Key Stats for UCTT Stock

- Past-6-Month Performance: 186%

- 52-Week Range: $17 to $74

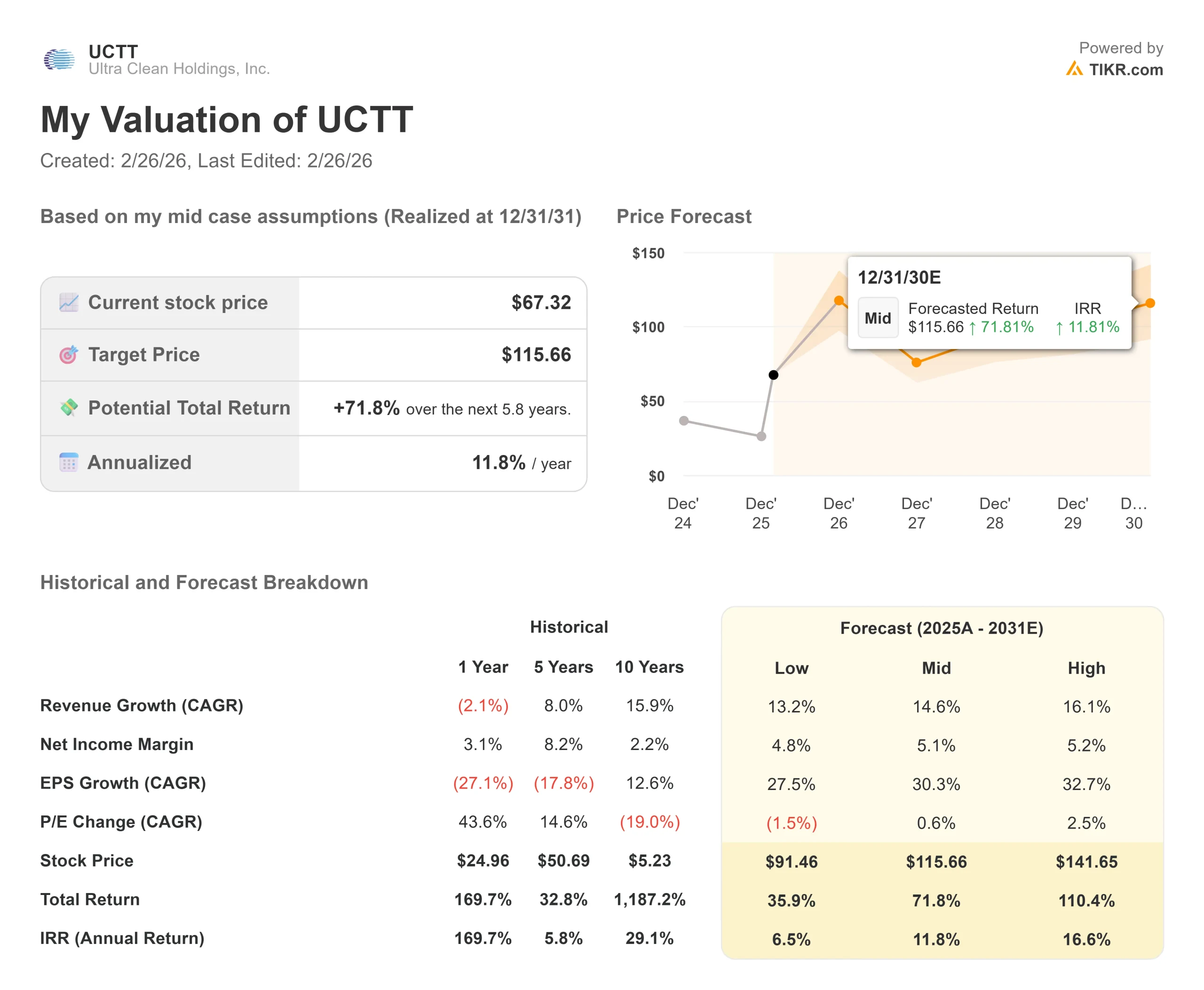

- Valuation Model Target Price: $116

- Implied Upside: 72%

Value your favorite stocks like Ultra Clean Holdings with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Ultra Clean Holdings stock has surged about 186% over the past six months, recently trading near $67 per share and approaching its 52-week high of $74.

The advance reflects a sharp reversal in semiconductor capital equipment sentiment as investors repositioned for a cyclical recovery heading into 2026.

The rally has been driven primarily by improving forward demand expectations and aggressive investor repositioning across semiconductor suppliers.

As capital spending visibility strengthened for advanced logic and memory, expectations for operating leverage improved materially, fueling multiple expansion and renewed institutional participation.

Institutional activity has reinforced the move. Public Sector Pension Investment Board increased its stake by 14.9% in Q3 to 176,870 shares worth $4.82 million, while Optimize Financial initiated a 56,535 share position valued at $1.54 million and Y Intercept Hong Kong Ltd added 35,295 shares worth approximately $962,000.

Institutional ownership now stands at 96.06%, signaling strong professional investor engagement during the recovery phase.

Ultra Clean also announced it will release fourth quarter and full year 2025 results on February 23, 2026, after market close, with a conference call scheduled the same day at 1:45 p.m. PT.

