Key Stats for Under Armour Stock

- Past-Week Performance: -6%

- 52-Week Range: $4.1 to $8.2

- Current Price: $7.6

What Happened?

Under Armour (UAA) is executing the most consequential inflection of its multi-year turnaround, with CEO Kevin Plank declaring December the bottom of the North America reset while UAA stock trades at $7.6, sitting 6.5% below its 52-week high of $8.2 and primed for a rerating.

Driving the sentiment shift, Fairfax Financial’s Prem Watsa, a 10% beneficial owner, filed an acquisition of additional Class C common shares on January 29, signaling that the largest outside shareholder is adding conviction precisely as the brand stabilization thesis takes hold.

Powering the recovery narrative, Under Armour delivered a Q3 adjusted EPS of $0.09 against an expected loss of $0.02, beat revenue estimates at $1.3 billion versus the $1.3 billion consensus, and lifted full year adjusted EPS guidance to $0.10 to $0.11 from a prior range of $0.03 to $0.05.

Beyond the quarter, the market is beginning to shift its mental model of Under Armour from a structurally impaired turnaround story to a brand repositioning play, as SKU rationalization, ASP expansion in footwear above $100, and improving wholesale order books signal a business moving from reset to execution.

President and CEO Kevin Plank stated on the Q3 earnings call that “North America is beginning to turn the corner. We believe the December quarter marks the bottom of the reset,” contextualizing a fall order book that is no longer showing significant declines and wholesale partner confidence visibly recovering.

Countering that optimism, Citigroup downgraded UAA to “sell” on February 10 with a price target of $6.2, citing intense competition and persistently weak DTC trends, a call that directly contradicts the bull case and keeps 2 of 26 brokerages in the bearish camp against 20 holds.

Looking out three to five years, Under Armour’s combination of SKU discipline, a 300-fabric-to-30-fabric raw material consolidation, ASP expansion toward $100-plus in footwear, and EMEA growing at 9% annually positions the brand to rebuild pricing power and margin credibility in a $5 billion consumer demand market it already authentically owns.

Wall Street’s Take on UAA Stock

With CEO Kevin Plank declaring December the bottom of North America’s reset and the fall order book showing no further significant declines, UAA’s Q3 beat directly accelerates the timeline toward FY2027 stabilization and makes the current $7.6 price a potential inflection entry point.

Yet the fundamentals still demand scrutiny, as forward estimates show FY2026 revenue compressing 3.9% to $5.0 billion while normalized EPS collapses 62.9% to $0.11, confirming the business is still contracting even as the turnaround narrative builds momentum heading into FY2027.

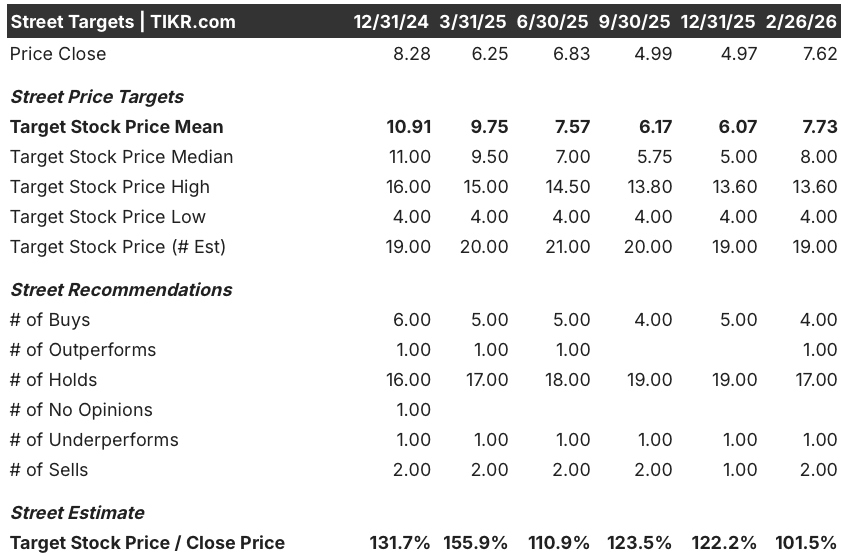

Wall Street currently shows 4 buys, 1 outperform, 17 holds, and 2 sells against a mean price target of $7.7, implying just 1.5% upside from UAA’s current price of $7.6, signaling analysts are holding a cautious wait-and-see posture rather than upgrading into the recovery story.

