Key Stats for Starbucks Stock

- Past-Week Performance: +1%

- 52-Week Range: $75.5 to $106

- Current Price: $99

What Happened?

Starbucks (SBUX), the world’s largest coffeehouse chain with 41,000+ locations globally, snapped an eight-quarter U.S. transaction decline in Q1 fiscal 2026, its most concrete proof yet that CEO Brian Niccol’s Back to Starbucks turnaround is producing real behavioral change, with shares sitting at $98.99.

On January 28, Starbucks reported Q1 revenue of $9.9 billion, up 5% year-over-year, with global comparable store sales accelerating to 4% growth led by a 3-percentage-point transaction contribution, as the Green Apron Service model, a $500 million labor investment standardizing staffing and service speed across North American stores, delivered its first full quarter of results.

The 650 coffeehouse pilot stores running the Green Apron program longer than the broader fleet outperformed system comps by 200 basis points, while Starbucks Rewards, the company’s loyalty app with 35.5 million active members, posted its first year-over-year transaction growth in eight quarters alongside accelerating non-member visits, a combination the company had not achieved since Q2 fiscal 2022.

Brian Niccol, Chairman and CEO, stated on the Q1 2026 earnings call that “company-operated transaction comps grew year-over-year for the first time in 8 quarters, and we grew transactions across all dayparts in the quarter,” directly validating the Green Apron rollout that reached all North American company-operated stores in August 2025.

With its reimagined three-tier Starbucks Rewards program launching March 10, the Energy Refreshers platform arriving spring 2026, and a fiscal 2028 framework targeting $3.35 to $4.00 in EPS on 13.5% to 15% operating margins, Starbucks is building compounding growth levers across loyalty, menu, and a 400-store annual U.S. development pipeline that management believes can ultimately double the domestic footprint.

Wall Street’s Take on SBUX Stock

The Q1 transaction inflection, the first positive U.S. comp driven by actual customer growth in eight quarters, directly resets the forward earnings trajectory, as fiscal 2026 EPS consensus of $2.29 implies 7.6% growth after fiscal 2025’s 35.6% collapse.

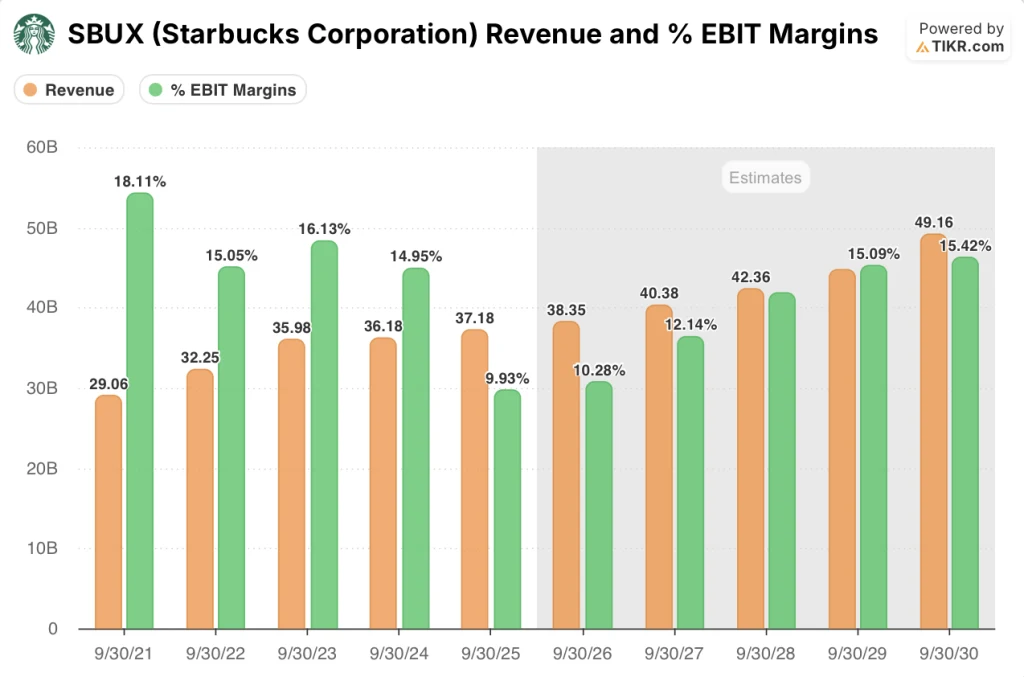

Revenue is rebuilding steadily from a near-stall, with fiscal 2025 actuals of $37.2 billion growing just 2.8% before reaccelerating to an estimated $38.4 billion in fiscal 2026, as the Back to Starbucks plan converts operational investments into measurable top-line momentum.

EBIT margins collapsed to 9.9% in fiscal 2025 from a 15% to 18% range in prior years, are forecast to recover to 10.3% in fiscal 2026, with management targeting 13.5% to 15% by fiscal 2028 as Green Apron investments anniversary.

Thirteen analysts currently rate SBUX a buy, five an outperform, and 15 a hold, with the mean price target sitting at $100.44, implying just 1.5% upside from the current $98.99, suggesting Wall Street is waiting for sustained margin proof before aggressively repricing the recovery.

The analyst target range stretches from $74 on the low end to $120 on the high end, a spread that maps directly to whether the Back to Starbucks plan can convert comp momentum into the margin expansion management has scheduled for fiscal 2028.

What Does the Valuation Model Say?

TIKR’s mid-case model prices SBUX at $139.48, implying 40.9% total return over 4.6 years at a 7.8% annualized IRR, built on a 4.8% revenue CAGR and net income margins recovering to 10.3% from the current 6.5% trough.

The model’s core assumption is margin normalization, and the evidence supporting it is already in motion: 90-plus active cost initiatives targeting $2 billion in savings, Green Apron investments anniversarying in Q4, and coffee and tariff pressures expected to peak in Q2 then abate.

The market is pricing SBUX near flat to the mean analyst target at $98.99, effectively assigning no value to the fiscal 2028 EPS framework of $3.35 to $4.00, which would represent roughly 55% to 85% earnings growth from fiscal 2026 estimates.

The 650 Green Apron pilot stores outperforming the fleet by 200 basis points in comp growth signal that operational consistency, once fully embedded across 18,000-plus North American locations, can structurally lift the system average.

The Back to Starbucks plan holds only if transaction growth sustains, and a deterioration in U.S. comp momentum toward zero would unwind the sales leverage assumption underpinning the entire margin recovery trajectory to 13.5% to 15%.

The April 28 Q2 fiscal 2026 earnings call is the first test of whether the transaction recovery holds beyond the holiday quarter, with the U.S. comp figure and any update on the March 10 Rewards relaunch being the two numbers that matter most.

Should You Invest in Starbucks Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SBUX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Starbucks Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SBUX stock on TIKR for Free →