The Walt Disney Company (NYSE: DIS) has regained momentum as earnings stabilize and streaming losses narrow. The stock trades near $113/share, up about 14% over the past year, supported by strong park attendance, steady cost cuts, and improving profitability at Disney+.

Recently, Disney completed its acquisition of the remaining stake in Hulu, paying about $439 million to take full control. Hulu will now be fully integrated into the Disney+ platform in the U.S., while internationally it will replace the “Star” brand starting in October 2025. Meanwhile, Disney’s sports division, ESPN, is preparing to launch a standalone direct-to-consumer streaming service later in 2025, which will also be available as part of a bundled offering with Disney+ and Hulu. These moves highlight management’s focus on streamlining its streaming ecosystem, improving margins, and strengthening its position in direct-to-consumer entertainment.

This article explores where Wall Street analysts think Disney could trade by 2027. We’ve pulled together consensus forecasts and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

Disney trades around $113/share today. The average analyst price target sits near $134/share, implying about 19% upside over the next year. Forecasts show cautious optimism across Wall Street:

- High estimate: ~$160/share

- Low estimate: ~$77/share

- Median target: ~$138/share

- Ratings: 21 Buys, 4 Outperforms, 6 Holds, 1 Sell

Analysts believe Disney’s earnings recovery and margin expansion could continue driving the stock higher. For investors, that means the path to gains remains open, but not guaranteed. The upside looks meaningful if management sustains streaming profitability and parks performance through 2027.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Disney: Growth Outlook and Valuation

Disney’s fundamentals are improving across its core segments as cost control and asset efficiency start paying off.

- Revenue is projected to grow ~5% annually through 2027

- Operating margin expected to reach ~19.5%

- Shares trade at ~18x forward earnings, slightly below their long-term average

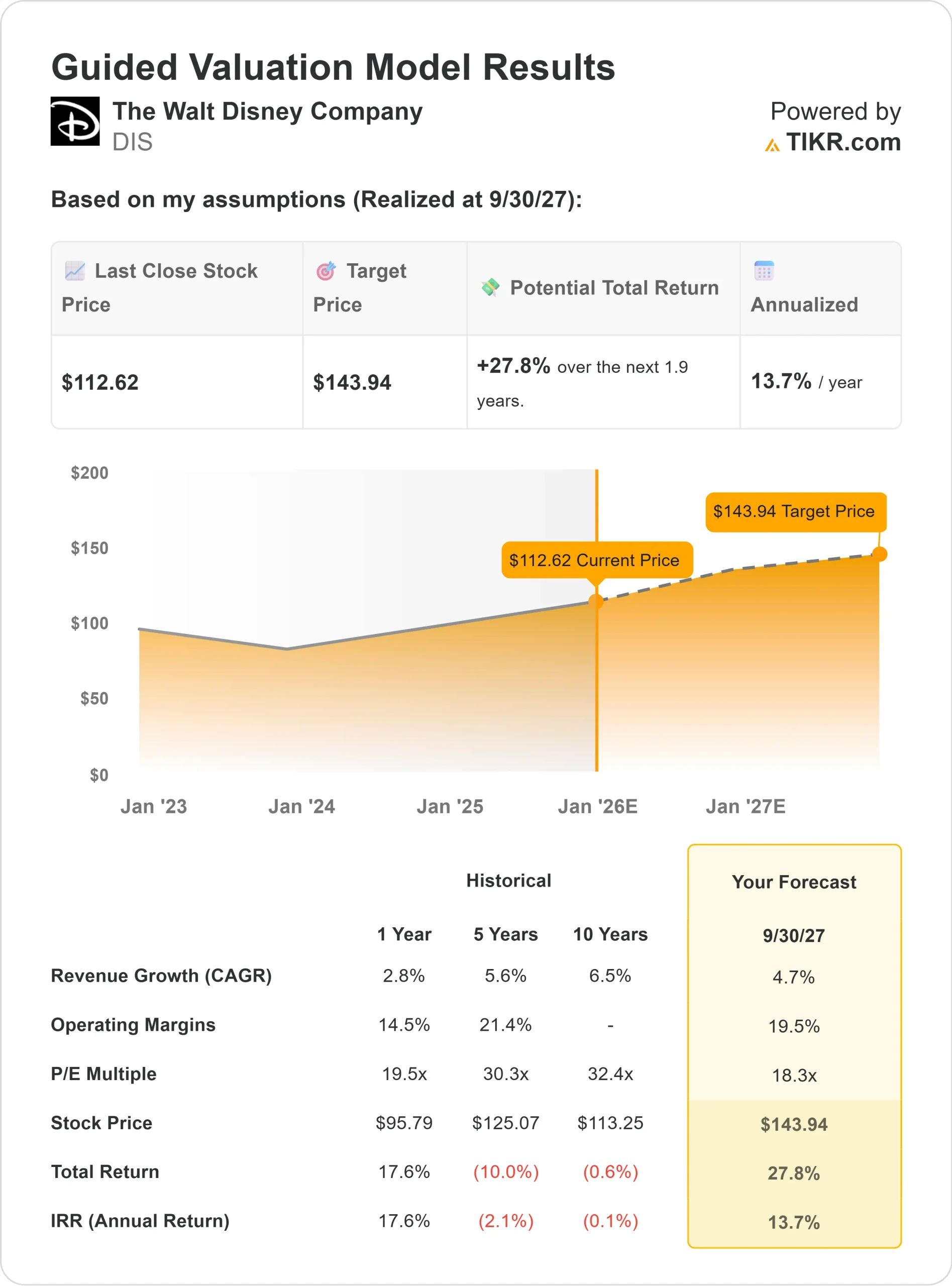

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P/E suggests ~$144/share by 2027

- That implies about 28% total upside, or roughly 14% annualized returns

For investors, this signals a company returning to healthy compounding. The stock looks reasonably valued given its improving cash flow and brand strength, but stronger execution in streaming and media will determine whether Disney delivers above-average returns.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Disney remains one of the world’s most valuable entertainment brands. Its parks and experiences business continues to generate solid cash flow, while the streaming segment shows progress toward profitability.

Management’s focus on cost efficiency, better pricing, and digital content integration is creating a leaner, more resilient business model. For investors, these moves suggest Disney is successfully transitioning from a turnaround story to a steady compounder with reliable earnings momentum.

Bear Case: Execution and Media Challenges

Even with clear progress, Disney still faces structural challenges. The decline of traditional TV continues to weigh on advertising, and competition from Netflix and Amazon keeps streaming growth in check.

While the stock’s valuation looks fair today, any slip in earnings or subscriber growth could limit upside. For investors, the key risk is whether Disney can consistently translate its global brand and creative assets into sustainable profit growth in a rapidly evolving media landscape.

Outlook for 2027: What Could Disney Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P/E suggests Disney could trade near $144/share by 2027. That would represent about a 28% total gain, or roughly 14% annualized returns from current levels.

While that marks a healthy recovery, it already assumes steady execution across parks, media, and streaming. To unlock stronger upside, Disney would need to outperform in direct-to-consumer profitability and maintain strict cost discipline.

For investors, Disney looks like a high-quality recovery story with dependable earnings momentum. The stock may not deliver explosive growth, but it offers a balanced mix of stability, brand strength, and improving fundamentals that could reward patient shareholders through 2027.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>