Key Takeaways:

- The 2-Minute Valuation Model values Solaris Energy stock at $46 per share in 2 years.

- That’s a potential 64% upside from today’s price of $28 per share.

- Solaris Energy stock is projected to grow EPS by almost 700% over the next 3 years as Power Solutions scales dramatically.

- The energy stock is trading at reasonable multiples despite securing major AI data center contracts with extended tenors.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Solaris Energy (SEI) is a leading provider of mobile power generation and logistics solutions, uniquely positioned at the intersection of two high-growth markets: AI data center power demand and energy logistics services.

Through its Power Solutions and Logistics Solutions segments, Solaris has transformed from a traditional oilfield services company into a critical infrastructure provider for the artificial intelligence revolution.

With the energy stock now trading at $28 per share, Solaris presents a compelling opportunity for investors seeking exposure to the AI infrastructure buildout and energy transition at an attractive valuation with strong earnings visibility.

Let’s examine why this energy infrastructure leader could deliver substantial returns as AI power demand accelerates and the company scales its contracted capacity.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings-per-share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why the Energy Stock Looks Undervalued

Forecast

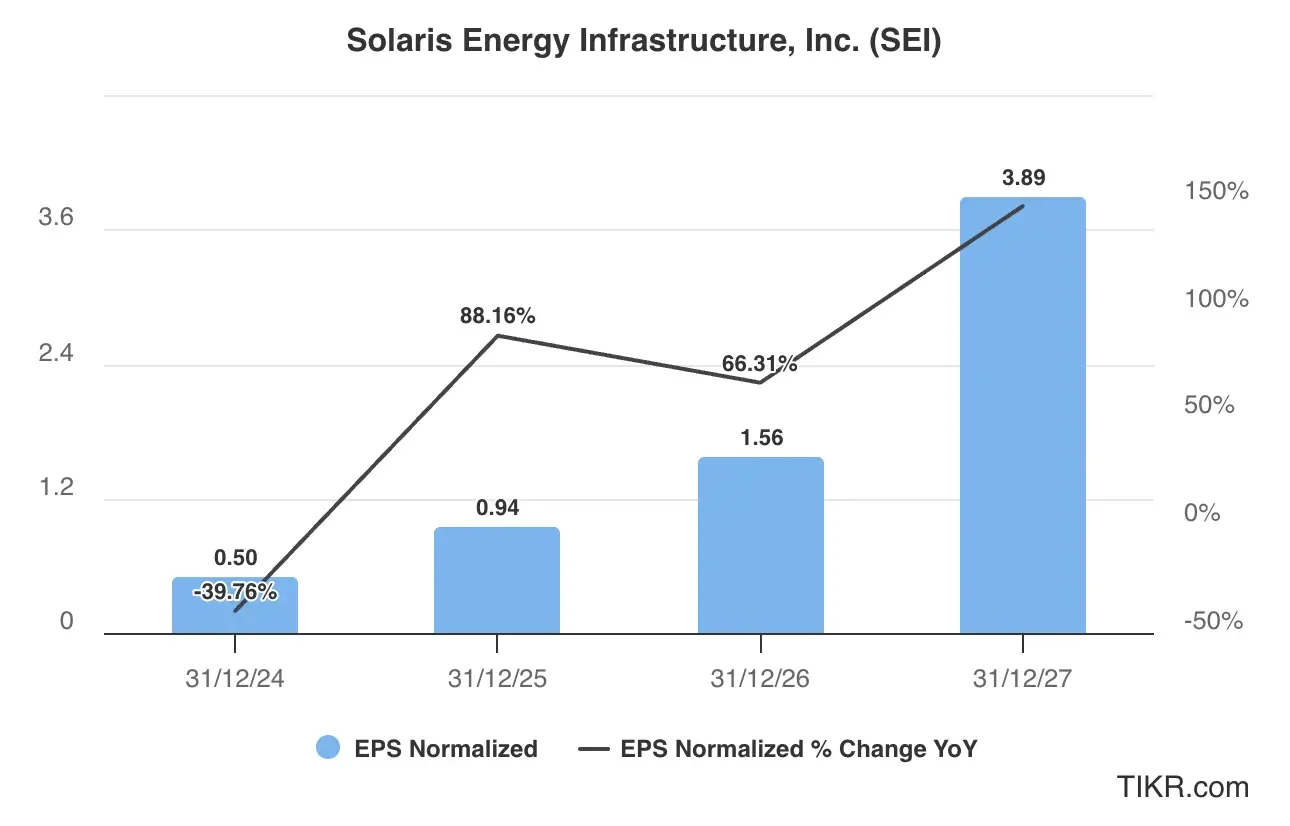

Based on analyst estimates, Solaris Energy is expected to experience explosive earnings growth over the next three years as it scales its Power Solutions business to meet the demand for AI data centers.

