Fox Corporation (NASDAQ: FOXA) shares have climbed over 40% in 2025, now trading near $65/share. The rebound has been driven by stronger ad revenue, stable affiliate fees, and disciplined cost management that helped lift profits after a weak 2024.

Recently, Fox announced plans to expand its digital sports coverage through its Tubi streaming platform, signaling a deeper push into ad-supported streaming. The company also renewed its long-term NFL broadcasting deal and secured additional college football rights, reinforcing its dominance in live sports programming. These moves highlight management’s focus on keeping Fox relevant as media consumption shifts toward digital platforms.

This article explores where Wall Street analysts expect Fox stock to trade by 2028. We have pulled together consensus targets and valuation models to outline the stock’s potential path based on current market expectations.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Fox trades at about $65/share today. The average analyst price target is $71/share, which points to roughly 7% upside over the next year. Forecasts remain mixed and reflect cautious sentiment:

- High estimate: ~$97/share

- Low estimate: ~$55/share

- Median target: ~$68/share

- Ratings: 10 Buys, 10 Holds, 1 Sell

It looks like analysts see modest potential for gains, but conviction remains low. For investors, this suggests Fox could deliver steady performance if digital initiatives and ad recovery continue, though major upside will likely require stronger earnings growth.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Fox: Growth Outlook and Valuation

The company’s fundamentals appear stable but not particularly strong:

- Revenue growth projected at ~1% CAGR through 2027

- Operating margins expected to stay near 18%

- Shares trade at ~14x forward earnings, slightly below peers

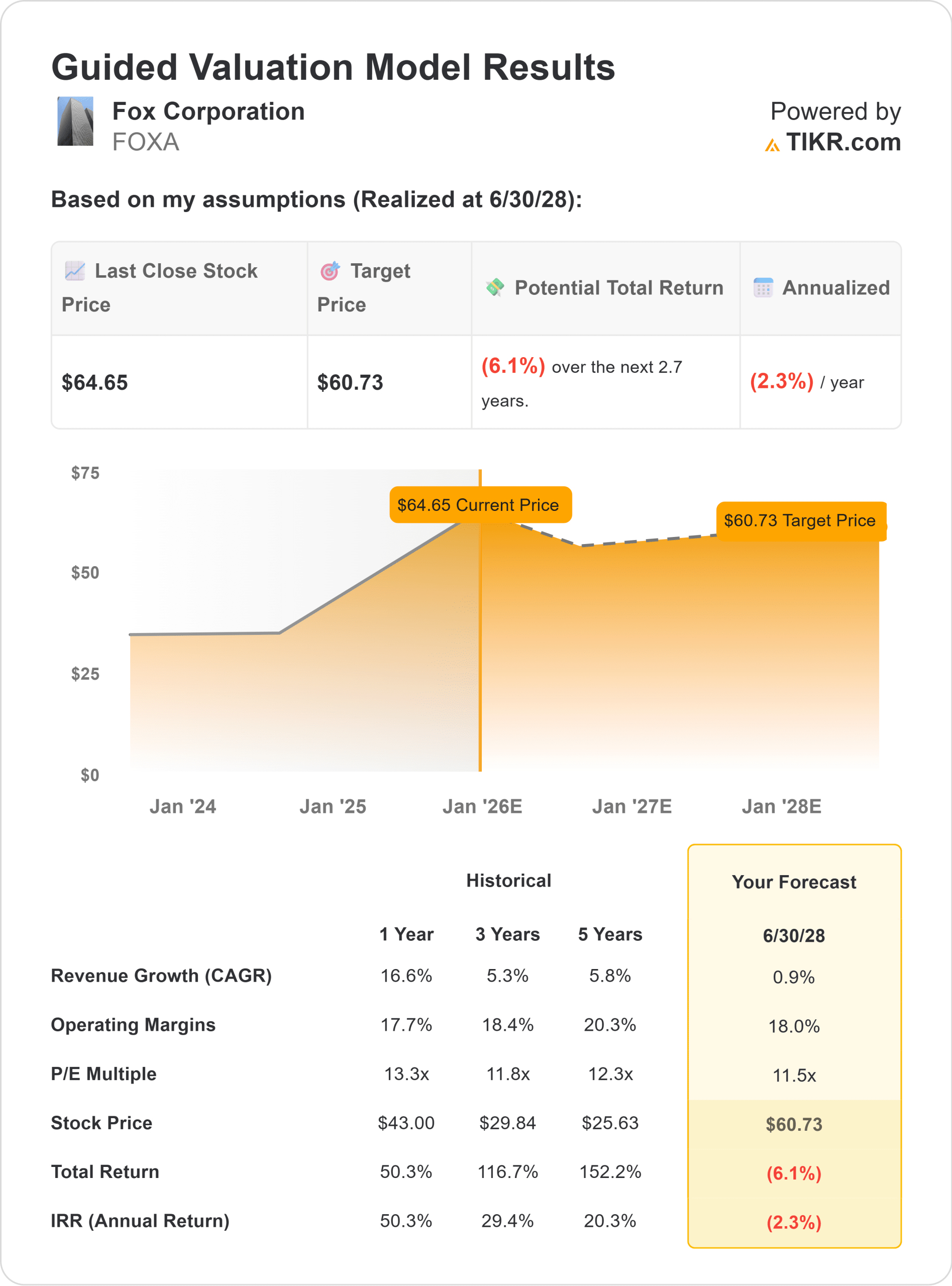

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11.5x forward P/E suggests ~$61/share by 2028

That implies about 6% downside, or roughly -2% annualized returns. For investors, this means the stock already reflects much of its recent recovery. Unless Fox can accelerate its digital expansion or lift affiliate margins, returns may stay muted despite strong cash generation and consistent shareholder returns.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Fox’s core strengths remain in live news and sports, two areas that continue to attract large audiences and premium advertising demand. Its growing presence on Tubi and consistent free cash flow provide a base of stability that supports dividends and buybacks.

For investors, these factors suggest that Fox is well positioned to preserve profitability even in a slow-growth environment. The company’s renewed sports deals and steady advertising partnerships help ensure revenue resilience across cycles.

Bear Case: Sluggish Growth and Limited Catalysts

The main concern is stagnation. The average analyst price target sits below the current share price, indicating low expectations for near-term upside. Revenue growth remains slow, and EBITDA is projected to decline slightly through 2027.

Fox still relies heavily on traditional TV, where cord-cutting and soft advertising demand continue to pressure results. Without meaningful progress in digital monetization, the company may find it difficult to grow earnings faster than inflation.

For investors, Fox looks more like a stable income stock than a long-term growth compounder.

Outlook for 2028: What Could Fox Be Worth?

Based on analysts’ average estimates, Fox could trade near $61/share by 2028, implying around 6% downside from current levels.

For investors, that points to limited upside potential. Fox remains financially sound with dependable cash flows and strong brand assets in sports and news, but the lack of clear growth catalysts limits valuation expansion. Unless management executes a successful digital transition, the stock may continue to deliver steady but unspectacular returns.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>