The company named Robert Wunar as Chief Operating Officer effective March 23, 2026, bringing over 30 years of semiconductor capital equipment experience as the company prepares for what management expects to be a more constructive demand environment in 2026.

See analysts’ growth forecasts and price targets for Ultra Clean Holdings (It’s free) >>>

Is UCTT Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 14.6%

- Net Income Margin: 5.1%

- Exit P/E Multiple: 0.6% CAGR expansion

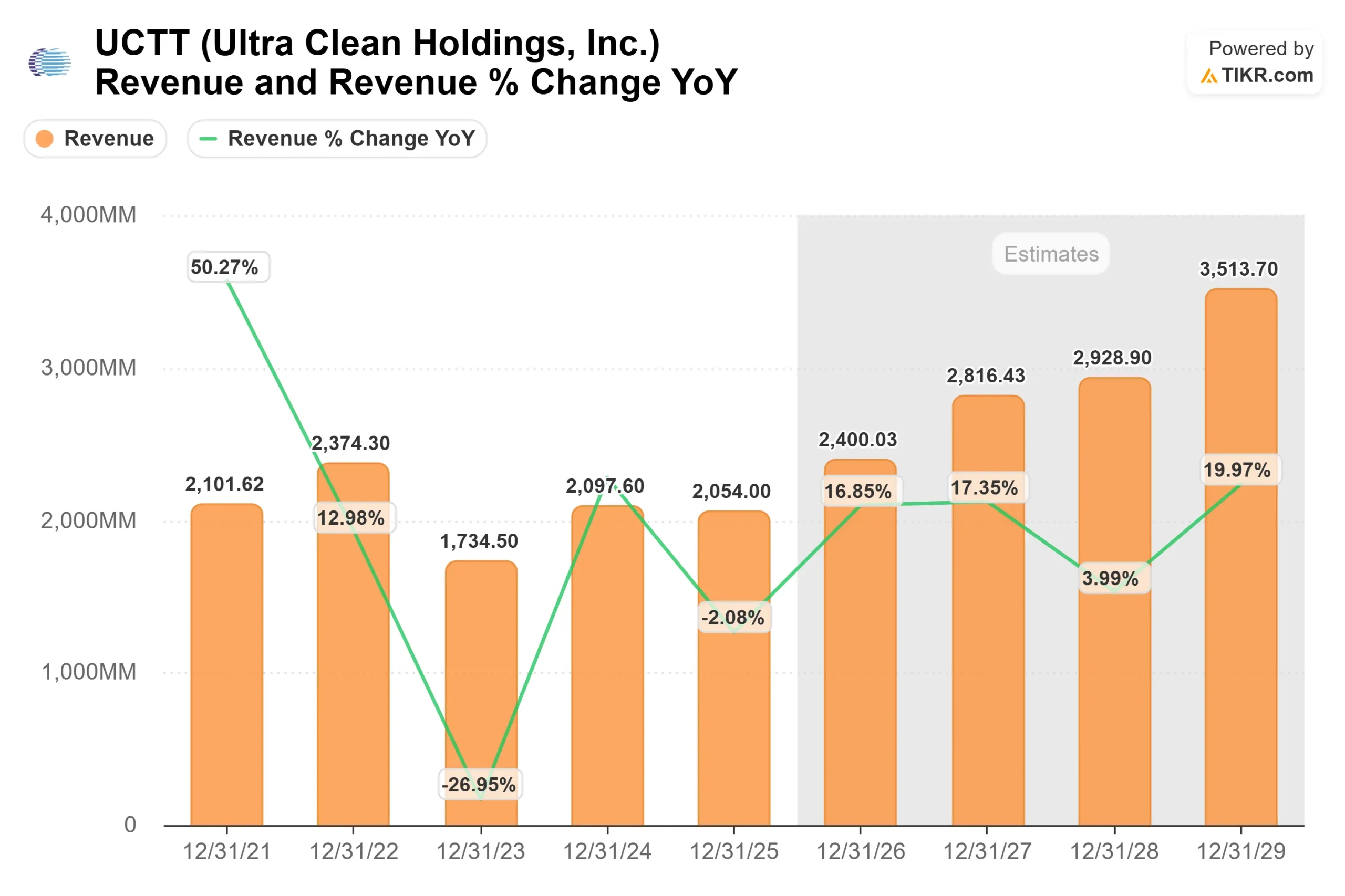

Revenue is projected to rise from about $2.1 billion in 2025 to roughly $3.5 billion by 2029, reflecting normalization in wafer fabrication equipment demand and stronger semiconductor capital investment after the 2023 downturn.

The central earnings driver is operating leverage. Incremental subsystem shipments tied to advanced logic, memory, and AI-related chip production flow through a cost structure that has already absorbed prior restructuring, allowing profitability to recover meaningfully if utilization rates improve.

Customer inventory normalization and sustained fab expansion remain critical variables in 2026, as improved fixed-cost absorption would directly lift margins from recently depressed levels toward the modeled 5% net income range.

Advanced packaging complexity and higher purity component requirements also increase content per tool, supporting revenue quality even if overall unit growth moderates.

Based on these inputs, the model estimates a target price of $116, implying about 72% total upside over the next several years.

At current levels near $67, UCTT appears undervalued, with future performance driven primarily by semiconductor equipment cycle recovery and structural operating leverage rather than speculative expansion alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>