Roku, Inc. (NASDAQ: ROKU) has rallied to about $106/share after a strong rebound in 2025. The company’s platform scale and improving cost discipline are helping it recover from recent ad market softness. While growth has moderated, Roku’s position in connected TV remains a key advantage as streaming continues to expand.

Recently, Roku announced the expansion of its Roku Channel lineup with more free ad-supported content, alongside partnerships with Warner Bros. Discovery and NBCUniversal to strengthen its advertising inventory. The company also introduced new AI-driven tools for advertisers, aimed at improving ad targeting and campaign performance across its 83 million active accounts. These updates highlight Roku’s continued push to enhance monetization and platform engagement amid a competitive streaming landscape.

This article explores where Wall Street analysts think Roku could trade by 2027. We have pulled together consensus targets and valuation models from TIKR to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Limited Upside

Roku trades around $106/share today. The average analyst price target is $107/share, suggesting roughly flat returns over the next year. Forecasts show a wide spread and reflect mixed sentiment:

- High estimate: ~$145/share

- Low estimate: ~$73/share

- Median target: ~$110/share

- Ratings: 13 Buys, 3 Outperforms, 12 Holds, 1 Underperform, 1 Sell

With the stock already near its average target, analysts believe Roku’s recent rebound may be largely priced in. The wide target range signals uncertainty over how quickly the company can turn platform growth into sustainable profits. For investors, this means short-term upside looks limited unless Roku delivers stronger earnings momentum or an advertising recovery that exceeds expectations.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Roku: Growth Outlook and Valuation

Roku’s fundamentals are stabilizing after several volatile years, supported by rising active accounts and improved cost control:

- Revenue growth: ~12.8% annually through 2027

- Operating margin: 2.3% forecast by 2027 (up from -2.3% today)