EPS is projected to surge from $0.50 in 2024 to $3.89 by 2027, representing a 678% increase in total. The growth trajectory shows dramatic acceleration, with EPS in 2025 expected to expand by 88%, followed by 66% EPS growth in 2026, and an explosive 149% growth in 2027.

This earnings growth for the energy stock is likely to be driven by:

- AI data center mega-contracts: A recently upsized joint venture with a major AI customer to 900 megawatts over seven years provides massive earnings visibility.

- Power-as-a-Service scaling: Fleet expansion to 1,700 megawatts total capacity (1,250 net to Solaris) with 70% contracted.

- Extended contract tenures: The average contract length increased from six months to over five years, providing unprecedented earnings stability.

- Operating leverage: As power generation scales, fixed costs spread across a larger capacity base drive margin expansion.

For our valuation, we’ll estimate that SEI stock will reach $3 in EPS in 2027.

Check out Solaris Energy’s full analyst estimates (It’s free) >>>

Is Solaris Energy Stock Undervalued Right Now?

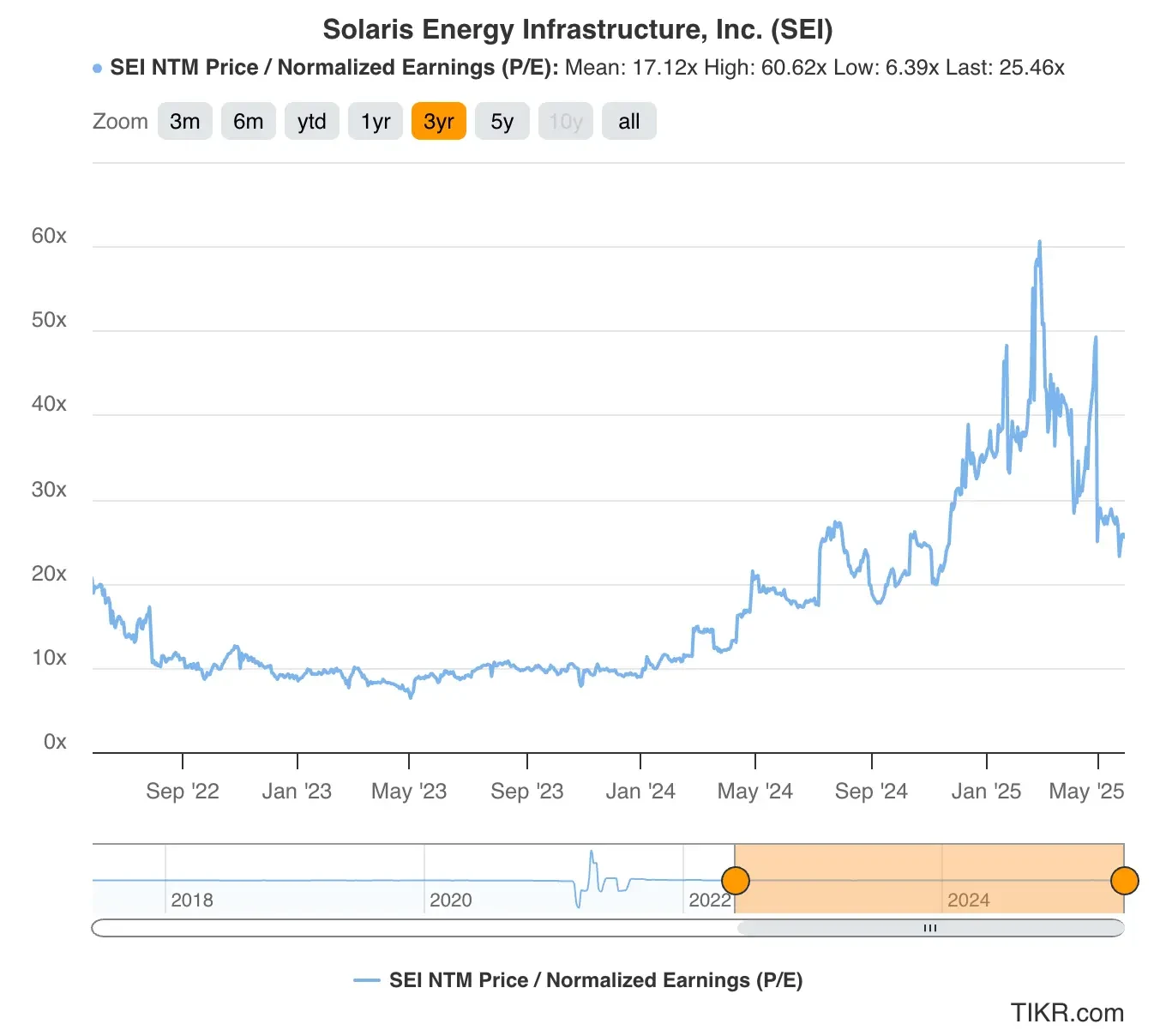

Solaris Energy stock trades at around 25x forward earnings, which is above its 3-year historical average P/E of 17x, as shown in the valuation chart.

