reached 17% in Q1 2026, up from 15% in Q1 2025, continuing a trajectory that saw operating margins move from 15% to 18% across the six quarters ending September 2025 before a Q4 2025 dip to 12% driven by elevated SG&A of $161.8 million, which appears to have normalized to $113.5 million in Q1 2026.

The start-up costs associated with the three-facility expansion are currently running through HVAC segment margins, which declined 40 basis points year-over-year in Q1 2026, and CFO Mark Carano sized the full-year burden at approximately $8 to $9 million, with two-thirds landing in the first half.

Stripping those costs out, Carano described 60 to 70 basis points of organic operating leverage in the HVAC segment, with an additional 10 to 20 basis points of accretion from recent acquisitions.

SPXC Stock Runs a Structural Operating Margin Lead Over Rexnord and Watts Water That Has Only Widened

SPX Technologies stock’s operating margin of 17% in Q1 2026 sat 6 percentage points above Rexnord (RRX) at 11% and 10 percentage points above Watts Water Technologies (WATTS) at 6% for the same period, a gap that has been consistent across every quarter in the data.

The lead is not cyclical. Across eight consecutive quarters from June 2024 through March 2026, SPXC stock’s operating margins ranged from 15% to 18%, while RRX ranged from 11% to 13% and WATTS ranged from 4% to 7%, a structural separation that points to a fundamentally different cost architecture rather than a favorable quarter.

What drives the gap is the engineered-to-order model. Because virtually every product SPX Technologies ships is configured or custom-built against a specific order, the company prices in real-time cost data rather than absorbing commodity swings against fixed-price inventory, an advantage that flows directly into the operating margin line and compounds as revenue scales.

The implication for SPXC stock’s valuation is direct. A business running 17% operating margins against peers at 11% and 6% on the same metric, with a margin trajectory that shows those gaps widening rather than closing, earns a premium multiple. The question the TIKR model answers is whether the current price of $233 reflects that premium appropriately, or whether the capacity expansion timeline and the data center revenue ramp represent upside the market has not yet priced in.

Is SPXC Stock Undervalued in 2026? TIKR’s $344 Mid-Case Suggests the Market Is Not Pricing the Full Capacity Ramp

TIKR’s mid-case values SPXC stock at approximately $286 by December 2030, implying around 23% total return from the current price of $233, or roughly 5% annualized over 4.5 years.

Under a high-case scenario, where revenue grows at a 8% CAGR and net income margins expand toward 17%, the TIKR model produces a stock price of approximately $425 by December 2034, implying around 82% total return or roughly 7% annualized.

The condition that drives the outcome is full utilization of the Madison, Alabama facility and continued data center demand growth into 2027 and 2028, which Lowe described as having “some attractive runway.”

Under a low-case scenario, where revenue grows at 6% and margins compress toward 15%, the TIKR model produces approximately $270 by December 2034, implying around 16% total return or roughly 2% annualized. The risk is elevated start-up costs persisting beyond management’s expected timeline and tariff headwinds that exceed the $0.05 to $0.10 guided range.

The mid-case requires roughly 7% revenue growth and net income margins near 16%, assumptions that appear conservative relative to a business currently growing revenue 17% and posting 22% adjusted EPS growth in the most recent quarter.

Is SPXC Stock a Buy Right Now?

SPXC stock beat Q1 2026 estimates on revenue, EBITDA, and EPS, then raised full-year guidance to a $7.95 midpoint for adjusted EPS.

The TIKR mid-case implies around 47% total return to December 2034.

The near-term question is whether start-up costs in HVAC normalize in the second half as management expects, since removing those costs reveals 60 to 70 basis points of organic operating leverage already in the business.

What Is the Outlook for SPXC Stock’s Data Center Business?

Management guided data center revenue to approximately $350 million in 2026, up 70% year-over-year from $200 million in 2025.

Three-facility capacity expansions in Kansas, Tennessee, and Alabama are designed to support approximately $750 million of total data center revenue at full build-out.

CEO Gene Lowe described demand as “accelerating” and noted visibility extending into 2027 and 2028.

Should You Invest in SPX Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SPX Technologies, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SPX Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SPXC stock on TIKR for Free →