Key Takeaways for Visa Stock as of July 2026

- 29 buy ratings and zero sells back Visa stock, with the mean target at $399 and a 10% premium built into the current $362 price.

- Modeled through September 2030, TIKR’s mid-case scenario prices Visa stock at $687, a 90% total return worth 16% annualized over 4.2 years.

- One of the real levers is value-added services, which climbed 27% in constant dollars to $3.3 billion in the March quarter, now 30% of net revenue and still accelerating.

Visa Stock’s EBITDA Grows 17% as Value-Added Services Reach 30% of Revenue

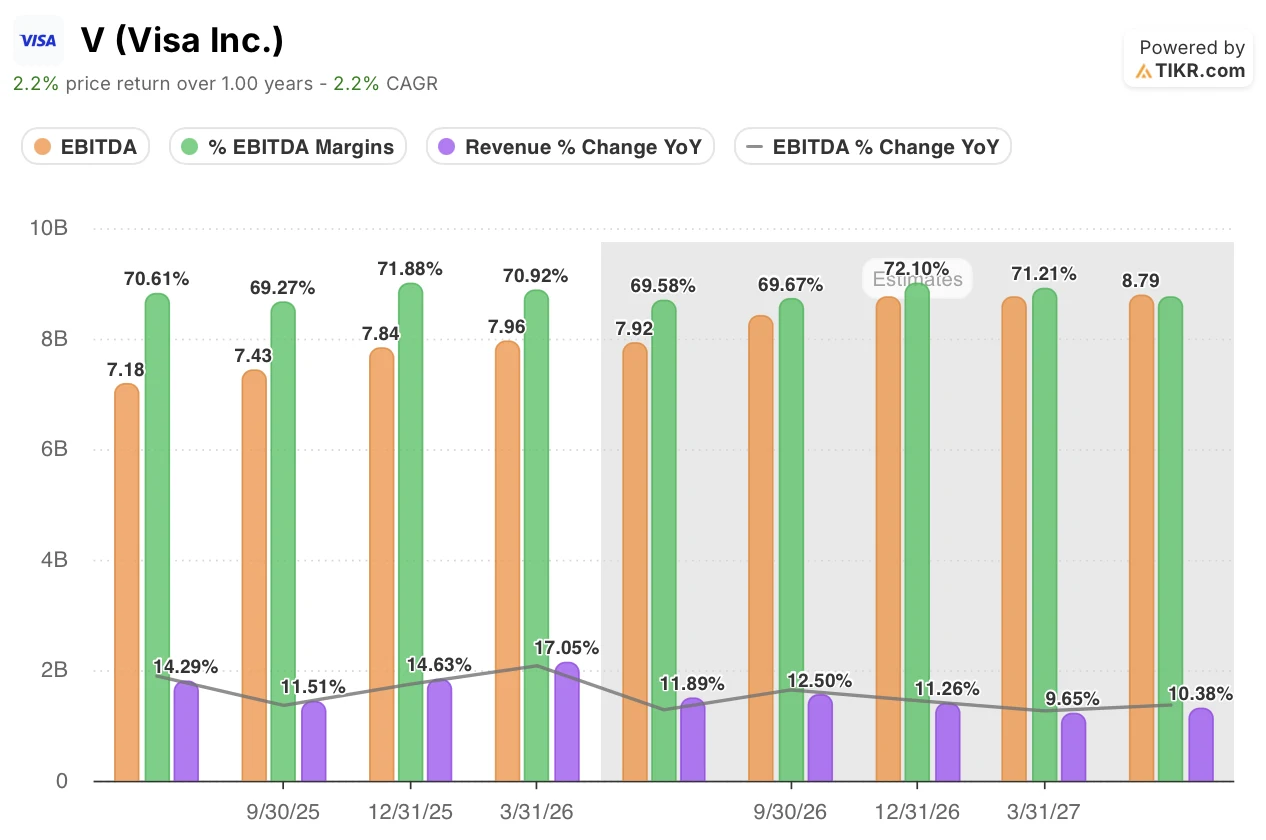

Visa Inc. (V) posted fiscal second-quarter net revenue of $11.23 billion on April 28, its strongest growth pace since 2022, and Visa stock closed at a fresh 52-week high of $362 on July 2. EBITDA climbed 17% to $7.96 billion in the same quarter, with margins holding near 71% even as growth decelerates elsewhere in the model.