The analyst target range spans $4.0 to $13.6, where the low reflects continued DTC weakness and tariff margin pressure while the high requires North America wholesale to reaccelerate meaningfully in FY2027, making the fall order book confirmation in May the single most important inflection point to watch.

What Does the Valuation Model Say?

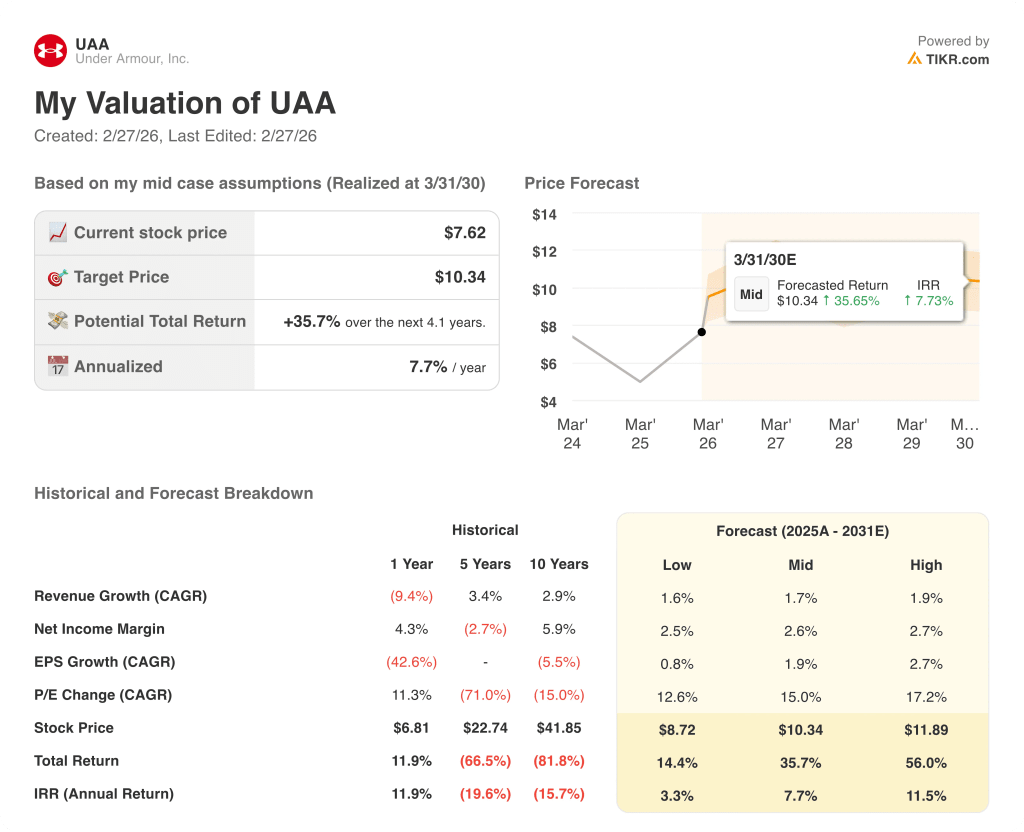

Given the still-compressing margins and early-stage nature of the brand reset, the mid-case valuation prices UAA at $10.3, implying a 35.7% total return and a 7.7% annualized IRR through March 2030, a return profile that feels credible only if FY2027 stabilization executes on schedule.

The most consequential risk remains tariff exposure, with U.S. import costs adding roughly $100 million this fiscal year, driving a 190 bps gross margin contraction that pushes EBITDA margins to just 4.6% in FY2026 against 6.5% the prior year, leaving almost no room for execution missteps.

UAA is a wait-and-see at current prices, fairly valued against a mean target of just $7.7, with the May earnings call serving as the first real test of whether North America wholesale stabilization and footwear ASP recovery can translate from narrative into numbers that justify re-rating the stock higher.

Should You Invest in Under Armour, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UAA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Under Armour, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze UAA stock on TIKR for Free →