Given the dramatic business transformation and contracted growth ahead, it seems like the stock could be undervalued today.

For our valuation, we’ll use a forward P/E multiple of 15x, which reflects a more normalized multiple for a scaled infrastructure business and accounts for the transition from a high-growth company to a business with steady-state operations.

Fair Value of Solaris Energy Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $3

- Conservative forward P/E multiple: 15x

- Expected dividends over the next 2 years: $1

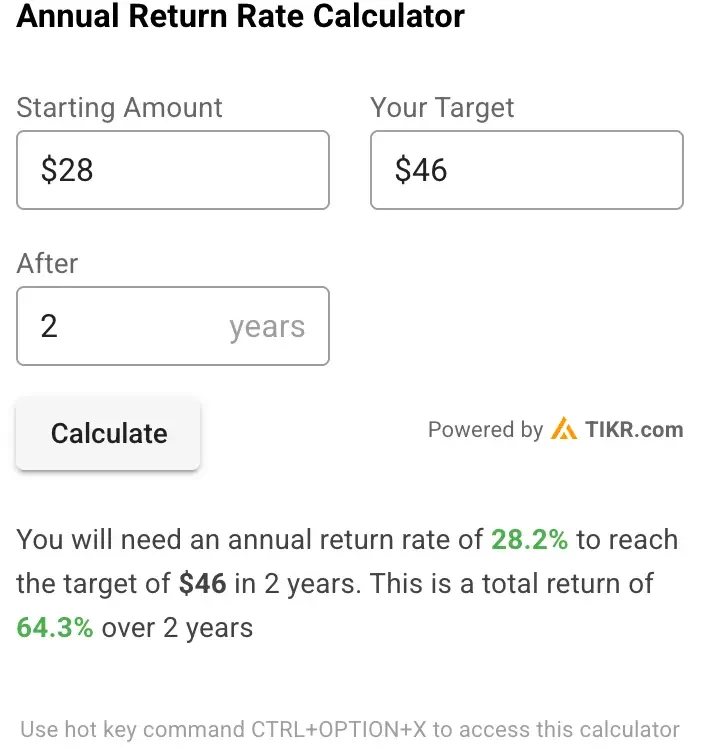

Expected Normalized EPS ($3) * Forward P/E ratio (15x) + Expected Dividends ($1) = Expected Share Price ($46)

The 2-year expected Solaris Energy stock price we would get from this valuation is $46 per share.

Solaris Energy stock is currently trading at around $28 per share, which implies a potential upside of 64% over the next two years or a 28% annualized return.

Solaris Energy stock is well-positioned to deliver outsized gains to shareholders, given that the broader markets’ average annual returns have been around 10%.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is the Average Analyst Price Target for SEI Stock?

Analysts think Solaris Energy could have some serious upside.

Their average price target is around $44 a share, which is about 57% higher than where the stock is trading today. It shows they’re confident in the company’s growing market share and its path to turning a profit.

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact Solaris Energy’s growth trajectory:

- Customer concentration: A heavy reliance on a single AI customer creates a concentration risk, despite strong contract terms.

- OEM supply constraints: A tight turbine supply chain could limit growth if additional capacity needs emerge.

- Commodity price sensitivity: The Logistics segment is exposed to oil price volatility and competition activity levels.

- Execution risk: Scaling from current capacity to 1,700 megawatts requires flawless project management.

TIKR Takeaway

Solaris Energy presents a unique opportunity to invest in the AI infrastructure buildout through a proven energy services provider with contracted growth visibility.

The energy stock’s significant upside potential is driven by its transformation from a cyclical oilfield services company to a contracted power infrastructure provider, with multi-year earnings visibility and massive scalability ahead.

While SEI faces execution risks typical of rapidly scaling infrastructure businesses, its early mover advantage in Power-as-a-Service, strong customer relationships, and secured capacity in a tight supply market position it uniquely for the AI power demand surge.

The contracted nature of the business model provides downside protection while the scaling opportunity offers substantial upside. Investors seeking exposure to AI infrastructure with downside protection should find Solaris compelling.

Is Solaris Energy stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!