Behind that resilience sits Visa’s global network, which links card issuers, acquirers and more than 175 million merchant locations across upwards of 200 countries and territories. Value-added services, the fraud, dispute and data tools layered onto that network, grew 27% in constant dollars to $3.3 billion in the quarter and now make up 30% of net revenue.

With value-added services already a third of net revenue, CEO Ryan McInerney addressed why that growth should hold up on the Q2 earnings call: “These services have durable competitive advantages as the vast majority are linked to transactions, cards and accounts, and they are only strengthened with AI, reinforcing their importance as a growth lever for years to come.” The implication: as AI tools get layered onto fraud and dispute products, the margin benefit compounds rather than fades.

Commercial and money movement solutions delivered a second lever, with revenue up 24% in constant dollars as Visa Direct transactions grew 23% to 3.7 billion for the quarter. Both segments carry higher margins than core consumer payments, which is why EBITDA growth held above revenue growth even as payments volume growth moderated.

Visa’s stablecoin settlement run rate reached $7 billion annualized in the same quarter, up more than 50% from three months earlier, and the company struck a June 10 partnership with OpenAI to route agentic commerce payments through its network. Neither shows up in EBITDA yet, but both extend the transaction base value-added services eventually monetizes.

Visa also bought back $7.9 billion in stock in the quarter, its largest buyback ever, and the board added a new $20 billion authorization in April, putting total capacity at $33 billion. That signals management sees the current valuation gap as wide enough to defend with capital, not just commentary.

Wall Street Analysts Rate Visa Stock a Near-Unanimous Buy at a $399 Mean Target

Wall Street’s rating on Visa stock is lopsided: 29 buy ratings, 8 outperforms, 3 holds and 2 no opinions, with zero sells or underperforms among 42 analysts as of July 2.

The 37 analysts feeding the price target model put the mean at $399, matching the median, which works out to 10% upside from the current $362 price. That premium has compressed sharply since March, when Visa stock traded near $302 against an almost identical $398 mean target, a gap that then implied 32% upside.

The $450 high and $330 low targets have barely moved in two straight quarters, and the tight band between them signals limited disagreement over where the stock’s ceiling sits heading into fiscal 2027.

Wall Street Expects Visa Stock’s EBITDA to Keep Compounding Through Fiscal 2027

Visa’s EBITDA reached $7.96 billion in the quarter ended March 31, up 17% year over year, with margins near 71%. That marked the fourth straight quarter of double-digit growth for the metric.

Analysts model EBITDA at $8 billion in the June quarter, a projected 10% gain, before growth reaccelerates to 13% in the September quarter. Value-added services and commercial payments, both growing revenue faster than the consumer segment, are the two engines behind that reacceleration.

Further out, the model has EBITDA reaching $9 billion by December, up 12%, and holding near $9 billion through June 2027, with margins projected to stay close to 70% the entire stretch. By comparison, revenue growth over the same stretch slows from 13% to 10%, which puts more of the story in margin than top-line expansion.

The thesis holds only if value-added services revenue, which grew 27% last quarter, keeps compounding above 20% through fiscal 2027, with commercial payments providing a second engine if that pace slips.

TIKR’s $687 Target on Visa Stock Holds if Value-Added Services Keep Compounding

TIKR’s mid-case model values Visa stock at $687 by September 2030, implying a 90% total return from the current price of $362, or 16% annualized over 4.2 years.

[TIKR Valuation Model Chart]

That gap becomes plausible if value-added services keeps compounding near 27% and EBITDA margins hold close to 70%, the trajectory the March quarter already showed. Commercial and money movement growth of 24% adds a second lever the Street’s $399 target does not appear to fully credit.

The record $7.9 billion buyback in the March quarter, backed by a fresh $20 billion authorization, gives management a direct tool to close that gap even before the fundamentals catch up.

Should You Invest in Visa Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Visa Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Visa Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze V stock on TIKR for Free →