The New York Times Company (NYSE: NYT) trades around $57/share, up modestly this year as investors weigh steady digital growth against slowing subscriber additions. The company remains one of the most profitable names in digital media, supported by strong brand trust and a resilient subscription-based model.

Recently, The Times announced a major strategic shift to expand its bundled subscription offerings, integrating access to its News, Games, Cooking, and The Athletic apps under one plan. This move follows a steady increase in digital subscribers, which surpassed 10 million earlier this year, highlighting the company’s growing pricing power and ecosystem strength.

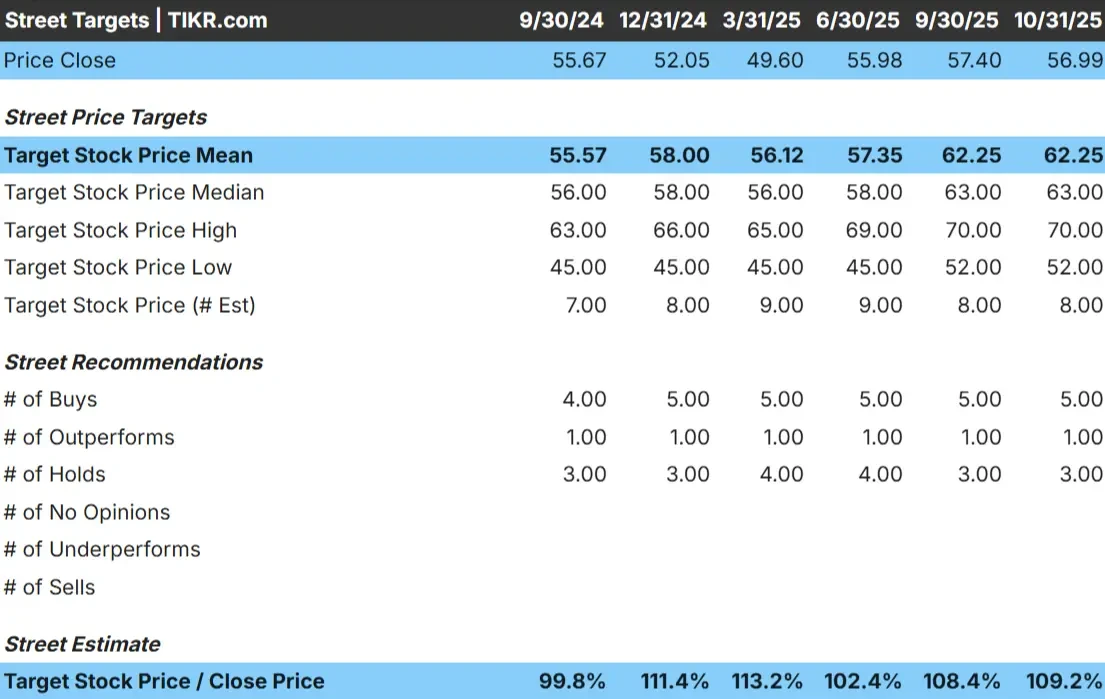

This article explores where Wall Street analysts think NYT could trade by 2027. We have pulled together consensus forecasts and TIKR’s Guided Valuation Model to outline the stock’s potential path based on current expectations.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

The New York Times trades around $57/share today. The average analyst price target is $62/share, implying about 9% upside over the next year. Forecasts remain tight, showing steady confidence in the company’s long-term fundamentals rather than a strong short-term rerating.

- High estimate: ~$70/share

- Low estimate: ~$52/share

- Median target: ~$63/share

- Ratings: 5 Buys, 1 Outperform, 3 Holds

Analysts appear cautiously optimistic, expecting NYT to grind higher as subscription revenue expands and cost controls strengthen margins. For investors, that means the stock could modestly outperform if digital engagement remains strong and operating efficiency continues to improve.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

NYT: Growth Outlook and Valuation

The company’s financial outlook remains solid, supported by consistent digital growth and disciplined spending:

- Revenue projected to grow about 6–7% annually through 2027

- Operating margins expected to rise from 12% to nearly 18%

- Shares trade at around 24x forward earnings, slightly above historical averages

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23.7x forward P/E suggests about $69/share by 2027

- That represents roughly 21% total return, or 9% annualized

For investors, this points to a stable, high-quality business that can compound at a measured pace. The Times is not a high-growth story, but it offers reliability, healthy cash flow, and steady upside for those focused on consistent performance over time.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

The New York Times continues to strengthen its position as the leading digital news brand. Its subscriber base has surpassed 10 million, reflecting strong engagement across News, Games, Cooking, and The Athletic. This ecosystem approach has turned NYT into more than a newspaper; it is now a lifestyle platform that monetizes loyal audiences through multiple content verticals.

Advertising has also shown signs of recovery, particularly in digital formats, while disciplined cost management has supported healthy cash generation. For investors, these strengths suggest NYT can sustain earnings growth even in a slower macro environment, with digital scale and pricing power driving steady margin expansion.

Bear Case: Valuation and Competition

Despite its strengths, NYT’s valuation leaves little room for disappointment. The stock trades around 24x forward earnings, slightly above its historical range, which already prices in much of the expected growth.

Competition for reader attention remains fierce. Free digital platforms, independent newsletters, and social media outlets continue to fragment audiences. For investors, the main risk is that subscriber growth slows faster than expected, limiting operating leverage and making it harder to justify the current multiple.

Outlook for 2027: What Could NYT Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23.7x forward P/E suggests The New York Times could trade near $69/share by 2027. That would represent about 21% total return, or roughly 9% annualized growth from current levels.

This forecast assumes stable subscription momentum and gradual margin expansion. To deliver stronger upside, NYT would likely need to outperform on digital monetization or accelerate ad revenue recovery. Without that, investors should expect steady but moderate gains supported by consistent profitability and strong cash flow.

For investors, NYT looks like a durable, high-quality compounder that rewards patience more than risk-taking.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>