Coles (COL) sits at the center of Australia’s supermarket industry, serving millions of households each week through its national store network, online channels, and private-label portfolio. The past year has been a reset period, marked by cost pressures, shifting consumer behavior, and operational challenges tied to inflation and supply chain volatility. Even with these headwinds, Coles maintained steady customer traffic and saw stable demand across core grocery categories.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The company continues to lean into digital adoption, operational simplification, and everyday-value positioning to support long-term competitiveness. That strategy helped Coles manage a complex FY25 environment in which volume held up, but margins required tighter discipline. Investors have taken notice: shares have climbed steadily since early 2025 as the earnings base stabilized.

As the company enters FY26, the setup looks cleaner. Cost visibility is improving, digital penetration is rising, and execution across fresh foods and private label remains solid. The next phase of growth depends on whether Coles can drive consistent operating leverage while keeping value-oriented customers engaged during a softer consumer cycle.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

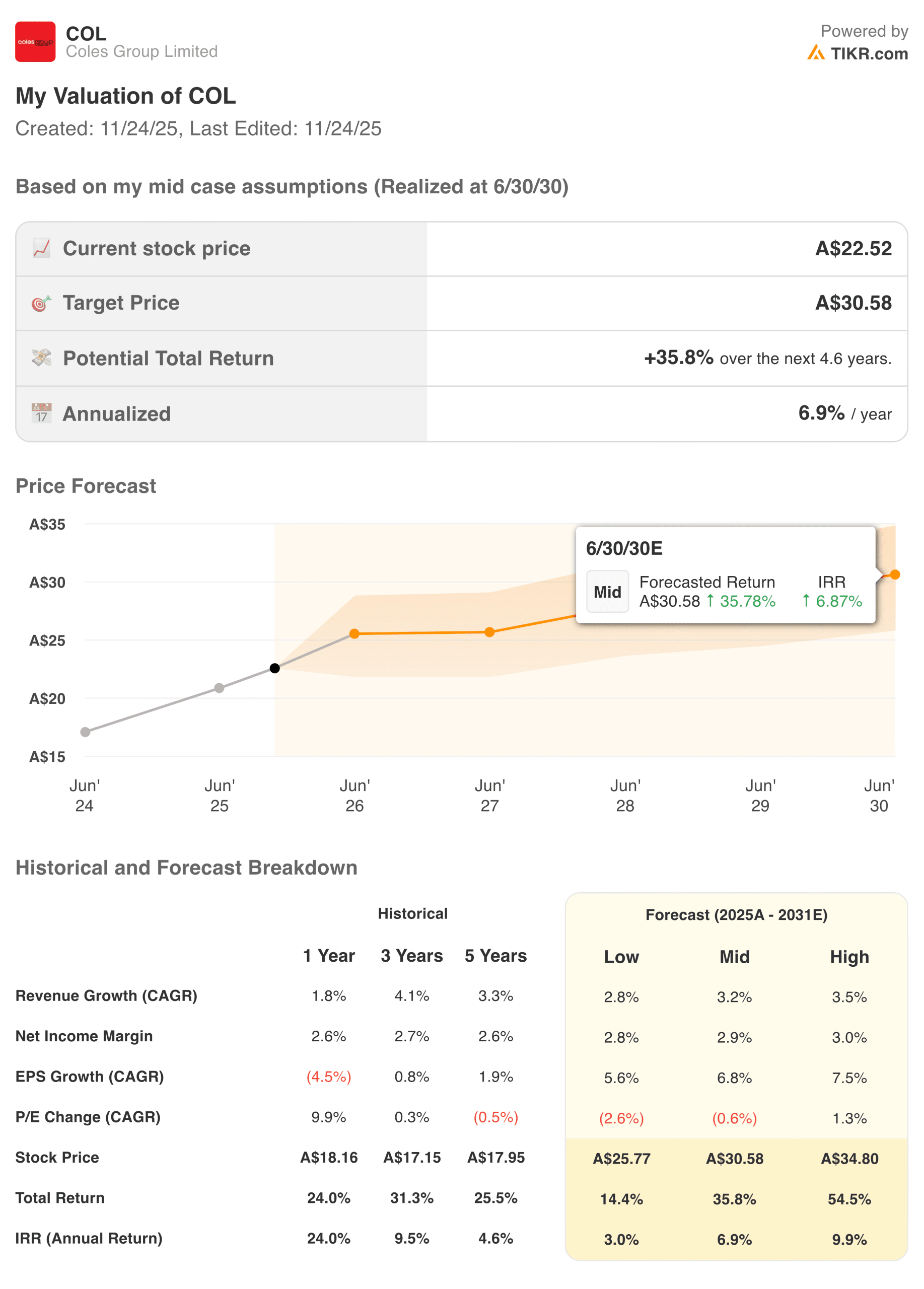

Coles delivered modest top-line performance for FY25, reflecting the realities of a slower consumer environment. Revenue increased 1.8%, supported by stable grocery demand and stronger online contribution. Net income margin held at 2.6%, showing disciplined cost control despite labor inflation and higher shrinkage.