- Forward P/E: ~119x

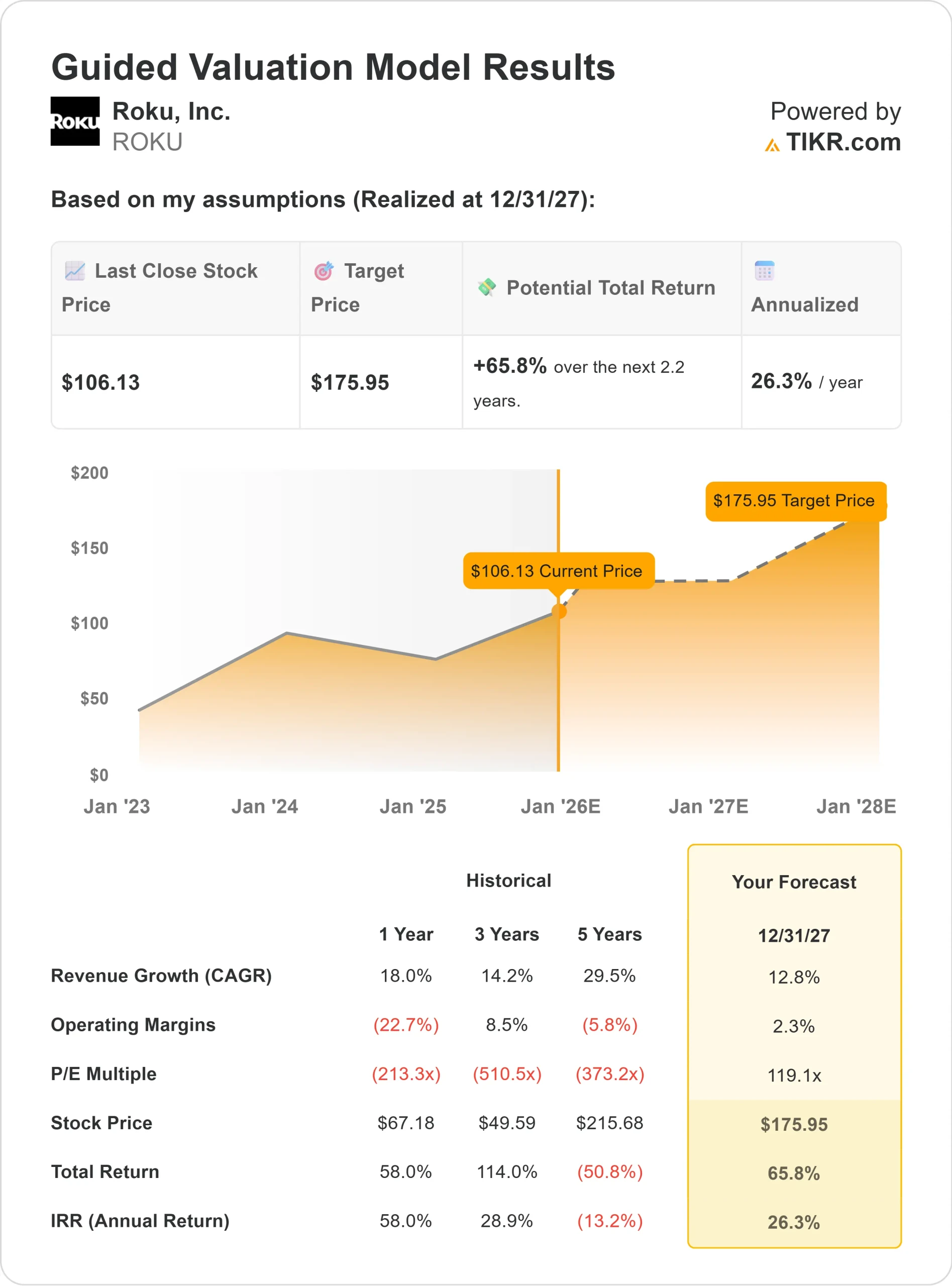

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 119x forward P/E suggests ~$176/share by 2027

- That implies about 66% upside, or roughly 26% annualized returns

This model reflects expectations that Roku will achieve meaningful operating leverage as ad spending rebounds and platform monetization improves. For investors, the takeaway is that Roku could still deliver strong medium-term returns if profitability expands as planned, but its premium valuation leaves little margin for error.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Roku remains one of the leading platforms in connected TV, serving more than 80 million active accounts across North America and international markets. Its advertising revenue continues to grow as marketers shift budgets toward streaming, and free ad-supported content on The Roku Channel is expanding engagement.

Management has also become more disciplined on costs, helping margins recover from pandemic-era lows. With stronger ad partnerships and AI-driven ad tools improving campaign performance, Roku is positioning itself to capture a larger share of the streaming ad market.

For investors, these trends suggest Roku has the platform scale and operating leverage to gradually rebuild profitability and deliver steady long-term compounding if execution remains strong.

Bear Case: Competition and Valuation Risk

Despite progress, Roku’s valuation remains demanding given its modest earnings profile. The stock trades at roughly 119x forward earnings, reflecting optimism that profits will expand sharply in coming years. Any slowdown in ad growth or user engagement could challenge those expectations.

Competition is also intensifying as tech giants like Amazon, Google, and Samsung invest heavily in their own TV operating systems and ad platforms. These players have broader ecosystems and larger data networks, which could pressure Roku’s ad margins over time.

For investors, the risk is that Roku’s growth story may already be priced in. Without sustained revenue acceleration and margin improvement, the stock could struggle to justify its premium multiple.

Outlook for 2027: What Could Roku Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 119x forward P/E suggests Roku could trade near $176/share by 2027. That would represent about 66% upside, or roughly 26% annualized returns from current levels.

While this projection points to strong potential gains, it already assumes a rebound in ad spending and further operating efficiency. To deliver even stronger returns, Roku would need to exceed expectations in ad monetization, international growth, and cost control.

For investors, Roku looks like a promising long-term growth story in streaming, but the upside will depend on management’s ability to turn its large user base into consistent, scalable profits.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>