| Metric | FY24 | FY25 |

|---|---|---|

| Revenue Growth (YoY) | 1.7% | 1.8% |

| Net Income Margin | 2.5% | 2.6% |

| EPS Growth (YoY) | 0.8% | (4.5%) |

| Stock Price (Period End) | A$17.15 | A$18.16 |

| Total Return | 31.3% | 24.0% |

Profitability trends were mixed. Earnings per share fell 4.5% year over year, reflecting higher operating expenses, ongoing technology investments, and weaker performance in selected discretionary categories. Still, Coles maintained a steady rhythm in price and promotion management, helping offset pressure in key cost lines.

Valuation expectations for FY26 through FY31 show a balanced path ahead. Analysts forecast 3.2% compound annual revenue growth in the mid case, modest but consistent with a mature supermarket business. EPS growth is expected to reaccelerate toward 6.8% annually as productivity initiatives and supply chain efficiencies take hold. The mid-case valuation model points to a target price of A$30.58, implying a total return of 35.8% over 4.6 years.

Look up Coles Group full financial results & estimates (It’s free)>>>

Broader Market Context

Australian consumer spending remains soft, driven by elevated interest rates, slower wage growth, and cautious household budgets. Supermarkets continue to benefit from value-seeking behavior, private-label adoption, and category stability, but pressure on discretionary spending persists. This dynamic favors retailers with strong loyalty programs, streamlined assortments, and effective cost management.

Coles and Woolworths remain the two dominant players in the sector, each navigating similar macro pressures but executing through different strategic levers. While Woolworths emphasizes premium fresh foods and digital scale, Coles leans toward sharper value positioning and operational simplification. As FY26 approaches, the competitive environment remains rational, giving the industry a steadier foundation after several years of volatility.

1. Margin Stability and Operational Discipline

Coles has focused heavily on tightening its cost structure after a period of higher labor, supply chain, and energy costs. Investments in automation, improved inventory management, and streamlined in-store processes are helping the company regain its margins. These efforts matter because small percentage swings in margin have an outsized effect in low-margin supermarket models.

The company’s ability to hold a net income margin of 2.6% during a difficult environment signals improving execution. Analysts see gradual margin expansion returning as efficiency programs scale and digital volumes increase. This creates a clearer path toward steady EPS growth after a year of compression.

2. The Role of Digital and Online Growth

Online grocery continues to grow as a share of overall revenue, with Coles investing in both delivery and click-and-collect infrastructure. Digital customers tend to demonstrate higher retention, larger baskets, and more consistent purchase frequency. These dynamics give Coles a strategic lever that can generate long-term revenue quality and better margin contribution.

As automated fulfillment and smarter logistics gain traction, online profitability should steadily improve. That matters because Coles needs digital to offset structural cost inflation. Stronger online momentum also helps strengthen customer loyalty, particularly among younger families and time-pressed urban shoppers.

Value stocks like Coles Group in less than 60 seconds with TIKR (It’s free) >>>

3. Competitive Positioning and Customer Value

Coles continues to emphasize everyday value, expanding private-label offerings, and sharpening price perception. This is critical in an environment where Australian households remain price-sensitive and willing to shift between retailers. Coles’ private-label performance has been a bright spot, delivering solid volumes and helping offset margin pressure.

Loyalty and rewards programs also support competitive positioning. Flybuys remains a meaningful differentiator, especially as data-driven promotions become more sophisticated. If Coles can combine strong value perception with a more efficient cost base, it will be well positioned to maintain share and deliver more consistent earnings through FY26 and beyond.

The TIKR Takeaway

Coles is slowly emerging from a reset year with better cost visibility, improving digital engagement, and stable customer volumes. The financial picture is not explosive, but it is becoming more predictable. TIKR’s long-term valuation model shows a reasonable path to mid-single-digit annual growth supported by margin recovery, operational simplification, and disciplined capital allocation. For investors who follow defensive industries, Coles presents a cleaner story heading into FY26.

Should You Buy, Sell, or Hold Coles Group Stock in 2025?

Coles looks steadier than it did a year ago, supported by improving execution and clearer margin trends. Digital growth, private-label momentum, and efficiency programs provide a foundation for more consistent earnings. The next few reports will be important in confirming whether margins can expand and EPS growth can reaccelerate. For now, the stock sits in a reasonable middle ground where patience and steady monitoring make sense.

How Much Upside Does Coles Group Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!